Meet the New Bond, Same as the Old Bond?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe rally in bonds to close out 2023 reflects the US Federal Reserve's (“Fed’s”) validation of beginning a rate cutting cycle in 2024. Bond markets expect more cuts than the Fed is signaling, and this expectation largely reflects a return to pre-COVID dynamics of low inflation, massive central bank support, and suppressed term premia. That may turn out to be the case, but changes in economic and financial structures emerging in the post-COVID environment could disrupt the return of “old” bond market dynamics—and potentially require a different investor playbook than for past rate cutting cycles.

Key points

- Three kinds of cuts: Cuts, damned cuts, and recessions —a twist on Mark Twain’s “three kinds of lies” quote on statistics illustrates the bond market outlook for 2024. Market consensus expects the Fed to cut interest rates either to (1) maintain restrictiveness as inflation falls, (2) calibrate monetary policy to a less restrictive stance in the face of falling inflation and a slowing economy, or (3) move to easier monetary policy in the face of a recession.

- Structural changes underpinning a “new” bond market regime: Each of these three scenarios leads to an outlook for lower rates and positive returns for bonds. But as another Twain aphorism goes, history may rhyme, but it doesn't repeat. Post-COVID global economic and financial structural changes suggest the potential for a very different bond market playbook during a cycle of global central bank rate cuts.

- A “new” conundrum for bonds? Within the consensus outlook for declining rates is also a consensus for rate declines to be led by the short end of the curve. We look at the potential for a “new” conundrum—playing out in the opposite way of the “old” Greenspan conundrum from the 2004/2005 hiking cycle. Back then, rate hikes at the short end were not met by rising rates at the long end, prompting the now famous “conundrum” (non) explanation. The impact of structural changes to the global market might similarly argue for longer term rates not falling as much (or even potentially rising) during this cutting cycle.

Meet the new bond, same as the old bond?

Despite heady expectations for bond returns in 2023, the near consensus “bonds are back” narrative failed to deliver the kind of returns that would validate bonds being “back.”

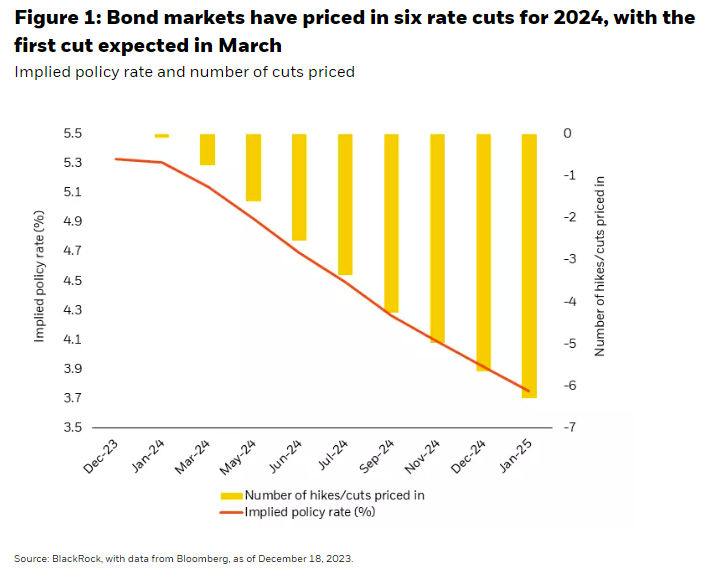

Now, following the stellar bond returns of November, “bonds are back” is back again as investors look forward to the typical backside of the Fed’s interest rate cycle. That cycle “typically” entails several hundred basis points of Fed rate cuts which are now reflected in bond market pricing of the short end of the yield curve (Figure 1).

Why all the rate cuts?

The fuss in the bond market over cuts reflects several developments that have accelerated at the end of 2023.

Figure 2 highlights the “typical” post-peak Fed rate cycle pattern which is fueling expectations for cuts next year. While the greatest number of cuts appears to follow the Fed “overshoot” (where overtightening results in a hard landing for the economy into a recession), the Fed has also typically delivered some rate cuts following the peak of the rate hiking cycle in the absence of a recession.

\

\

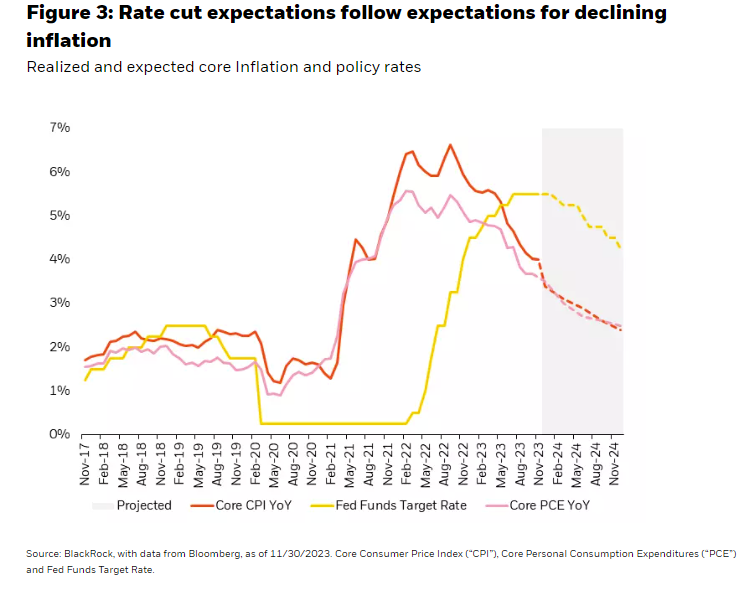

However, the COVID boom-bust cycle of today defies historical comparisons. Rather, the supply and demand induced inflation cycle during this period has been the principal determinant of economic and financial performance. Recently, the driver has been the faster declines in inflation than the market—and the Fed—had been forecasting. And as highlighted in Figure 3, the bond market’s expectations for rate cuts in 2024 largely follows forecasts for inflation to continue falling and relatively uneventfully reaching the Fed’s pre-COVID 2% inflation target.

Three kinds of rate cuts

With the expectation for rate cuts, we can consider three different kinds of cutting scenarios that could take place:

1. Maintenance cuts.

Consider this expectation for rate cuts—what many term “maintenance” cuts—as the first type of rate cutting scenario. “Maintenance” implies that the Fed is cutting rates not to provide accommodation, but to simply keep the policy rate in real terms from rising as it would under the forecasted scenario of continued declines in inflation. Under this scenario, the Fed would cut rates to maintain a relatively constant level of real Fed funds rates (defined as nominal Fed policy rates less inflation). This scenario interprets the Fed’s continued language around remaining “restrictive for longer” as implying a need for vigilance around bringing down inflation sustainably by maintaining the real policy rate. Most of what we see currently priced into bond market rate cut expectations reflects this type of rate cutting action by the Fed in 2024. Notably, this path is also consistent with the “soft landing” economic scenario expected under the consensus outlook.

2. Calibration cuts.

If maintenance holds the real policy rate roughly constant as inflation declines, further interest rate cuts could occur under two additional scenarios. First, slowing economic growth worries the Fed that policy has become too restrictive. Under this scenario, the Fed—convinced of sustained success in taming inflation—would pivot to prioritizing the growth side of its mandate and recalibrate policy to move from restrictive to looking for “neutral.” The cuts implied under this scenario are larger than those that simply follow the path of declining inflation as they occur under the scenario of a desired change in the stance of monetary policy from “sufficiently restrictive” to “neutral.”

3. Recession cuts.

“Recessionary” cuts extend these scenarios to the next level of growth slowdown. As Figure 2 previously highlighted, these are the scenarios where the largest interest rate cuts and largest fixed income returns have historically come. The lack of such large cuts currently priced in reflects the move away from recession expectations that accelerated throughout 2023—making the base case economic expectations for 2024 firmly align with the ”soft-landing” scenario.

One common assumption: 2% inflation

The common assumption underlying each of these scenarios is that the expected path of inflation meets the Fed’s 2% target. This is an expectation of a return to pre-COVID dynamics—and along with that, a return to “divine coincidence”1 in monetary policy where the ability to cut rates to manage growth deviations is unburdened by concerns over inflation as there is (yet again) too little inflation. What might disrupt this convenient market expectation (which is also convenient for the outlook for financial market performance) is an inflation trajectory that fails to cooperate.

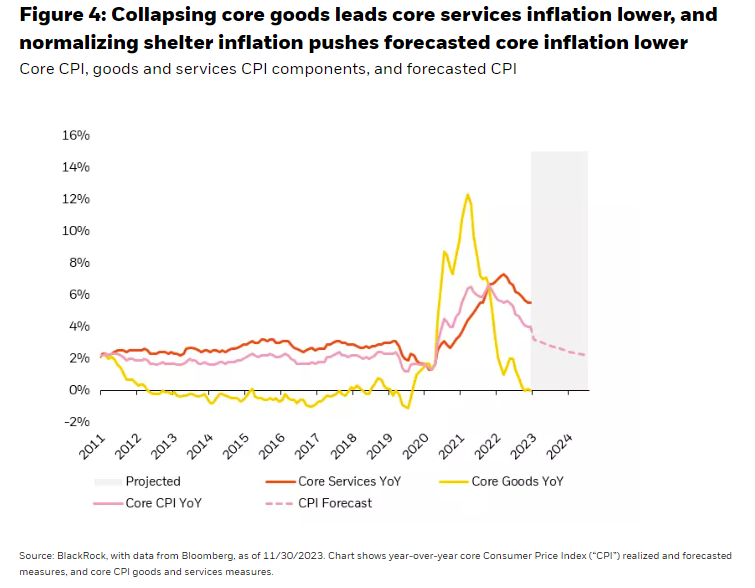

We continue to watch the divergence in services and goods inflation as key to this outlook, as faster declines in goods inflation have mostly been to credit for the faster declines in core inflation that are underpinning overall monetary policy expectations for 2024 (Figure 4). Services inflation is also expected to decline as the lagged impact of falling shelter inflation makes its way into the inflation metric. But if these services and goods inflation declines (and outright deflation) were to not keep up with expectations, continued stickier inflation could up-end the market consensus narrative that maintenance cuts will fuel bullish outcomes for both bonds and stocks.

Structural changes underpinning a “new” bond market regime

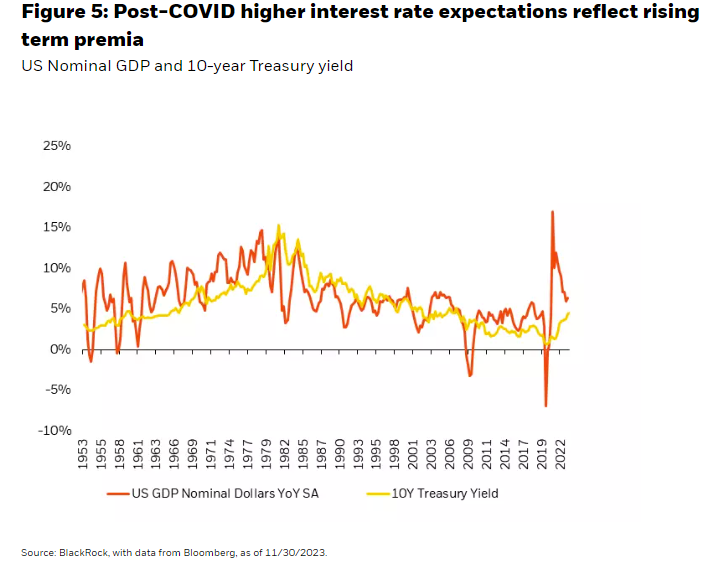

The market consensus outlook for bonds primarily reflects a return to pre-COVID dynamics of 2% growth and 2% inflation—albeit with a higher interest rate structure. A decomposition of term interest rates commonly explains the higher interest rate expectations along the dimensions of real neutral rates + inflation compensation + term premia. But a simpler empirical observation relates the level of term interest rates (in this case 10-year rates) to nominal GDP (Figure 5).

This approach considers the “fair value” for 10-year interest rates simply as the level of nominal GDP +/- a premium (discount). Overall, interest rates track the level of nominal GDP in the economy. In other words, the base rate of risk-free financing tracks the average nominal return in the economy. Whether rates are above (premium) or below (discount) that average, nominal return depends on structural characteristics governing the relative supply of investment capital vs. the demands on that capital.

The pre-COVID and post-2000 environment reflects what Larry Summers has described as a period of “secular stagnation” with too little growth, too little inflation, and an excess of global savings relative to investment demand. This led to a persistent discount of 10-year Treasury rates relative to nominal GDP. The history shows this is not “normal,” but rather a function of the structural elements of the time. And those structural elements change over time rather than reverting back to this particular “discount” setting.

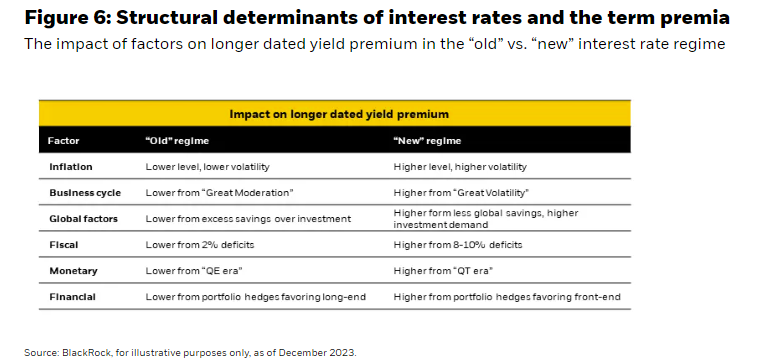

Post-COVID higher interest rate expectations then reflect several of the structural changes that appear to be occurring. These include factors across global economics, monetary and fiscal policy, as well as financial considerations such as debt issuance and portfolio hedging. In each case, the pre-COVID structure supported lower interest rates and flatter term premia, that is, a lower degree of additional yield compensation for extending debt maturities (Figure 6).

Inflation. This one is obvious and clear. The post-COVID environment has seen both higher inflation and higher inflation volatility in a departure from the prior era of sustained low readings in both. Indeed, the period prior to COVID was an era marked by a deficit of inflation.

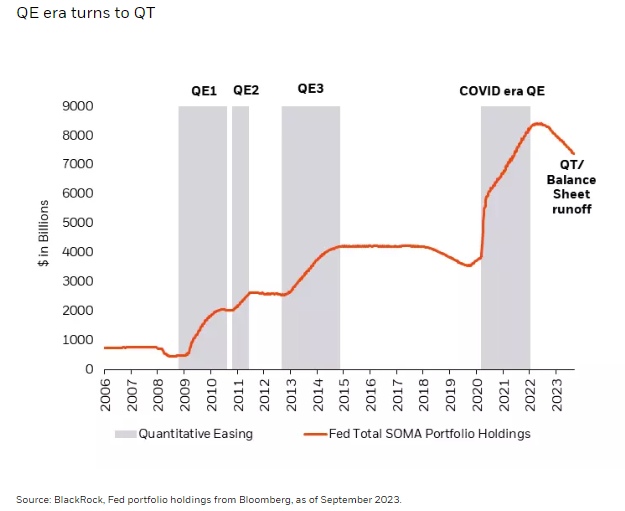

Monetary. Too little inflation allowed for monetary factors (Quantitative Easing (“QE”) era) to expand to deal with the inflation target persistently missing from below. That made a larger arsenal of tools available to deal with the deficit of inflation—including zero and negative interest rate policy, extended forward guidance (promising a longer period of that accommodative policy), and larger and larger amounts of explicit bond purchases (and debt monetization) by global central banks.

Financial. The combination of “divine coincidence” from too little inflation and the central bankers’ use of an arsenal of tools to combat it, led investors to increase their expectations for a central bank insurance policy in the form of long government bonds. This era was characterized by significantly negative stock/bond correlation and a high Sharpe ratio of returns in long dated government bonds. This further led to portfolio hedging favoring long maturity instruments for their capital efficiency and performance efficacy, reinforcing existing trends and further reducing term premia.

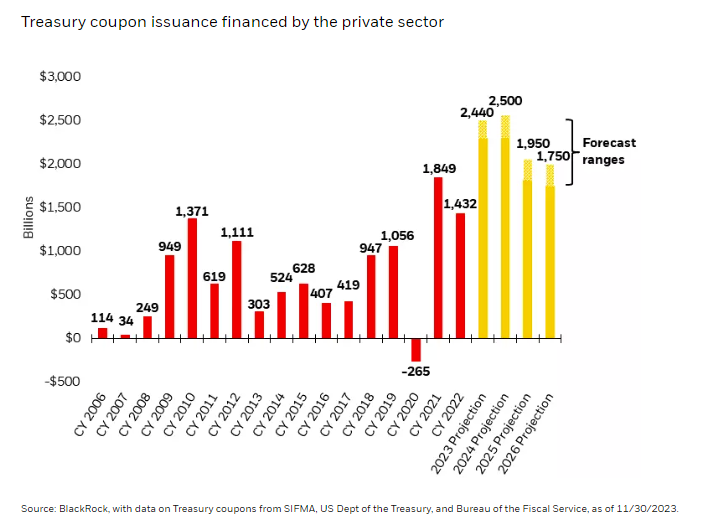

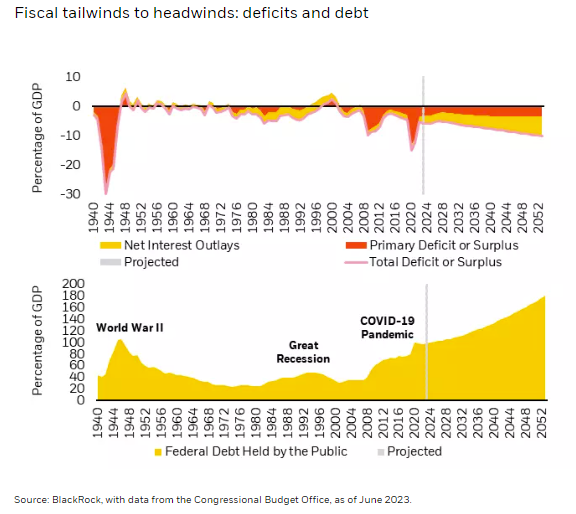

Fiscal. Facing both lower longer term and short term borrowing costs reflecting zero or negative interest rate policy, fiscal policymakers deferred the cost of profligacy. Some took this to an extreme, arguing for a “Modern Monetary Theory” which held additional spending should not be constrained by concerns over debt and deficits. Monetary policy contributed to rising long term spending in the QE era as recycled short term “profits” from QE policies of “borrowing” costs below invested asset yields reduced Federal deficits, flattering near term deficit estimates, and lowering near term issuance requirements. A normalizing monetary policy now exacerbates the implications of structurally higher deficits leading to greater issuance absorption required from private investors—the opposite as during the QE era.

Global factors. Global factors in the pre-COVID era contributed to these dynamics through the globalization of supply chains. This led to falling costs, falling investment demand, and recycled foreign surpluses fueling an excess of savings over investment. Today, those factors are reversing as considerations such as building resilient supply chains ("onshoring" and "friend shoring") are prioritized over cost. As well, heightened geopolitical conflict increases defense spending, further driving up investment demand. The energy transition leads to a large increase in investment demand to deal with damages from climate change and investments in green infrastructure relative to the pre-COVID era.

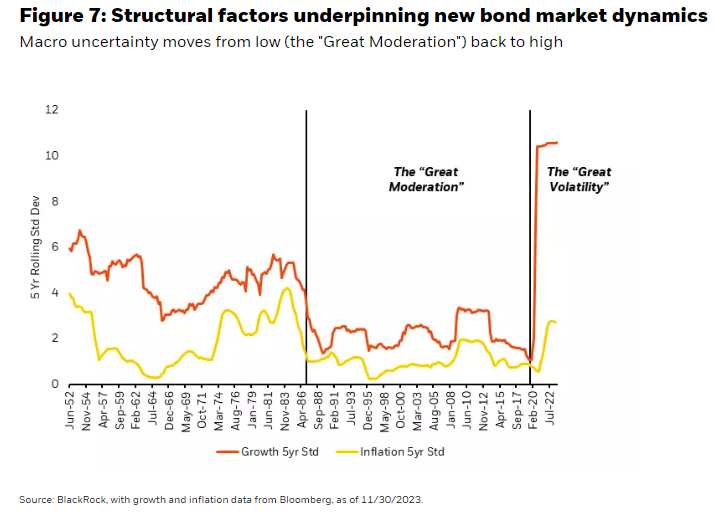

Business cycle. Business cycle volatility may be increasing in a departure from the post-2000s “Great Moderation.” Recovery from the 2008 Global Financial Crisis (“GFC”) balance sheet recession led to private capital excess savings over investment to repair balance sheets even at zero and negative interest rates, a process not likely repeated this cycle. Catch-up Capex following this decade of under investment and balance sheet repair and funding the growing deficits from aging populations all increase investment demand relative to supply—potentially further increasing investors’ compensation for term and inflation premia relative to pre-COVID.

A “new” conundrum for bonds?

The combined impact of all those factors might lead to what we’ll call the potential for a new conundrum for bond investors. Recall the old conundrum, coined by then Fed Chair Greenspan during the 2004-2005 hiking cycle at his February 2005 Humphrey Hawkins Congressional Testimony: “The broadly unanticipated behavior of world bond markets remains a conundrum… Long term interest rates have trended lower in recent months even as the Federal Reserve has raised the level of the target Federal Funds Rate by 150 basis points. This development contrasts with most experience, which suggests that, other things being equal, increasing short term interest rates are normally accompanied by a rise in longer term yields.”

Today of course, the conditions are reversed. The Fed is broadly expected to cut rates in 2024, and long term interest rates are broadly expected to follow those cuts lower as well. However, the potential for the above outlined factors to assert themselves may lead to lagging declines in long term rates and even the potential for “conundrum” type behavior—where long term rates move higher even as the Fed lowers short term policy rates.

Now the first scenario where declines in longer term rates are less than the declines in shorter term rates could be considered “normal.” Indeed, this expected “steepening” of the yield curve is the consensus view for 2024. But a “twist steepening”—where short term rates fall but longer-term rates rise—would be more of a conundrum as it would be at odds with both expectations and historical experience. However, it is precisely for the structural reasons outlined above that bond market performance may not move in line with historical experience.

Additionally, when we think about the three types of rate cuts as outlined in the first section (maintenance, calibration, recession), these may have very different implications for the behavior of the long end of the curve. Maintenance cuts particularly have the greatest potential to exhibit “conundrum” curve behavior as these cuts reflect falling inflation without a decline in growth. Under such a scenario, the anticipated benefits from longer duration might fail to be realized. This would mean less demand for portfolio flows to drive long term rates lower—one of the key factors outlined as a structural source of past bond market long end outperformance.

Under calibration (economic slowing leading to cuts) or recession-induced cuts, we might expect more of a return to “normal” bond market behavior of long end outperformance. While not a conundrum of rising rates, this outcome would still frustrate market consensus outlooks for outperformance in the front end of the curve. Indeed, that market consensus positioning (and its unwinding under this scenario) might contribute to flattening curves under calibration or recession scenarios.

But there are other scenarios as well to consider. Most importantly, inflation failing to fall as far as consensus expects. Such a scenario would undermine rate cut expectations and consensus positioning for both long duration and steeper curves. Such expectations have become consensus and embedded in market pricing because the inflation data has validated the “immaculate disinflation” narrative where inflation falls without significant labor market or economic weakness.

Taking the other side of the consensus recession views in 2023 proved to be correct. Taking another contrarian view in 2024 (but this time towards the bearish side) will be correct again if the current inflation trajectory fails to hold.

The current market consensus for 2024 expects normalizing growth and fading inflation to underpin an optimistic case for financial returns as recession is averted, inflation proves transitory, and a soft-landing fuels Fed rate cuts. How could that go wrong? If the current inflation trajectory fails to hold from sticky services inflation and less goods deflation. And stronger than expected growth that holds up inflation expectations could further undermine both expectations for Fed cuts and consensus expectations for financial market returns in 2024.

Implications for investors

Post-COVID structural economic and financial changes may lead to lagged declines (or even increases) in long term rates relative to short term rates as cuts take place. In this “new” regime for bond investors, investors may find better risk-adjusted performance and diversification potential in shorter maturity bonds relative to longer maturities—particularly if a soft-landing economic scenario plays out. Investors may also consider adding sources of defensive alpha that take advantage of today’s more volatile and higher rate regime to seek uncorrelated, diversifying returns that can help build portfolio resiliency amid uncertainty.

Conclusion

The market consensus expectation for rate cuts comes with the expectation of a return to pre-COVID bond market dynamics characterized by long-end outperformance and a consistently negative stock-bond correlation.

The narrative that “bonds are back” is rooted in history and “old” bond market dynamics that support declining long term rates during Fed cutting cycles. But like the Mark Twain quote on statistics suggests, past examples aren’t always illustrative of what’s to come.

In the post-COVID era, the impact of structural changes in the economy and financial markets may not be fully appreciated by the consensus outlook for bonds. Changes across global economics, monetary and fiscal policy, as well as financial considerations such as debt issuance and portfolio hedging are contributing to persistently higher interest rates and term premia. This has the potential to limit declines in longer maturity bonds as rates are cut, or even cause long term rates to rise—especially if the consensus view for a soft landing plays out and leads to “maintenance” cuts.

When considering the outlook for bonds, the effects of a structurally different economic and market backdrop may be shaping a “new” regime for bond investors that calls for a different playbook than past cycles.

1 Source: Blanchard, Olivier; Galí, Jordi (2007). "Real Wage Rigidities and the New Keynesian Model" (PDF). Journal of Money, Credit and Banking. 39 (1): 35–65. doi:10.1111/j.1538-4616.2007.00015.x

This material is prepared by BlackRock and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of December 2023 and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any of these views will come to pass. Reliance upon information in this material is at the sole discretion of the reader. This material is intended for information purposes only and does not constitute investment advice or an offer or solicitation to purchase or sell in any securities, BlackRock funds or any investment strategy nor shall any securities be offered or sold to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction.

Stock and bond values fluctuate in price so the value of your investment can go down depending upon market conditions. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. The principal on mortgage- or asset-backed securities may be prepaid at any time, which will reduce the yield and market value of these securities. Obligations of US Government agencies and authorities are supported by varying degrees of credit but generally are not backed by the full faith and credit of the US Government. Investments in non-investment-grade debt securities (“high-yield bonds” or “junk bonds”) may be subject to greater market fluctuations and risk of default or loss of income and principal than securities in higher rating categories. Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

Index performance is shown for illustrative purposes only. Indexes are unmanaged and one cannot invest directly in an index.

Investing involves risk, including possible loss of principal

©2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are trademarks of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits