January update

- Municipal bonds posted negative total returns as the market reassessed macro expectations.

- Seasonal supply-and-demand dynamics were supportive, albeit less so than in prior years.

- We maintain some caution until absolute and relative valuations are more attractive.

Market overview

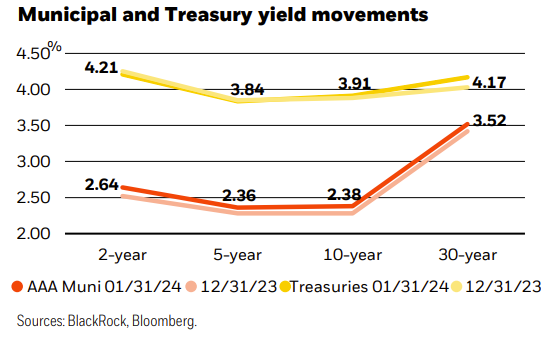

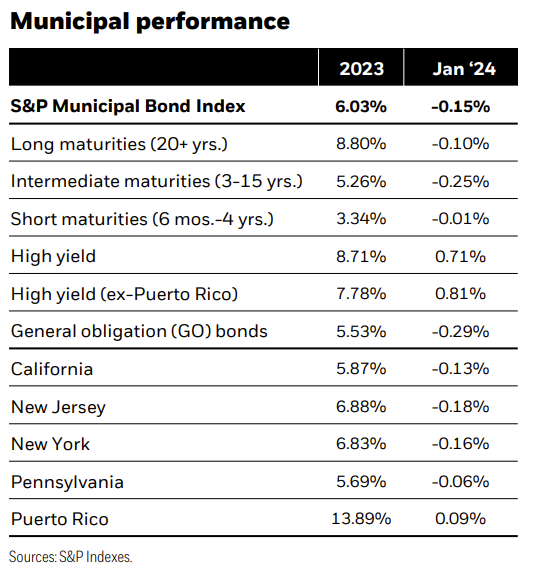

After posting the strongest performance since the mid1980s during the fourth quarter of 2023, municipal bonds took a breather in January. The asset class produced modestly negative total returns amid a macro-backdrop that generally unfolded as anticipated (see our 2024 Municipal Market Outlook). Economic growth remained firm and continued to eclipse projections, causing the market to reduce forward expectations for monetary policy easing, both in timing and in magnitude. As a result, the Treasury curve steepened with front-end rates falling and back-end rates rising. Given rich valuations, municipals modestly underperformed comparable Treasuries, and the S&P Municipal Bond Index returned -0.15%. Shorter-duration (i.e., less sensitive to interest rate changes) and single-A rated bonds performed best.

Supply-and-demand dynamics were supportive to start the year but provided a more muted seasonal tailwind than in prior years. Issuance increased to $32 billion in January, 16% above the five-year average. Despite the pickup, supply was still outpaced by reinvestment income from maturities, calls, and coupons by $2 billion. Consequently, issuance was easily absorbed with deals oversubscribed 4.7 times on average, above the 4.3 times average in 2023. At the same time, mutual fund flows turned consistently positive, benefiting from the end of seasonal tax loss harvesting. However, the moderate pace of inflows indicated continued caution from investors.

We believe that persistent economic strength, patience from the Federal Reserve, and weakening seasonal supply-anddemand dynamics could spur better valuations later in the quarter. Thus, we maintain near-term caution, but would view any material sell-off as a buying opportunity.

Strategy insights

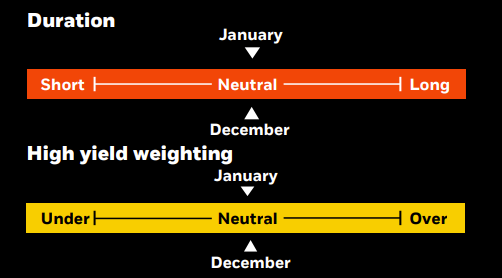

We favor a neutral duration posture overall. We continue to advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15 - 20-year part of the curve. We prefer lower-rated investment grade credits, but think high yield offers an attractive risk-reward opportunity, given favorable structures and the ability to generate alpha through security selection.

Overweight

- States that primarily rely on consumption taxes

- Essential-service revenue bonds

- Flagship universities

- Select issuers in the high yield space

Underweight

- States overreliant on personal income taxes, especially California Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

- Senior living and long-term care facilities

- Lower-rated private universities

- Stand-alone and rural health providers

Credit headlines

New York City: Mayor Adams proposed a $109.4 billion fiscal year (FY) 2025 budget that closes an initial $7 billion gap through better-than-expected revenues, reductions in migrant costs, and draws on historically high reserves. Outyear budget gaps for FYs 2026 - 2028 are projected to range from $5 - $6 billion annually, lower than the $7 - $8 billion gaps estimated for the last two fiscal outyears in the June 2023 financial plan. Despite improved projections, the city faces fiscal challenges, including economic conditions, the post-pandemic health of the commercial real estate (CRE) market, and the influx of migrants. While CRE is 45% of the city’s assessed value, the CRE portion of property taxes is only about 13% of government fund revenue. In addition to spending cuts, a diverse revenue mix, including personal income, sales, business, and other miscellaneous tax and revenue sources, gives the city flexibility in meeting its legal obligation to balance budgets

Jefferson County, AL: After gaining notoriety as the largest municipal bankruptcy when it filed in 2011, Jefferson County sold $2.2 billion in sewer system bonds to refinance debt that was issued as part of a plan to exit court protection. With investment grade triple-B category ratings, the county’s fiscal recovery speaks to the resilience of government issuers in the municipal market. The bonds continue to attract positive investor interest, with the 10- year maturity yielding 3.08% on February 1, a 20 basispoint tightening from its January 22 low.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of January 7, 2024, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2024 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

More Fixed Income Topics >