Q4 earnings revealed a tale of two markets in the U.S., with tech and internet players hitting home runs as other sectors and industries played small ball in comparison. Yet Fundamental Equities investor Carrie King sees the market broadening in the quarters ahead, opening up a wider playing field for stock pickers.

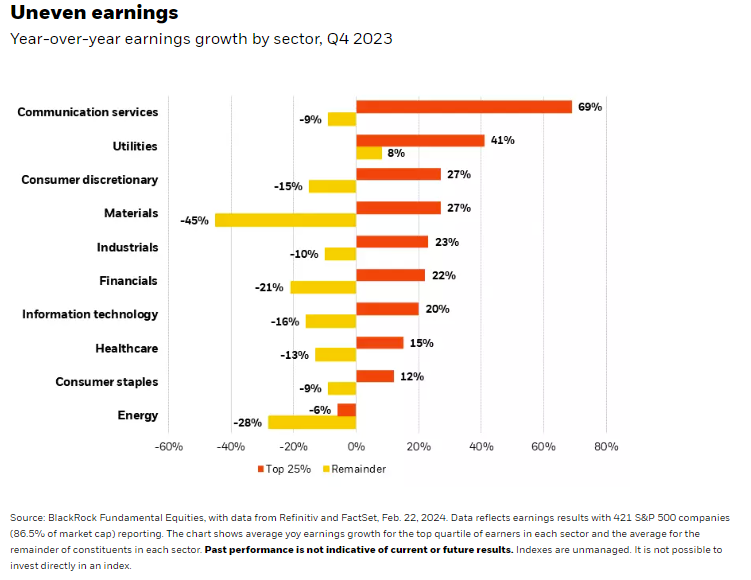

Dispersion on display

S&P 500 earnings were positive for a second consecutive quarter, with the lion’s share of Q4 growth powered by the tech and internet stocks that led markets higher in 2023. Earnings growth of 4.4% at the index level masks dispersion in year-over-year (yoy) results not only between sectors, but within them.

Consumer discretionary (+52%) and communication services (+43%), together holding four of the “Magnificent 7” mega-cap stocks, were Q4 standouts. Energy (-25%) and materials (-20%) were the main laggards as commodities prices fell with moderating inflation.

Healthcare, one of our favored sectors, saw negative earnings as well, yet this was driven by only four names in a category that includes more than 50. This illustrates the differentiation we’re seeing within sectors (see chart below) as well as the importance of stock selection to parse potential winners and losers and maximize a portfolio’s return prospects. While earnings dispersion is not new or unexpected, we believe it can be more informative in an environment where company fundamentals may be poised to drive more price action after an extended period in which macro concerns dominated markets.

Broadening beyond tech-plus

Earnings expectations for the so-called tech-plus stocks that have been driving market returns since last year were exceptionally high ― and yet they surpassed even that lofty bar. Healthy revenue growth plus a cost base that was “right sized” in 2023 contributed to the strong results. Year-over-year comps also were not hard to beat after a dismal 2022.

We still like tech stocks and expect momentum from generative AI to continue powering earnings growth. Yet the biggest numbers are probably in, with comps getting tougher and earnings likely to decelerate from Q4’s very robust levels.

Meanwhile, we see reason to believe that earnings growth for the remainder of the S&P 500 could pick up. The technology sector broadly has been experiencing a different business cycle than the rest of the market. Bloated investing and hiring during the COVID-induced digitization of everything in 2020 and 2021 was followed by a reining in and normalization in 2022 and 2023.

Other sectors were having the opposite experience, suffering during COVID and still re-adjusting upward today. Healthcare procedures and travel plans that were delayed during the pandemic are back on and consumers are still playing catch-up on missed experiences. Q4 results for hotels, restaurants and leisure showed 88% yoy earnings growth and profit margins that are just now returning to pre-COVID levels. One major hotel chain noted their expectation for slower but still growing leisure revenues into 2024. We’re watching the consumer closely, given pockets of stress that we noted last quarter, and are acutely attuned to the impact that higher interest rates are having on wallets and purchasing decisions.

The example in EVs

Q4 earnings offered one notable example of where consumers are growing more guarded ― in the market for electric vehicles (EVs). The EV leader in the Mag 7 was the only name in the group to post negative yoy earnings growth in the quarter. Another major U.S. EV manufacturer noted in its earnings call “the impact of historically high interest rates” on demand while also announcing job cuts.

To be sure, the effect of higher rates on total purchase price is not the only factor in the EV slowdown. The market is experiencing growing pains as early adopters are at saturation and manufacturers look to penetrate the next layer of potential buyers. Technical issues around battery range and infrastructure for charging are also being addressed and some traditional car makers are refocusing efforts on hybrid vehicles over fully battery-powered models.

Yet the pullback in demand among EVs and other big-ticket items speaks to a more discerning consumer who is beginning to feel the bite of higher rates and prioritize purchases. A major home improvement chain, for example, noted that the consumer is still “healthy” and “engaged” ― but in smaller projects at this juncture.

As fundamental stock pickers, we are looking to identify those companies best positioned to weather a potential consumption slowdown as buyers grow more discriminating in their spending.

Bottom line

We expect a slowdown in the blockbuster tech-plus earnings alongside a pick-up in the rate of earnings growth in those areas of the market where COVID hangover effects are still being worked off. Dispersion in earnings is evident between and within sectors as companies adjust to a new era of higher rates and volatility. This, we believe, creates a fertile hunting ground for active stock pickers to source greater alpha opportunities in an environment where we believe beta, or market return, could underwhelm expectations.

Earnings figures cited herein are from BlackRock Fundamental Equities, with data from Refinitiv and FactSet. Figures are as of Feb. 22, 2024, with 421 companies (86.5% of S&P 500 market cap) reporting. Yoy figures compare currently reported data to full-quarter data one year prior and are subject to change.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of March 2024 and may change as subsequent conditions vary. The information and opinions contained in this post are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by BlackRock, its officers, employees or agents. This post may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this post is at the sole discretion of the reader. Past performance is no guarantee of future results.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

Prepared by BlackRock Investments, LLC, member FINRA.

© 2024 BlackRock, Inc. or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc., or its affiliates. All other marks are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© BlackRock

More Active Management Topics >