The Surge In Bitcoin ETFs And Its Potential Impact On Gold

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsBitcoin and gold were both top of mind at this past week’s 2024 Investment U Conference in Ojai, California, which I had the privilege of presenting at. There was a rumor circulating that the Bitcoin price rally was sparked by a large financial institution recommending a 2% to 3% weighting to some of its high-net-worth clients. I can’t confirm this, but it’s being reported that Bank of America and Wells Fargo are now offering the Bitcoin ETFs to certain wealth management clients, joining Charles Schwab, Robinhood and others.

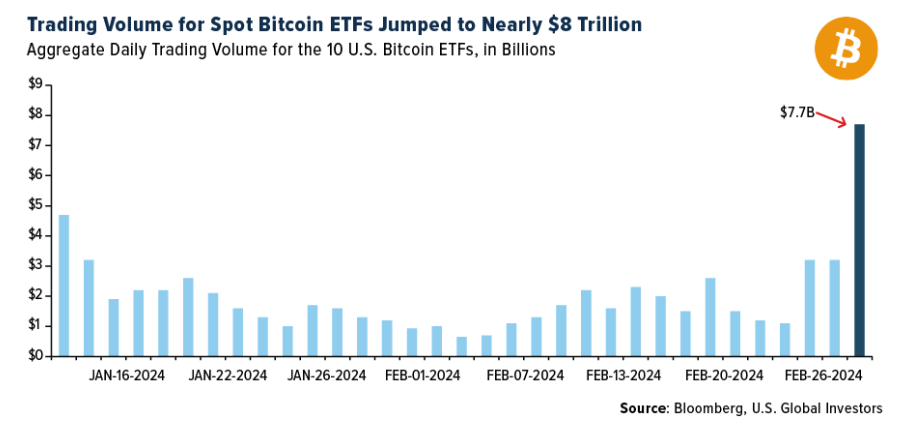

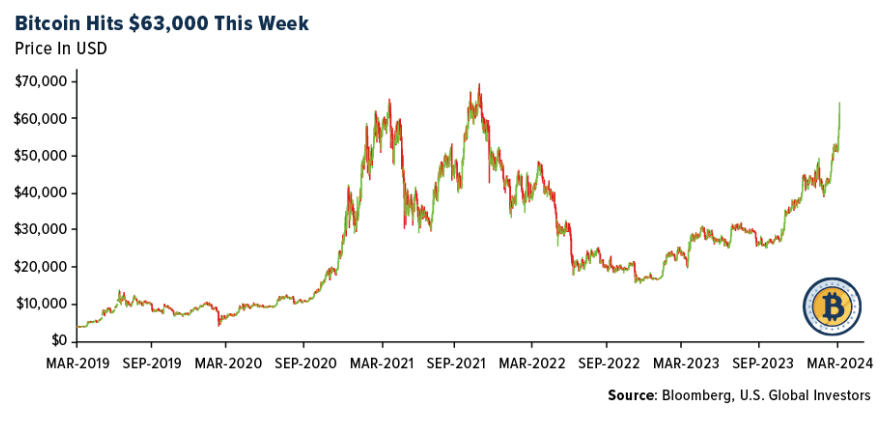

The price of Bitcoin pumped more than 45% last month, with around half of those gains recorded in the final week, as demand for the long-awaited spot Bitcoin ETFs hit a fever pitch. Combined daily trading volume for the 10 ETFs was a jaw-dropping $7.7 billion on Wednesday alone, fueled by institutional speculation and leveraged bets that pushed the price of the underlying asset to a near-record high.

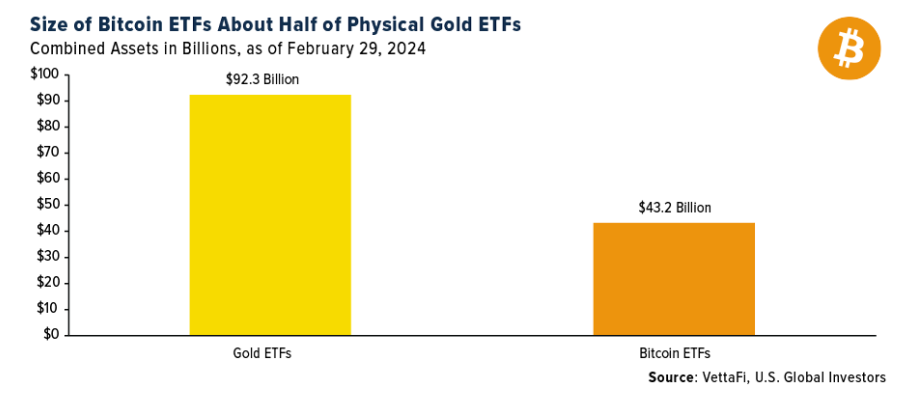

Remarkably, as of February 29, the combined value of the holdings in U.S.-based Bitcoin ETFs was roughly half the value of all known gold ETFs. The Bitcoin ETFs, which began trading in January, held $43.2 billion, while gold ETFs held $92.3 billion.

The cryptocurrency’s breathless catch-up to gold is reflected in the dramatic difference in sentiment between the two assets right now. CoinStats’ Crypto Fear and Greed Index is currently flashing Extreme Greed, while JM Bullion’s Gold Fear and Greed Index sits in Neutral territory.

A Tale Of Two Assets: Risk And Reward

As you know, I often recommend a 10% weighting in gold, with half in physical gold (coins, bars, jewelry) and the other half in high-quality gold mining stocks, mutual funds and ETFs. I believe this weighting is suitable for most investors seeking a non-correlated asset, but especially conservative investors who might not have a long-term investment horizon.

For investors with a longer horizon, or those with a bigger risk appetite, there’s Bitcoin, whose volatility is about eight times greater than that of gold, its analog cousin. Whereas the precious metal has a 10-day standard deviation of ±3%, Bitcoin’s is ±25%.

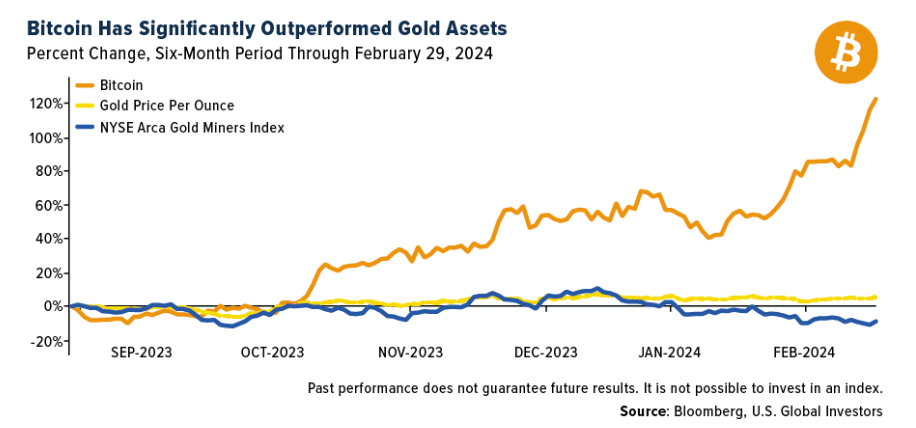

Though not guaranteed, with greater risk can come greater reward. For the six-month period through the end of February, Bitcoin more than doubled in price, surging close to 130%. Over the same period, gold increased a little over 5% while gold majors, as measured by the NYSE Arca Gold Miners Index, lost 9%.

Whether the excitement surrounding Bitcoin is siphoning flows away from gold is unclear, but there does appear to be some disconnect between gold’s price action and investment levels. Historically, the gold price and holdings in gold-backed ETFs have traded in tandem, but starting in 2023, the two began to decouple, as you can see below. This could be caused by a number of factors, including changes in investor sentiment, monetary policy, portfolio balancing, currency fluctuations and more.

Gold Was Up, But Most Miners Couldn’t Grow Free Cash Flow

Analysts here at U.S. Global Investors looked at a basket of 85 gold mining stocks and found that, generally speaking, financial conditions worsened for the industry in 2023, despite the fact that gold had a relatively good year, jumping more than 13%.

Our analysis shows that, of those 85 names, only 47—or 55% of the basket—reported a positive free cash flow (FCF) yield as of December 31, 2023. That’s little changed from a year earlier, when 48 gold producers had positive FCF.

The same concerning results surfaced when we compared sales growth to changes in the price of gold. In December 2022, 23 out of 85 gold miners had positive FCF as well as sales growth that outpaced the yellow metal over the trailing 12 months (TTM); a year later, that figure fell to 10, representing only around 12% of the basket.

This means that fewer than one in 10 gold miners recorded an improvement in financial conditions…during a year when the price of gold was up.

For this reason and more, younger people just haven’t shown interest in gold stocks, which is a shame for the companies. We’re on the verge of history’s greatest transfer of wealth, with $84 trillion expected to be left to heirs over the next two decades. Perhaps producers should take a page out of Bitcoin miners’ playbook and HODL their gold.

Will Central Banks Start Buying Bitcoin?

As I shared with you, some market watchers, including our shop, have noted that the driver of the gold price appears to have shifted in recent months. For decades, the yellow metal had an inverse relationship with real rates—rising when yields fell, and vice versa—but since the start of the pandemic in 2020, this pattern has broken down. During the 20 years before the pandemic, gold and real rates shared a highly negative correlation coefficient. Since that time, though, the correlation has turned positive, and the two assets now move in the same direction more often than not.

BMO Capital Markets commented on this in January, making the case that buying activity by central banks is the new driver of gold. It’s hard to argue against this position. Financial institutions, chiefly those in emerging economies, have been net buyers of the metal since 2010 in an effort to support their currencies and diversify away from the U.S. dollar.

For what it’s worth, Edward Snowden shared his 2024 prediction this week that a national government will be found to have been secretly buying Bitcoin, “the modern replacement for monetary gold,” the former NSA whistleblower said in a tweet.

This would be something, though I should point out that the government of El Salvador currently holds 2,381 bitcoins in its treasury. Its president, Nayib Bukele, says these holdings are up 40% after the recent price rally, and yet he has no intention of selling. El Salvador and the Central African Republic (CAR) are the only two countries so far that have made Bitcoin legal tender.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.11%. The S&P 500 Stock Index rose 0.95%, while the Nasdaq Composite climbed 1.74%. The Russell 2000 small capitalization index rose 2.87% this week.

- The Hang Seng Composite lost 0.71% this week; while Taiwan was up 0.25% and the KOSPI fell 0.96%.

- The 10-year Treasury bond yield fell 6 basis points to 4.183%.

Airlines And Shipping

Strengths

- The best performing airline stock for the week was Embraer, up 14.5%. According to ISI, for the week, passenger throughput was up 6% year-over-year on positive 2% year-over-year capacity. The group continues to see favorable supply-demand driving estimated load factor improvement in February. Airline web traffic was up 4% year-over-year for the week, compared to up 4% year-over-year in the trailing four-week period.

- JPMorgan believes the impact of continued Cape of Good Hope rerouting could largely absorb new ship supply in 2024. The group expects freight rates to fall in the slow season from February, but also expect protracted Red Sea impact; tonnage supply/demand could remain tight until tonnage shortages are eliminated. Roughly 15% of global containership routes used to go through the Suez Canal, but these have all been rerouted around the Cape of Good Hope, and as voyage times have risen around 30%, this appears to have absorbed about 5% of tonnage supply.

- The Airline Industry Group RAA noted a shortfall of 968 pilots in 2023 versus a more severe shortfall of 3,637 in 2022. The group expects this dynamic to improve further in 2024. RAA notes that with a shortage of at least 4,605 pilots, 400 aircraft were parked, and 14%/50% of the eligible pilot workforce must retire within five to 15 years.

Weaknesses

- The worst performing airline stock for the week was Air Transport Services, down 13.3%. Canadian ULCC Lynx announced it ceased operations on Monday, February 26, based on first quarter/second quarter 2024 schedules (seats), Lynx accounts for 2.1%/3.5% of domestic, 1.9%/2.0% of Transborder, and 0.5%/0.9% of Canada-Mexico.

- According to Morgan Stanley, war-risk premiums may have increased by as much as 900% since the Houthi attacks on shipping in the Red Sea began. This is one of several troubling predictions in a United Nations Conference on Trade and Development (UNCTAD) report released yesterday. UNCTAD said that, according to some sources, from below a level of 0.1% of the value of a vessel, during the final weeks of last year, war-risk premiums had jumped to as much as 1% of vessel value by the start of this month. Meanwhile, journeys through the Suez Canal this year have dropped 42%, year-on-year, and via Panama by 49%, noted UNCTAD.

- According to Bank of America, although Volaris´ revenue beat their forecast by over 5%, EBITDAR missed estimates by 3% and adjusted EBIT by 4%. This was driven by a mix of TRASM (total revenue per available seat mile) 5% above their numbers, mainly driven by strong ancillary revenue, and operating expenses 7% above their estimates, (mainly explained by higher maintenance, landing/take-off fees, and other operating expenses).

Opportunities

- Bloomberg is reporting that Air China is considering increasing its 29.99% stake in Cathay Pacific (“CX”). Discussions are reportedly in early stages with no announcement or comment from Air China. They note that any increase in Air China holding above 30% would trigger a general offer under the HK Takeover Code, while Swire under the CX Shareholders Agreement would have to consent to any additional stake increase. Air China taking an increased stake in CX could increase cooperation including alliances and network integration and could also help CX manage Chinese regulatory and customer risks.

- According to JPMorgan, Yangzijiang Shipbuilding (‘YZJ’) recorded its strongest net profit to date in fiscal year 2023 (FY23), which is an 8% beat to the bank’s estimate. Its record profitability was led mainly by solid expansion in shipbuilding margins (22%). Additionally, YZJ’s orderbook is set to further strengthen with a 50% uplift in 2024 new order guidance. YZJ’s strong net cash also offers headroom for higher fiscal year 2024 dividend payout with low FY23 payout attributed to YZJ’s cash conservation for future growth initiatives.

- Air Canada announced it will cap fares and add over 6,000 seats on select routes operated by Lynx Air, in response to Lynx Air’s suspension of operations starting February 26, 2024. This move aims to offer affordable travel options for Lynx Air customers affected by the shutdown, covering travel within Canada, to the U.S., and to Cancun, Mexico. These special fares are for purchase before February 26 for travel up to April 2, encompassing the March Spring break and Easter holiday.

Threats

- According to JPMorgan, Japan Air Lines’ international route unit price was up 73% versus 2019 in the first half of 2023 and up 76% in the third quarter. This reflects increases versus 2019 of 27 points from net unit price, 38 points from market impact, and 8 points from route mix. High unit prices were supported by a good supply/demand environment, but in the fourth quarter, it seems likely that supply-demand will ease somewhat in North America and China, so the bank expects the increase in fourth quarter unit prices to be smaller than in the third quarter.

- According to Morgan Stanley, Amazon, USPS, and major retailers have restructured their eCommerce supply chains and transitioned to more short-haul, regionalized models to increase their proximity to end-customers and rapidly improve time-to-serve. This could pressure entrenched Express/Air business models at UPS and FedEx. Their proprietary Alpha Wise data analysis shows that Amazon’s Air network has already embraced this regionalization with length of haul (down 17% from peak) and service airport patterns noticeably changing over the past year.

- Regarding Transat, the new flight attendant deal will see a 30% cumulative pay increase over five years along with other contract enhancements. The union representing the TRZ flight attendants (CUPE) is the same union representing flight attendants at most of Canada’s airlines, including Air Canada, so this new contract probably represents a benchmark for the industry. Air Canada’s flight attendants see their contract up for renewal in March 2025.

Luxury Goods And International Markets

Strengths

- Cruseliners gained this week after Norwegian Crusie Line Holdings reported a fourth-quarter 2024 earnings miss, but projected strong sales in the current quarter due to robust demand. Shares gained more than 10% on Tuesday, lifting its competitors as well. For the week, Norwegian Crusie Line Holdings gained 19.9%, Carnival 4.1%, and Royal Caribbean 1.2%.

- Prices are declining in Europe, heading towards the 2% target set by the European Central Bank (ECB). Year-over-year CPI was reported at 2.6% in February, down from 2.8% in Januray. Core inflation declined from 3.3% in the previous month to 3.1% by the end of February.

- RealReal Inc. was the best performing S&P Global Luxury stock, gaining 63.8% in the past five days. It is an online platform for re-selling previously-owned luxury items. Shares gained on Friday after the company announced a quarterly earnings beat and set a new strategy to expand the number of current stores from 13 to 30 in the next five years.

Weaknesses

- China manufacturing PMI remains below 50, which separates growth from contraction. The index was reported at 49.1 in February, down from January’s reading of 49.2. However, the Caixin Manufacturing PMI remains in expansionary territory. It was reported at 50.9 for the month of February, above 50.8 that was recorded in January.

- The Eurozone’s economic sentiment dipped in February. Among the largest economies in Europe, sentiment was weaker in Italy and Germany, but improved in the Netherlands.

- Faraday Future Intelligence was the worst performing S&P Global Luxury stock, losing 23.6% in the past five days. This is now a penny stock, with high volatility after losing 99% of its market share last year. Shares closed at 19 cents on Friday.

Opportunities

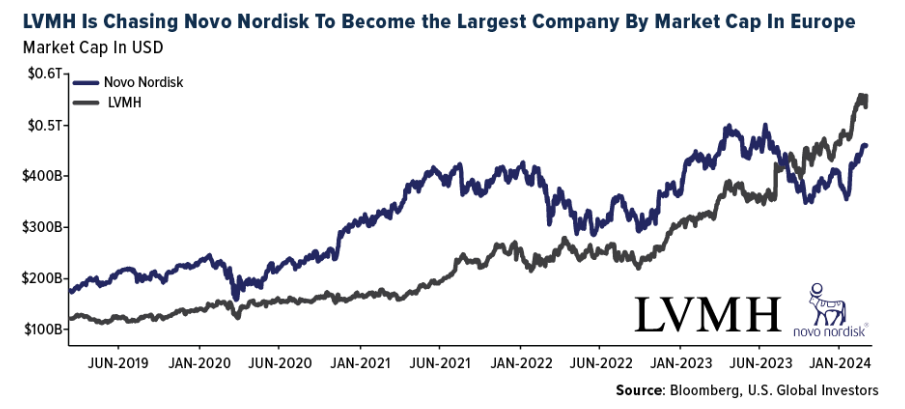

- Since January 17, the S&P Global Luxury Index has surged by 11.5%, surpassing the gains of both the S&P 1500 Index and European equities as measured by the STOXX Europe 600 Index. This uptrend can be attributed to a reporting season that exceeded expectations, driving up prices for certain luxury brands. Notably, Louis Vuitton is poised to potentially regain its status as the largest company in Europe by market capitalization.

- BYD, a Chinese local electric vehicle (EV) maker, is competing with Ferrari and Lamborghini, by introducing its new Yangwang U9 model. Initially, it will be offered locally with a price tag of $233,450. This is a high-performance electric supercar that can hit 100 kilometers per hour (62 miles per hour) in 2.36 seconds and reach a top speed of 309.19 kilometers per hour (192 mph).

- Next week, on March 5, China will begin its parliamentary annual meeting. The National People’s Congress (NPC) will set economic objectives for next year. Some analysts are expecting extra measures to be announced that will support the struggling country and lift equities trading in mainland China and on the Hong Kong Stock Exchange.

Threats

- Li Auto reported better-than-expected profitability and free cash flow for the fourth quarter, pointing to strong local demand for EV makers in China. Management guided to produce 100,000 cars in the first quarter of 2024, versus 53,000 units delivered in the same period last year. BYD already is a leader in EV sales, taking over Tesla’s market share, which generates about one-fifth of its sales in China.

- The University of Michigan Consumer Sentiment Index declined by 2.7% compared to the previous month, now standing at 76.9%. The index includes measurements of attitudes regarding personal finances, general business conditions, and market conditions or prices. The decrease in this index suggests a shift in consumer sentiment, potentially affecting consumers’ willingness to purchase discretionary goods.

- Although luxury markets have shown robust year-to-date performance, the JPMorgan research team remains skeptical about its sustainability. Earnings beats released this quarter have been modest, averaging only a 2% increase in fourth-quarter sales, primarily led by Moncler and Hermes. Anticipating minimal growth for the sector in the first half of the year, the JPMorgan team remains cautious.

Energy And Natural Resources

Strengths

- The best performing commodity for the week was China Lithium Carbonate 99.5%, rising 9.42%, on comments from Chile’s SQM (Sociedad Quimica y Minera de Chile SA) the world’s second largest lithium producer, who said the price of lithium will likely lift in the second half of the year, (prompting investors to take a more positive view on the outlook). SQM is so confident that buyers will return, they are continuing to increase output for stockpiles of lithium carbonate while buyers are running down their existing inventories.

- According to Bank of America, steel prices increased globally in the fourth quarter of 2023. The rally was remarkable in the U.S., where hot-rolled coil (HRC) prices rose by nearly 60% between September and December, topping $1,200 per ton. Indeed, while U.S. HRC prices have often outperformed those in Europe and China, that divergence has become increasingly visible in the past three years. The bank believes protectionist measures (i.e. trade restrictions) and public infrastructure spending have played a pivotal role.

- Oil rose this week, bolstered by pockets of strength in physical crude markets, writes Bloomberg, while traders weighed the potential for OPEC+ to extend its output cuts. West Texas Intermediate climbed to just shy of $79 a barrel in a low-volume session, trading near the highest level of 2024. In the physical market, U.S. refineries are benefiting from strong profit margins while foreign buyers are turning to American crude to avoid Red Sea shipping issues.

Weaknesses

- The worst performing commodity for the week was sugar, dropping 3.35%, on a 1.3-million-ton delivery for the March contract, the second largest for March, showed supplies may not be as tight as thought. Hedge funds also cut their bullish positioning to a six-week low, as reported by Bloomberg. According to Goldman, Qatar Energy’s announcement of further LNG export capacity expansion will likely extend the bearish cycle they expect in global LNG markets for most of the second half of this decade.

- An unusually warm winter and roaring U.S. output have pushed natural-gas prices to some of the lowest levels of the shale era. Adjusted for inflation, natural-gas futures recently hit their cheapest prices since trading began on the New York Mercantile Exchange in 1990. This is good news for American consumers, who can look forward to lower utility bills, as well as for businesses that use a lot of natural gas making basic materials like steel, concrete, cardboard, and fertilizer.

- According to CLSA, U.S. hot-rolled coil prices slipped further this week as tradable value from both Midwest and Southern mini-mill trended lower and as overall spot activity remained limited due to market uncertainty. Platts assessed the daily TSI U.S. hot-rolled coil index at $860 per ton on an ex-works basis, down $20 per ton from the previous assessment.

Opportunities

- Alcoa moved to cement its position as one of the world’s largest bauxite and alumina producers by making a $2.2 billion offer to buy Australia’s Alumina, its joint-venture partner in a global mining operation. Alcoa’s pursuit of Alumina represents a bet on commodities that have a role to play in the energy transition, with aluminum used in large quantities to manufacture electric vehicles and renewable-power infrastructure.

- Jubilee Metals Group is in talks to buy a mothballed Zambian copper-cobalt refinery from Eurasian Resources Group Sarl, according to the southern African country’s mining minister. Operations at the facility owned by ERG’s Chambishi Metals subsidiary were suspended in early 2020, after the Luxembourg- registered group said it could not supply enough feedstock to run the plant.

- Zambian President Hakainde Hichilema said a U.S.-backed project to connect Zambia’s copper mines to an Angolan port offers the nation a “once-in-a-lifetime” opportunity. The project will link mining operations that companies including Barrick Gold Corp. and First Quantum Minerals Ltd. own to the Atlantic Ocean port of Lobito by building new track in Zambia and connecting it to an existing railway in Angola. The U.S. is supporting the refurbishment of the Angolan line through a $250 million loan — subject to due diligence — that the International Development Finance Corp. announced last year.

Threats

- Copper fell along with most industrial metals, as rising inventories in China pointed to signs that a significant pick-up in demand following the Lunar New Year holiday is yet to materialize, writes Bloomberg. Weekly inventories for all base metals increased over the past week, with copper spiking in warehouses monitored by Shanghai Futures Exchange, after consumption slowed during the week-long holiday earlier this month.

- Many of the world’s biggest nickel mines are facing an increasingly bleak future as they wake up to an existential threat: a near limitless supply of low-cost metal from Indonesia, reports Bloomberg. With roughly half of all nickel operations unprofitable at recent prices, the bosses of the largest mining companies last week sounded a warning that there was little prospect of a recovery.

- Data confirms a slow start to the year in China, asthe operating rate of aluminium extruders (extrusions are used in construction) declined to 47.94% in January, reports the Shanghai Metals Market, also confirming that only a small number of companies received new orders. That weakness carried over into February, when most domestic aluminium extrusion factories have suspended production. This – and weak sentiment accompanying it – has been putting pressure on prices.

Bitcoin And Digital Assets

Strengths

- Of the cryptocurrencies tracked by CoinMarketCap, the best performer for the week was WIF, up 233.72%.

- A record $520 million stampeded into BlackRock’s spot Bitcoin ETF in a single day. The iShares Bitcoin Trust saw its biggest one-session haul on Tuesday, marking the largest daily inflow so far among the batch of new U.S. ETFs investing directly in the world’s biggest cryptocurrency, writes Bloomberg.

- Bitcoin jumped past $60,000 (briefly touching $63,000) for the first time in more than two years this week, amid surging optimism that demand for the token is widening beyond committed digital asset enthusiasts, writes Bloomberg.

Weaknesses

- Of the cryptocurrencies tracked by CoinMarketCap, the worst performer for the week was Bitget Token, down 5.42%.

- FTX’s Sam Bankman-Fried should serve no more than six and a half years in prison for orchestrating the fraud that brought down the cryptocurrency exchange, his lawyers told a federal judge who could issue a sentence of as long 20 years for the most serious charges in the case. His attorneys made their recommendation to U.S. District Judge Lewis Kaplan ahead of Bankman-Fried’s March 28 sentencing, writes Bloomberg.

- The U.S. government appears to have transferred about $922 million worth of Bitcoin from crypto wallets that held seized assets from a 2016 Bitfinex hack, writes Bloomberg.

Opportunities

- A group of former FTX and Alameda Research employees have raised $17 million to build out a crypto exchange called Backpack, joining the ranks of startups seeking to fill a gap left by the collapse of their former employer. The Dubai-based company, which also offers a crypto wallet and NFT collection called Mad labs, said it reached $120 million valuation, writes Bloomberg.

- Kraken, one of the oldest cryptocurrency exchanges, has started a new unit, Kraken Institutional, to better serve its largest customers. Designed to cater to users such as hedge funds and ETF issuers, the firms aim to become a one-stop shop with services like spot, trading, custody, lending, and staking, writes Bloomberg.

- Bitcoin climbed for a seventh consecutive day, with option traders increasing bets that the digital asset will soon surpass its late 2021 high. Bitcoin has surged more than 20% since last Friday, the biggest weekly increase in a year, writes Bloomberg.

Threats

- Coinbase Global experienced a spate of outages Wednesday just as Bitcoin continued its rally above $60,000. Coinbase reported that some users may see zero balances across their Coinbase accounts, writes Bloomberg.

- Michael Novogratz is cautioning investors that Bitcoin may see some corrections before rallying to a record and ending the year “much higher.” “I wouldn’t be surprised to see some correction and some consolidation,” Novogratz said during an interview, according to Bloomberg.

- Nigerian authorities have detained two executives of Binance just days after the central bank governor said that the nation is losing out on taxes from unregistered crypto exchanges. The two were intercepted by national security officers after arriving in the country on the grounds that Binance was illegally in Nigeria, writes Bloomberg.

Defense And Cybersecurity

Strengths

- General Dynamics received a contract modification worth up to $150.98 million for materials for Virginia Class submarines SSN 814-817. Completion of the project is expected by September 2035 and is funded by FY24 allocations, under the sole source authority of Federal Acquisition Regulation 6.302-1, by the Naval Sea Systems Command.

- Two years after Russia’s invasion of Ukraine, the global corporate sector, including major Western companies like Apple, Google, and Amazon, has played a crucial role in economically isolating Russia by exiting or reducing operations, while simultaneously aiding Ukraine’s resilience and recovery efforts amid the conflict. The international response, coupled with sanctions and the strategic withdrawal of over 1,000 companies from Russia, has significantly impacted Russia’s economy, underscoring the importance of corporate actions in addressing geopolitical challenges and supporting Ukraine’s fight against the invasion.

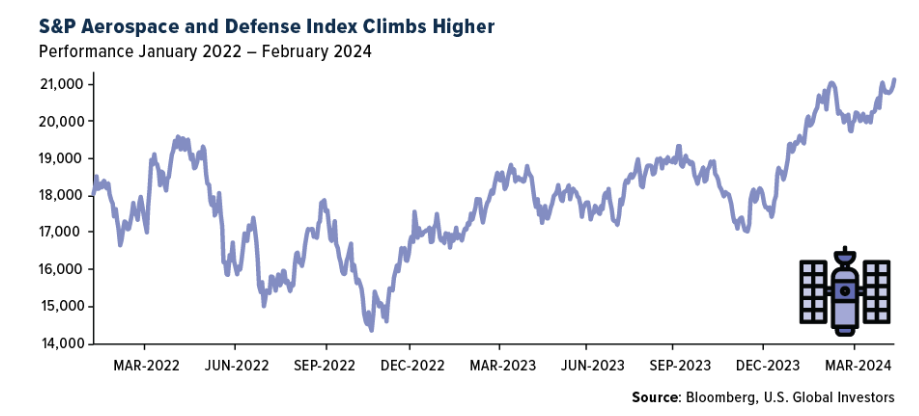

- Axon Enterprise Inc., a safety technology company, rose this week by 16.12%, becoming the best performing stock in the XAR ETF. This week the company’s price target was increased by 11 analysts, by an average of 18%.

Weaknesses

- Reports indicate that submarine cables in the Red Sea were damaged following threats from Yemeni Houthi rebels. This impacts internet access and highlights the region’s geopolitical tensions, along with the challenges of underwater infrastructure repair amidst ongoing conflicts.

- U.S. Border Patrol Chief Jason Owens reported that armed bandits attempted to rob migrants crossing illegally near the U.S. southern border, highlighting the dangers faced by migrants and border agents alike.

- Archer Aviation Inc., an aerospace company, was the worst performing stock this week, losing 5.41% in the past five days, after posting its latest fourth quarter report.

Opportunities

- Frank Calvelli, Space Force’s acquisition leader, advocates for the strategic use of fixed-price contracts for simpler projects but acknowledges the necessity of cost-plus contracts for complex endeavors like advanced satellites, balancing efficiency with the need for flexibility in face of industry concerns over financial risks. This approach aims to streamline procurement while accommodating the unique challenges of cutting-edge space technology developments.

- Shares of Palo Alto Networks surged after Congresswoman Nancy Pelosi disclosed buying up to $1 million in call options, despite the company’s lowered revenue guidance and subsequent downgrades by several Wall Street firms.

- In May, the U.S. Air Force will select Lockheed Martin or Boeing to develop its NGAD sixth-generation fighter, aiming to sustain air superiority with 1,000 drones and 200 stealth jets, despite each NGAD’s $300 million cost.

Threats

- U.S. and UK airstrikes against Houthi militants in Yemen have not deterred the group, which continues to attack commercial vessels in the Red Sea and Gulf of Aden, including a U.S.-owned oil tanker and a UK-owned cargo ship. Despite being designated a terrorist organization by the U.S., the Houthis are preparing for a prolonged conflict, fortifying mountain hideouts for missile launches and posing threats to maritime and internet infrastructure.

- Pro-Russian separatist officials in Transnistria have requested Moscow’s protection against Moldova’s increased pressure, as stated in a resolution from a special congress.

- After France stated that it does not exclude the possibility of sending its troops to Ukraine during an address to the Russian nation, Vladimir Putin warned NATO of a potential nuclear conflict if it intervenes in Ukraine. This emphasizes Russia’s capacity to strike back with nuclear weapons, amidst Putin’s military advancement in Ukraine and discussions in the U.S. and Europe about increasing support for Kyiv.

Gold Market

This week gold futures closed the week at $2,092.60, up $43.20 per ounce, or 2.11%. Gold stocks, as measured by the NYSE Arca Gold Miners Index, ended the week higher by 14.78%. The S&P/TSX Venture Index came in up 4.28%. The U.S. Trade-Weighted Dollar fell 0.03%.

Strengths

- The best performing precious metal for the week was gold, up 2.11%. The precious metal closed the week strongly on weaker-than-expected factor data on Friday combined with consumer confidence waning, which may prompt the Federal Reserve to act sooner rather than later. Bullion has largely held ground this year despite expectations being pushed back on how soon the Fed will start easing. Swaps markets suggest investors do not see much chance of a reduction in borrowing costs until June.

- According to BMO, Reunion Gold released a new resource and hosted a teach-in today. In general, the update was positive, with mineral inventory and grade both increasing. Indicated resources increased 72% compared to the June 2023 maiden resource. The company also released a maiden underground resource of 1,145K ounces.

- Endeavour Mining announced that wet commissioning is underway at its Sabodala-Massawa BIOX plant expansion with overall construction 91% complete and on budget, and that they are expecting first gold in early May 2024 (as planned). Sabodala-Massawa’s FY24 guidance forecasts production of 360,000-400,000 ounces at an all-in sustaining cost (AISC) between $750-$850 per ounce.

Weaknesses

- The worst performing precious metal for the week was palladium, down 3.78%. According to Bank of America, production widely disappointed with nine of 12 gold companies reporting guidance below Bloomberg consensus expectations. On unit costs, similarly, nine out of 12 companies reported guidance that was higher versus Bloomberg consensus expectations. Total capex was better, with only four out of 12 companies reporting higher capex than consensus. On conference calls, cost inflation remained very topical with most companies noting that they are still seeing cost inflationary pressures in certain areas (such as labor) while easing fuel costs have provided some offset.

- RBC says it expects a negative reaction from Argonaut Gold shares following 2024 guidance with higher costs and capital versus their estimates and consensus. At the Magino project in Ontario, greater dilution from selective mining of higher-grade material upfront has resulted in 5%-10% lower budgeted grades over the first few years. Throughput is guided to continue to ramp up through the first half of 2024 due to lower availability and higher costs driven by pressures related to labor and diesel.

- According to Sibanye Stillwater, platinum group metal (PGM) prices may be close to the bottom. BMO spoke to the continued challenges in the PGM environment but remained optimistic for the future, indicating that the PGM market could be nearing the end of the destocking cycle and outlook for interest rate cuts later in 2024 should help demand recovery. They are of the view that the supply response to the PGM price weakness, while possible, remains a less flexible option in the near term.

Opportunities

- Orla Mining announced it will acquire all the outstanding common shares of Contact Gold for $8.1 million, representing an implied enterprise value (EV)-to-ounces of resource of $18, compared to the average for developer companies at $89. Each holder of Contact shares will receive 0.0063 of an Orla share, for total consideration of $0.03 per share, with closing expected in the second quarter.

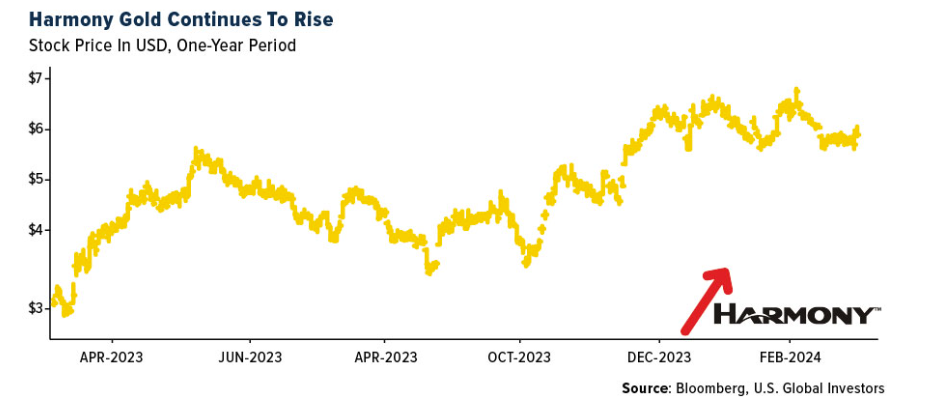

- Harmony Gold Mining said it will spend 7.9 billion rand ($410 million) to extend the life of the world’s deepest mine, bucking the trend in South Africa’s dwindling gold industry. The company acquired the Mponeng mine – east of Johannesburg – when AngloGold Ashanti sold its last remaining assets in South Africa four years ago. The project has become the star performer in Harmony’s portfolio, helping the miner triple its profit in the six months through December.

- BMO continues to be excited about the increased pace of new technology adoption among mining companies. As companies prepare for the next phases of growth, technology leaders are increasingly likely to adopt new productivity improvements such as electric vehicles, autonomous haulage, advanced process control, etc. These technologies will be available to “fast followers” as well as the first movers. Mines built to large-cap companies with financial and technical resources should have cost and efficiency advantages in the future.

Threats

- Mexico’s president, Andrés Manuel López Obrador, or AMLO, recently presented a series of potential constitutional changes to the Mexican Congress, including a measure that aims to ban open pit mining in the country. This is still very early stage and part of a broader reform package, which still must be approved by Congress by a 2/3rds majority in both houses.

- Northam Platinum reported that its earnings declined 91% year-over-year The PGM industry is currently navigating significantly depressed PGM prices and high inflation, together with a raft of global geopolitical uncertainties and locally, Eskom faces load curtailment events. We have not yet seen a change in fundamentals which are likely to move the market into more positive territory, and consequently, the short-term outlook remains challenging. Northam anticipates the depressed pricing environment will continue over the next 12 to 24 months, placing significant pressure on earnings and cash generation across the PGM mining sector as reported by Bloomberg.

- According to Scotia, for SSR Mining, public comments from the Turkish government indicate that test results to date have been negative with respect to potential environmental contamination. Containment and remediation efforts are ongoing as directed by the Turkish government, with an initial focus on removing heap leach material from the Sabırlı Valley and relocating it to a permanent storage location. SSR is in the process of evaluating the estimated remediation costs and anticipates recording a remediation liability during Q1/24.

U.S. Global Investors, Inc. is an investment adviser registered with the Securities and Exchange Commission (“SEC”). This does not mean that we are sponsored, recommended, or approved by the SEC, or that our abilities or qualifications in any respect have been passed upon by the SEC or any officer of the SEC.

This commentary should not be considered a solicitation or offering of any investment product. Certain materials in this commentary may contain dated information. The information provided was current at the time of publication. Some links above may be directed to third-party websites. U.S. Global Investors does not endorse all information supplied by these websites and is not responsible for their content. All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

Holdings may change daily. Holdings are reported as of the most recent quarter-end. The following securities mentioned in the article were held by one or more accounts managed by U.S. Global Investors as of (12/31/2023):

Japan Air Lines

Air Canada

FedEx Corp

Boeing

General Dynamics

Carnival

Royal Caribbean

Louis Vuitton

Moncler

Hermes

Reunion Gold

Argonaut Gold

Sibanye Stillwater

Contact Gold

Harmony Gold Mining

Anglogold Ashanti

SSR Mining

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry. The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies. The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks. The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months. The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange. The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver. The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar. The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks. The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The S&P/TSX Venture Composite Index is a broad market indicator for the Canadian venture capital market. The index is market capitalization weighted and, at its inception, included 531 companies. A quarterly revision process is used to remove companies that comprise less than 0.05% of the weight of the index, and add companies whose weight, when included, will be greater than 0.05% of the index.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500. The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500. The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period. The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500. The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500. The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500. The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500. The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500. The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500. The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns. The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment. Gross domestic product (GDP) is the monetary value of all the finished goods and services produced within a country’s borders in a specific time period, though GDP is usually calculated on an annual basis. It includes all private and public consumption, government outlays, investments and exports less imports that occur within a defined territory.

The S&P Global Luxury Index is comprised of 80 of the largest publicly traded companies engaged in the production or distribution of luxury goods or the provision of luxury services that meet specific investibility requirements.

The STOXX Europe 600 Index is a stock market index that represents a broad array of European companies. It is part of the STOXX Global Index family, which includes various regional and global indices. The STOXX Europe 600 Index includes large, mid, and small-cap companies across 17 European countries, covering approximately 90% of the region’s market capitalization.

The Michigan Consumer Sentiment Index (MCSI) is a monthly survey of consumer confidence levels in the United States conducted by the University of Michigan. The survey is based on telephone interviews that gather information on consumer expectations for the economy.

The Gold Fear and Greed Index is based on a variety of data points, including physical gold premiums data, gold spot price volatility, social media sentiment around gold, proprietary retail activity for gold, and Google Trends data on Gold search terms. The Crypto Fear and Greed Index is based on volatility, social media sentiments, surveys, market momentum and more.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our full schedule of upcoming CE-approved virtual events.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits