Productivity will be a catalyst for further disinflation.

Contestants on the game show The Price Is Right get a chance to compete for prizes by guessing the prices of various consumer goods. The winner is the one whose guess comes closest to the actual price, without going over. In that game, it is better to err on the cautious side than be disqualified for going too high.

Economic forecasters (ourselves included) must have watched The Price Is Right at a formative age. Over the past two years, we have had to revise a lot of numbers upward: the Fed hiked rates more than we expected, inflation has been sticky and growth has far exceeded expectations.

Last week’s employment report repeated that pattern. Against expectations of moderation, the report showed a stunning 353,000 jobs created, plus upward revisions to prior months. The unemployment rate held at the very low level of 3.7%.

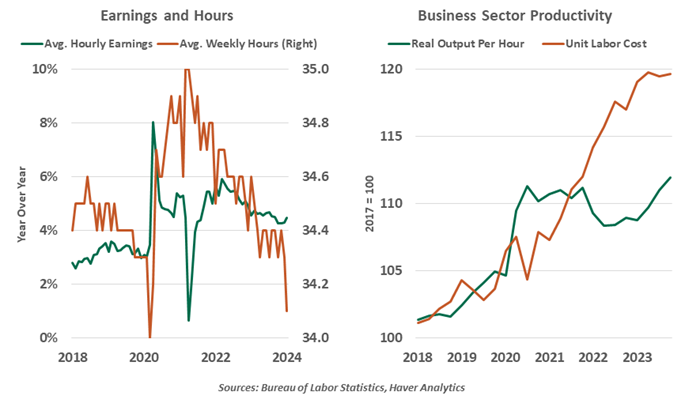

Average hourly earnings showed a surprising acceleration to 4.5% year over year. Service sectors like education, healthcare and transportation saw the largest monthly gains, while goods-producing occupations were more temperate. We are somewhat sensitive to wage growth for the inflationary risk it poses; at last week’s Federal Open Market Committee press conference, Chair Jerome Powell cited limited improvement in services inflation as a reason to hold rates higher for longer.

The average workweek for all employees fell to a post-pandemic trough of 34.1 hours. That reading was lower than any value seen between 2010 and 2019. Aggregate weekly hours (the sum of all hours worked) dipped by over 10 million hours (-0.3%) from December, its largest decline since early 2022. This leads to suspicion of labor hoarding, with employers disinclined to let people go; instead, they cut costs by reducing hours.

Some of the decline could be seasonal. While the Bureau of Labor Statistics makes adjustments for routine seasonal shifts, January 2024 featured more bouts of very cold weather than normal, spread across an abnormally wide swath of the country. When normally temperate regions encounter a layer of ice or snow, commerce comes to a halt. Over a half million workers were employed but not at work due to bad weather, the highest for any January since 2011. Tellingly, nonsupervisory employees in the utilities sector stood out for having an upward shift in hours; in extreme weather, they were more essential than ever.

MORE PRODUCTIVE WORKERS SHOULD EARN HIGHER WAGES

These disparate developments can be difficult to reconcile. Payrolls are growing; job openings are elevated; layoffs are limited; wages are gaining. However, the labor force is declining and hours worked are falling. How can we make sense of these readings?

Productivity ties it all together: Workers can work less time and be paid more if they are more productive. Wages are payment for the value a worker provides to a business. When workers contribute more, their wages should rise.

Business sector productivity has been another upward surprise in the economic data, rising 2.7% year over year in the fourth quarter of 2023. Unit labor costs, essentially wages per unit of output, grew 2.2%. Output per worker is up 2% on the year, even as hours worked were nearly flat over the same interval.

Additionally, the Great Resignation has concluded. Recent readings of the Job Openings and Labor Turnover Survey show the rates of workers changing jobs have returned to their pre-pandemic norms. Climbing the learning curve impairs productivity, but it is less of a challenge now.

Human capital gains are essential to an economy with aging demographics and a constrained supply of workers. Technological advancements may help maximize worker output, including investments in artificial intelligence (AI). When earnings rise due to higher productivity, the result raises less of an inflation risk. Better productivity and more stable hiring will be key for inflation to come on down.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust