This PIMCO Perspectives assesses how the term premium’s 40-year downturn could start to reverse.

Common sense holds that investors should get paid more for taking more risk. This tends to be true in the bond market: The further you extend the maturity of bonds you hold, the more uncertainty you are underwriting and the more you should get compensated. Think about it simply. If you own a two-year bond, your principal will be returned after two years (absent default) and you can decide how to reinvest. The problem with a 30-year bond is that after two years, you still have to wait another 28.

Currently, the U.S. bond market doesn’t follow this logic. The yield curve is inverted, with cash yielding more than longer-dated bonds. The odds are that this trend will not continue.

The most common way an inversion corrects is when the Federal Reserve cuts its short-term policy rate, which both markets and Fed officials expect to happen this year. However, there is the possibility of a much bigger shift ahead: that the curve will also correct as the term premium comes back.

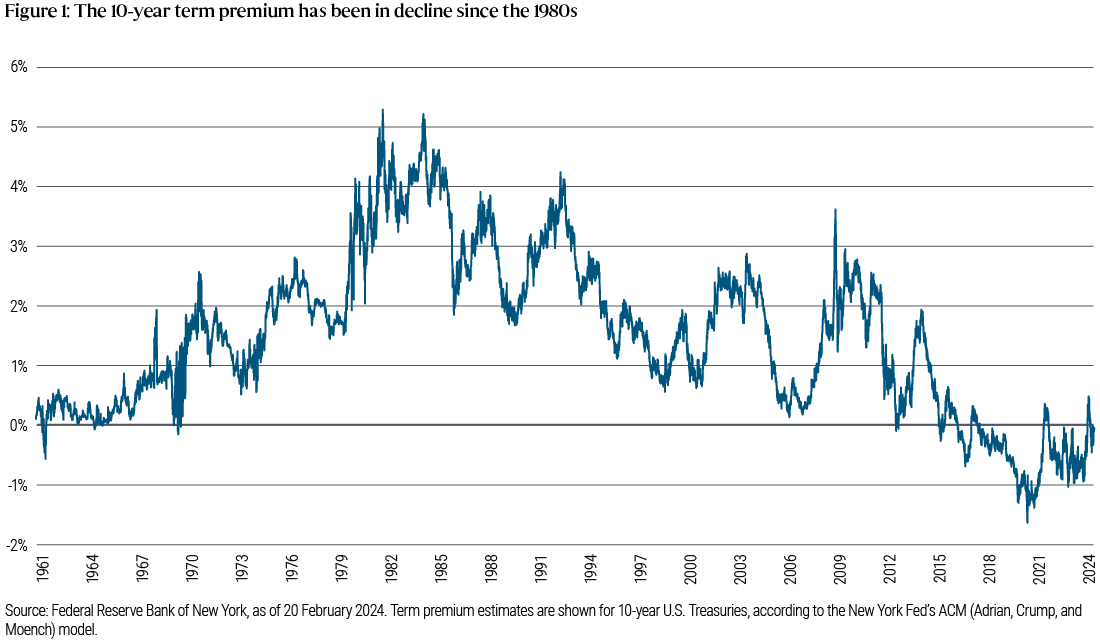

Since the financial crisis, the term premium – a gauge of how much more it pays to hold longer-dated debt instead of repeatedly reinvesting in short maturities – has averaged only about 50 basis points (bps), even turning negative at times (see Figure 1). But what if we are heading back to the future, to a market resembling prior decades when higher term premiums prevailed?

The term premium has gradually declined since rising well above 400 basis points (bps) in the 1980s – when strategist Ed Yardeni coined the term “bond vigilantes” for investors who discipline government spending by demanding higher yields, and when the movie that inspired this column’s title was released.

We are at a moment when the term premium could start to reverse the 40-year downtrend. January’s hotter-than-expected consumer price index (CPI) reading, along with the Congressional Budget Office’s latest estimates in February of the rising trajectory of U.S. debt (and the presumable increase in Treasury issuance needed to fund that debt), are recent signs of forces that could help rebuild the term premium.

If the term premium returned even to levels common in the late 1990s to early 2000s – around 200 bps – that would likely become the defining feature of financial markets during this era. It would not only affect bond prices but also prices of equities, real estate, and any other asset that is valued based on discounted future cash flows.

Spent stimulus

How far back to the future could we go? Consider that the U.S. hasn’t run a balanced budget in more than two decades. This hasn’t mattered because interest expenses held steady despite soaring debt. Thank falling interest rates (and term premium) for that – partly a function of the extended post-financial crisis period that PIMCO in 2009 dubbed “The New Normal.”

Then COVID-19 changed everything. Massive pandemic-era fiscal spending helped U.S. households build excess savings, but it contributed to the spike in inflation that shocked the U.S. economy away from the zero lower bound of interest rates.

U.S. consumers have since shown greater resilience than those in other developed market (DM) countries, but that durability is fading everywhere. U.S. and euro area households are back to pre-pandemic levels of real wealth, and the U.K. is well below those levels, while inflation has cooled but remains sticky.

Borrowing costs are now higher, as are ongoing deficits. Therefore we know with near-certainty that interest expenses will keep rising.

Privilege and discipline

Markets call this type of profligacy “fiscal dominance” – and the conventional reaction for governments is to stop spending! Recall the U.K.’s fiscal issues in September 2022 – when the British pound lost almost 15% of its value following unfunded government spending proposals – and countless emerging market (EM) examples to boot.

The important point is that markets are a disciplining mechanism for governments, keeping them from straying too far down this spending path. Well, that is the case for nearly every DM and EM country – but it does not necessarily apply to the U.S. as the custodian of the world’s reserve currency.

Indeed, the U.S. is leaning very hard on this exorbitant privilege. But privilege can tip into profligacy, slowly at first and then all of a sudden.

In the U.S., the last instance of this was in the 1980s, when the market – led by those bond vigilantes – demanded higher borrowing costs in what became a vicious spiral. It took a disciplined, coordinated approach by policymakers to short-circuit this spiral, first with tight monetary policy in the 1980s, followed by tighter fiscal policy throughout the 1990s.

And here is the crux of our concern: There is not the political will to do today what was ultimately required then. Sadly, more deficits are in the cards.

Investment implications

To be clear, we do not think we are traveling straight back to the 1980s – even if “Back to the Future” has recently reappeared as a Broadway musical. The Fed remains independent and will seek to keep a lid on inflation. But even a return to term premium levels of later decades would have material asset price implications.

In the third quarter of 2023, the term premium climbed as bond yields rose globally amid concerns about debts, deficits, higher-for-longer rates, and Fitch’s downgrade of the U.S. credit rating. Shortly thereafter, we noted our overweight view toward duration – a gauge of interest rate risk – saying yields looked high relative to our near-term expectations. In the ensuing months, yields fell.

We could get a second bite at the apple. As we said in our January Cyclical Outlook, “Navigating the Descent,” fiscal concerns will likely persist and could produce further episodes of long-end yields rising. We cited a curve-steepening bias in our portfolios, with overweight positions in the 5- to 10-year area globally and underweights in the 30-year area.

There is a very real possibility that the curve could kink following the first Fed rate cut, with shorter-term yields declining, intermediate rates not moving much, and longer-term yields rising as the term premium stages a comeback. In the meantime, investors do not have to take excessive duration risk to capture the lion’s share of income and potential return.

DISCLOSURES

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the manager] and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.: ©2024, PIMCO]

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© PIMCO

More Large Cap Growth Topics >