Markets in 2023 kept investors on the edge of their seats. Groundbreaking technological advancements, mega-popstars being blamed for summertime inflation, and a December Fed pivot were just a few of the plot twists. We reflect on three macro developments that defied market expectations and share some of the questions that are top of mind as we turn our attention to 2024:

1. What US landing?

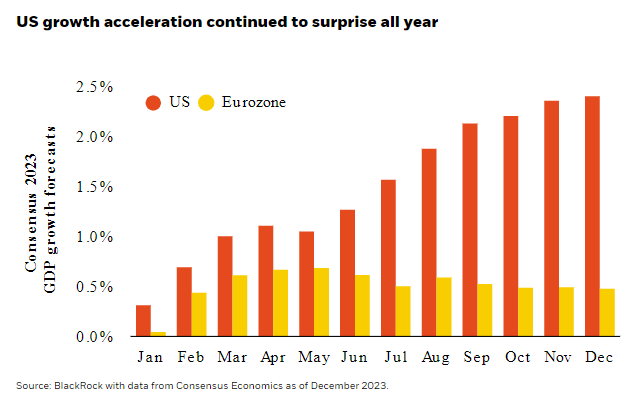

The widely debated “hard landing vs. soft landing” for the US economy turned out to be no landing – or maybe even a takeoff. US GDP growth sequentially accelerated all year and continually outpaced expectations. Upside revisions also diverging meaningfully from growth in Europe, which remained more tepid and in line with expectations. US consumers and corporates shrugged off higher policy rates and Uncle Sam chipped in with big fiscal incentives through the Inflation Reduction Act (IRA) and CHIPS Act. High real rates didn’t dampen real activity and final demand accelerated throughout the year despite manufacturing being in the doldrums.

2. What liquidity crunch?

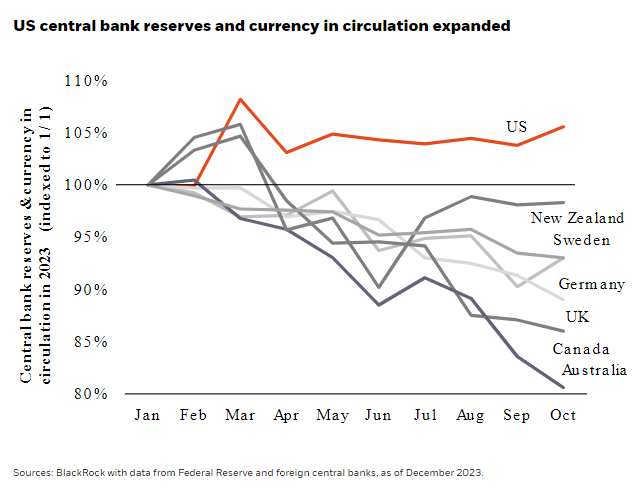

In January 2023, the market expected US policy rates to end the year under 4.5%, as indicated by Fed Fund futures. Instead, the Federal Reserve went on to hike interest rates four more times before pausing at 5.25%. But that wasn’t the only monetary policy surprise. Despite continuing to hike, the Fed actually expanded liquidity in the spring and summer of 2023 on the back of concerns that that failure of Silicon Valley Bank would trigger a credit tightening. US liquidity was the outlier relative to other countries that deployed a broader range of monetary policy tightening tools, and this contributed to strong US equity returns.

3. What China reopening?

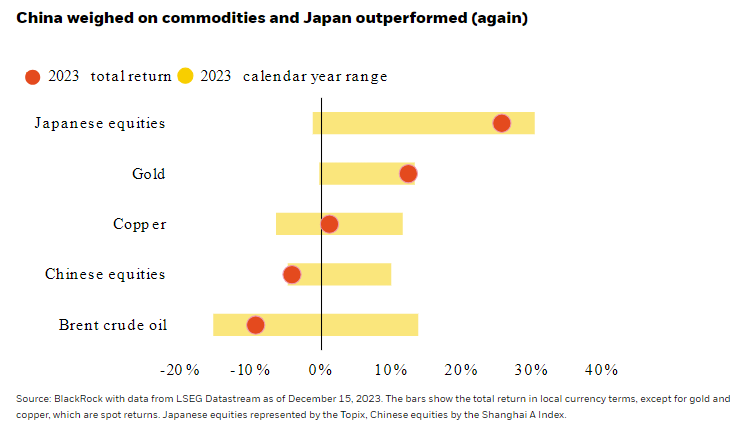

The global demand boom that was anticipated to accompany the end of Chinese COVID lockdowns in early 2023 never materialized. Instead, continued challenges in the property sector and muted consumer demand meant that China slipped back into deflation. Tepid Chinese demand weighed on commodity and global goods prices throughout the year. In a story of contrasts and a reversal of roles, Japan’s reflation party that began in 2022 kept strengthening throughout 2023. Japanese stocks outperformed most other major markets for the second year in a row while divergence in inflation expectations between Japan vs. China created opportunities for fixed income investors.

Looking Ahead:

As we look ahead to 2024, we expect the regime of greater macro dispersion and elevated market volatility to persist. In particular, we view positive stock-bond correlation as a market feature that is likely to remain so long as core inflation remains above target. As we seek to capture opportunities across countries in stock and government bond markets, key questions we are focused on include:

- Is the inflation beast really slayed? Though markets and policymakers both want it to be true, we think getting services inflation closer to target in 2024 might prove harder than the goods deflation of 2023. In our portfolios like the Tactical Opportunities Fund, we remain short duration as the yield curve inversion makes cash more attractive compared to long bonds on a tactical horizon.

- Is US dollar past its peak? Though fiscal concerns have receded in the closing months of 2023, the magnitude and unsustainability of the US twin deficits (government budget and current account) could exert downward pressure on the US$ in 2024; particularly if the Fed eases the policy rate outlook. We have been extending our short US dollar position in the portfolio.

- Is Europe a bargain? The bar is low, but we are optimistic on European earnings growth. Clear signs of a stabilization in the manufacturing sector, continued wage growth, and a very high savings rate could provide a tailwind for European consumers in 2024. We like peripheral European markets like Italy and Spain.

Carefully consider the investment objectives, risks, charges and expenses of the funds carefully before investing. The prospectuses and summary prospectuses contain this and other information about the funds and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

Important risks: The fund is actively managed and its characteristics will vary. Stock and bond values fluctuate in price so the value of your investment can go down depending on market conditions. International investing involves special risks including, but not limited to political risks, currency fluctuations, illiquidity and volatility. These risks may be heightened for investments in emerging markets. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Asset allocation strategies do not assure profit and do not protect against loss. The fund may use derivatives to hedge its investments or to seek to enhance returns. Derivatives entail risks relating to liquidity, leverage and credit that may reduce returns and increase volatility.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

©2024 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock