Three 2023 Lessons We Carry Into 2024

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- We think 2023 stressed the value of adapting to a new volatile macro regime, and leveraging investment insight and structural forces to find opportunities.

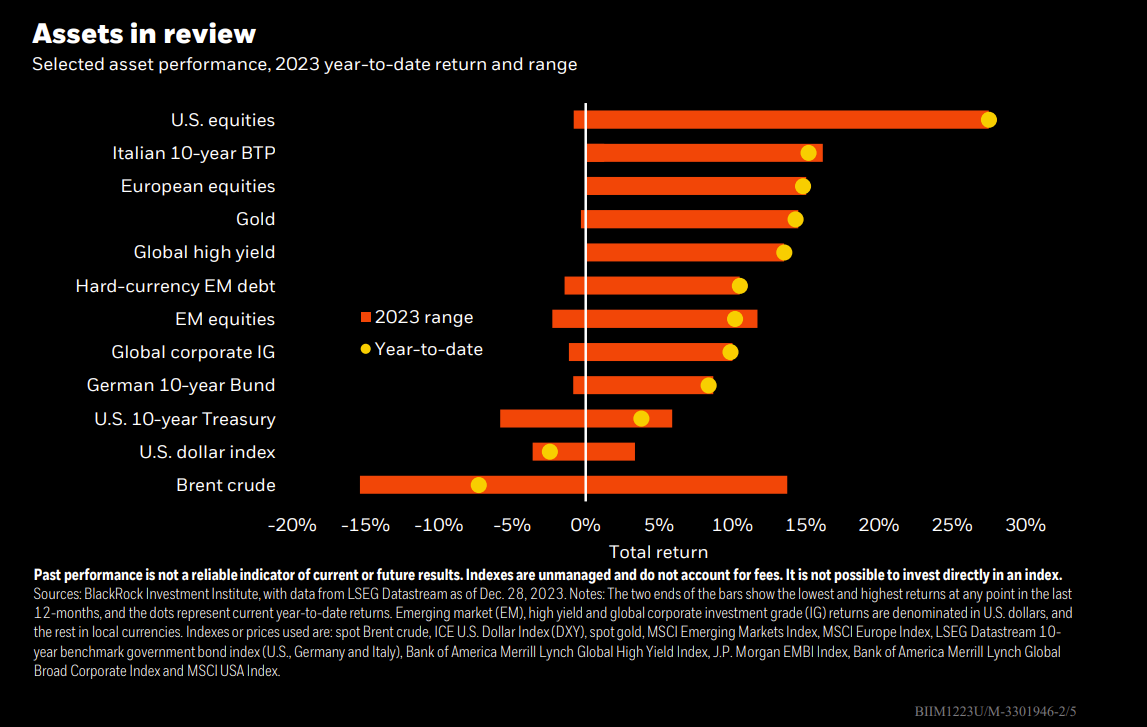

- U.S. stocks surged in 2023, a reversal from their 2022 underperformance. Flipflopping market views about the policy path stoked volatility in long-term bonds.

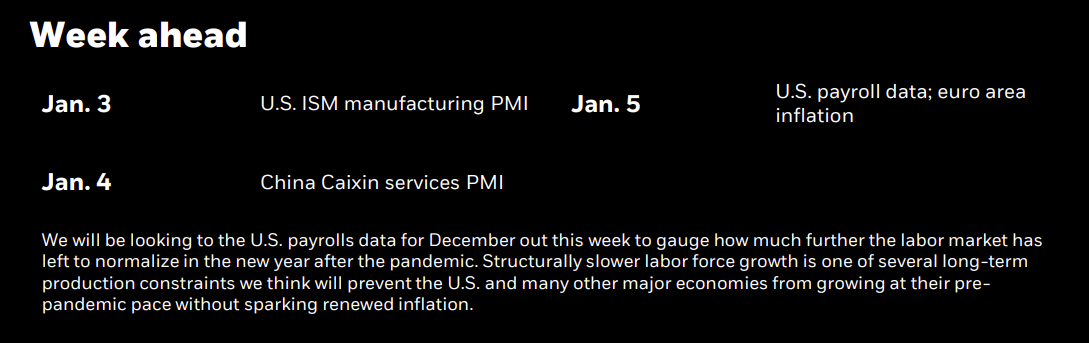

- December U.S. jobs data out this week should signal how much more the labor market needs to normalize. Slower jobs growth is a long-term supply constraint.

We take three lessons from 2023 to shape our investment approach in the new year. First, markets flipflopping between macro narratives does not reveal new information about where we will end up. This is not a typical business cycle and context is everything. Second, greater dispersion is creating opportunities. That requires skill and granularity. Third, artificial intelligence buzz has underpinned U.S. stock performance – and shows mega forces matter now, not just in the future.

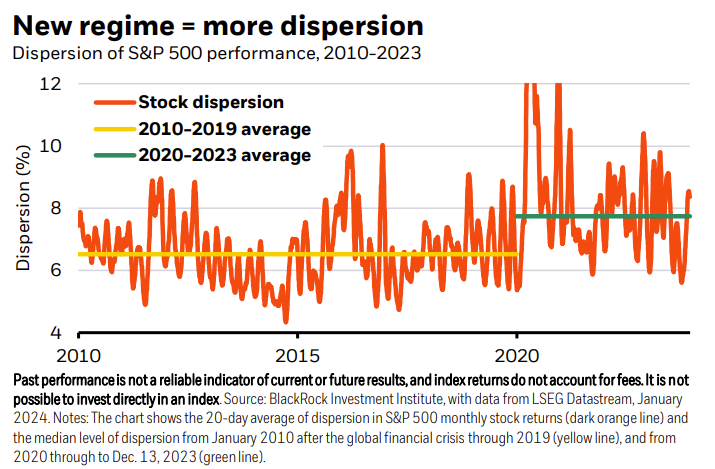

Looking back, 2023 largely saw a concentrated tech stock rally, with the Nasdaq up 55% from 2022. A market-wide rally since November also supported tech and led the equal-weighted S&P 500 to eke out a 12% return. Overall, we are seeing more dispersion in individual stock returns since 2020 (green bar in the chart). Macro uncertainty, geopolitics and structural shifts are driving volatility and dispersion. We think markets have stoked volatility, too, by viewing the new regime through the lens of a typical business cycle. Investors leaned into long-term bonds in early 2023 on hopes the Federal Reserve would cut policy rates by year end. It then became clear higher government spending and labor shortages are set to make inflation persistent and keep interest rates above pre-Covid norms. Ten-year Treasury yields surged to 16-year highs near 5% in October as markets priced in this outlook. They tumbled back below 4% by year end after the Fed blessed the pricing of rate cuts.

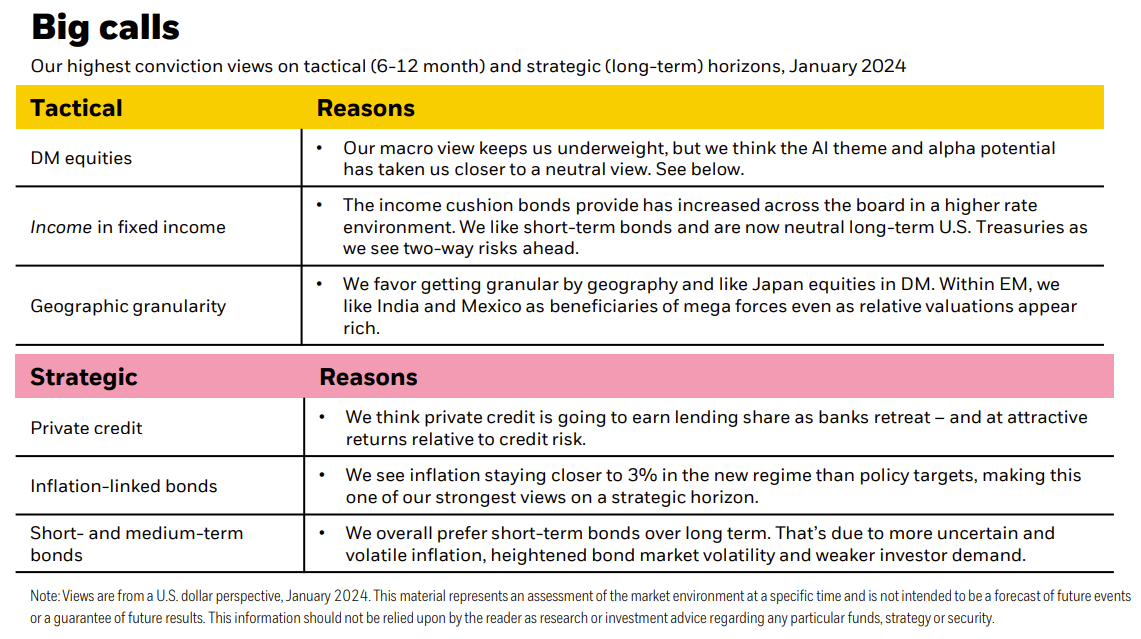

These volatile moves underscore the first lesson that was reinforced in 2023: The macro backdrop is much more uncertain today than during the Great Moderation period of stable growth and inflation. This is tough to navigate for markets, with them flipflopping between macro narratives through 2023. In the final quarter alone, both stocks and bonds surged on news of lower inflation – with the November PCE report confirming a goods-led slowdown – and dovish Fed projections. Small caps rallied on hopes for a soft economic landing. And markets have repeatedly priced in aggressive rate cuts just to walk them back. All this shows markets may extrapolate a lot from one piece of data or central bank comment. That’s taking a big bet on the macro outlook when the range of outcomes is wide, in our view. We don’t believe the prevalent market narrative tells us new information about where the macro will end up. Yet we are cognizant markets can run with a narrative for some time. This is why we turned tactically neutral on long-term U.S. Treasuries last October. We think long-term yields will resume their rise over time as investors demand more compensation amid persistent inflation and budget deficits.

The greater macro risk means the dispersion of returns has increased. The result: a wide divergence in performance across equity sectors – and greater opportunities for investment expertise to shine, in our view. The correlation between bond and stock returns has flipped firmly into positive territory, meaning stocks and bonds fall or rise simultaneously. As a result, the old approach to portfolio construction that relied on bonds to offset equity sell-offs won’t work, in our view. Instead, we advocate breaking up broad asset allocation blocks and digging deeper. All this is why our second lesson is that granularity is more essential now. We look beyond the macro to seek above-benchmark returns, or alpha, by being dynamic and selective.

One example of going beyond broad asset class exposures is to harness mega forces. The artificial intelligence (AI) mega force drove 2023 stock performance to an even larger extent than we had imagined. The importance of AI and other mega forces hammers home our third lesson: Structural forces matter now. Aging populations mean an ever-rising share of the population is past retirement age, resulting in worker shortages. That’s a key constraint fueling U.S. inflation now as a tight labor market keeps wage growth elevated. Others include the low-carbon transition and geopolitical fragmentation. The latter is evidenced by wars in Ukraine and Gaza and the intensifying structural competition between the U.S. and China.

Bottom line: 2023 emphasized the macro risks but also the opportunities on offer from structural shifts and getting granular in the new regime. Our 2024 Global Outlook outlines how we capture them.

Market backdrop

U.S. stocks surged roughly 25% last year, a near mirror image of their downtrodden 2022 performance. That was partly driven by excitement over AI lifting tech stocks and carrying the broader market. Meanwhile, the 10-year Treasury yield ended the year where it started: It climbed from lows of roughly 3.3% in April, to 16-year highs near 5% in October before falling below 3.9% at year end. We think some of the sharp swings in narratives – and markets – reflect the new regime of greater volatility.

Tracking five mega forces

Mega forces are big, structural changes that affect investing now – and far in the future. As key drivers of the new regime of greater macroeconomic and market volatility, they change the long-term growth and inflation outlook and are poised to create big shifts in profitability across economies and sectors. This creates major opportunities – and risks – for investors. See our web hub for our research and related content on each mega force.

Tracking five mega forces

Mega forces are big, structural changes that affect investing now – and far in the future. As key drivers of the new regime of greater macroeconomic and market volatility, they change the long-term growth and inflation outlook and are poised to create big shifts in profitability across economies and sectors. This creates major opportunities – and risks – for investors. See our web hub for our research and related content on each mega force.

- Demographic divergence: The world is split between aging advanced economies and younger emerging markets – with different implications.

- Digital disruption and artificial intelligence (AI): Technologies that are transforming how we live and work.

- Geopolitical fragmentation and economic competition: Globalization is being rewired as the world splits into competing blocs.

- Future of finance: A fast-evolving financial architecture is changing how households and companies use cash, borrow, transact and seek returns.

- Transition to a low-carbon economy: The transition is set to spur a massive capital reallocation as energy systems are rewired.

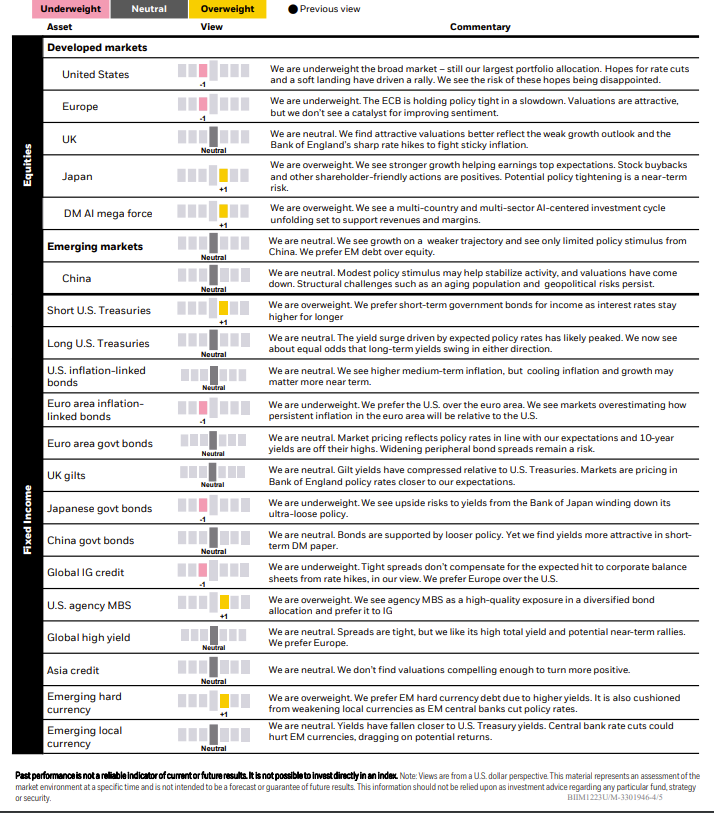

Granular views

Six- to 12-month tactical views on selected assets vs. broad global asset classes by level of conviction, January 2024.

Our approach is to first determine asset allocations based on our macro outlook – and what’s in the price. The table below reflects this and, importantly, leaves aside the opportunity for alpha, or the potential to generate above-benchmark returns. The new regime is not conducive to static exposures to broad asset classes, in our view, but is creating more space for alpha.

BlackRock Investment Institute

The BlackRock Investment Institute (BII) leverages the firm’s expertise and generates proprietary research to provide insights on macroeconomics, sustainable investing, geopolitics and portfolio construction to help Blackrock’s portfolio managers and clients navigate financial markets. BII offers strategic and tactical market views, publications and digital tools that are underpinned by proprietary research.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The opinions expressed are as of Jan. 2, 2024, and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks. This information is not intended to be complete or exhaustive and no representations or warranties, either express or implied, are made regarding the accuracy or completeness of the information contained herein. This material may contain estimates and forward-looking statements, which may include forecasts and do not represent a guarantee of future performance.

In the U.S. and Canada, this material is intended for public distribution. In EMEA, in the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Investment Management (UK) Limited, authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL. Tel: + 44 (0)20 7743 3000. Registered in England and Wales No. 02020394. For your protection telephone calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock. In the European Economic Area (EEA): this is Issued by BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In Italy, for information on investor rights and how to raise complaints please go to https://www.blackrock.com/corporate/compliance/investor-right available in Italian. In Switzerland, for qualified investors in Switzerland: This document is marketing material. Until 31 December 2021, this document shall be exclusively made available to, and directed at, qualified investors as defined in the Swiss Collective Investment Schemes Act of 23 June 2006 (“CISA”), as amended. From 1 January 2022, this document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under art. 4 FinSA, please see the following website: www.blackrock.com/finsa For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign RecognisedCompany registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738). In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorised and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 29th floor, Olaya Towers – Tower B, 3074 Prince Mohammed bin Abdulaziz St., Olaya District, Riyadh 12213 – 8022, KSA, Tel: +966 11 838 3600. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA or any other authority or regulator located in KSA has approved this information. In the United Arab Emiratesthis material is only intended for -natural Qualified Investor as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA or any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, to sophisticated institutions who have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document, does not constitute and should not be construed as an offer of, invitation, inducement or proposal to make an offer for, recommendation to apply for or an opinion or guidance on a financial product, service and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to the Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into accountyour individual objectives, financial situation, needs or circumstances. In New Zealand, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975, AFSL 230 523 (BIMAL) for the exclusive use of the recipient, who warrants by receipt of this material that they are a wholesale client as defined under the New Zealand Financial Advisers Act 2008. In China, this material may not be distributed to individualsresident in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in anyinvestment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

©2024 BlackRock, Inc. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: The crypto landscape is on the brink of a revolution. Are you prepared for what's coming in 2024? Dive into expert insights on the future of crypto and its influence on next year's market. Join us at the Crypto Symposium on January 12th at 11 am ET. Click here to register.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All