February update

- Municipals posted positive performance and outperformed comparable Treasuries in February.

- We expect supply-and-demand dynamics to turn less supportive in the coming months.

- After patience to start the year, we would view any material backup as an opportunity to buy.

Market overview

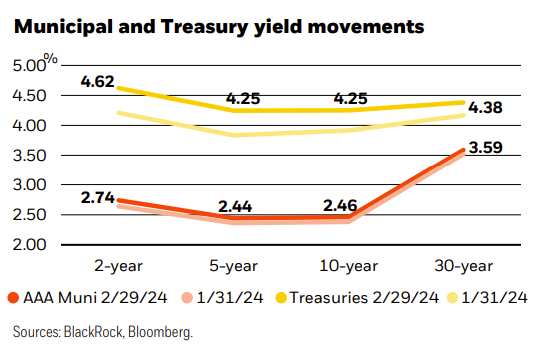

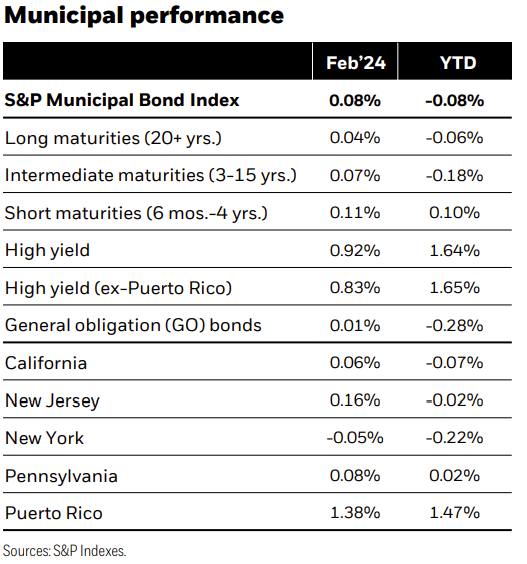

Municipal bonds posted modestly positive performance in February as the macro-backdrop remained the focus. Interest rates rose considerably amid firm economic growth, a surprising uptick in inflation, and a message of continued patience from the Federal Reserve. Favorable supply-anddemand dynamics prompted strong municipal outperformance versus comparable Treasuries. The S&P Municipal Bond Index returned 0.08%, bringing the year-todate total return to -0.08%, with coupon return slightly outpacing negative price return. The 20-year part of the yield curve and lower-rated credits performed best.

Issuance was $31 billion in February, 2% above the five year average, bringing the year-to-date total to $62 billion. Supply was outpaced by reinvestment income from maturities, calls, and coupons by over $5 billion. As a result, deals were well absorbed, oversubscribed 5.3 times on average. At the same time, demand remained firm. Mutual fund flows waned slightly from the levels experienced in January but stayed consistently positive, led by the high yield sector.

Seasonals turn less supportive in the coming months as the market transitions to net positive supply in the spring. March has historically been one of the worst-performing months of the year, typically pressured by a month-overmonth swell in issuance. This year, supply could be further exacerbated if issuers are successful in their efforts to trigger the extraordinary redemption provision to refinance Build America Bonds in the tax-exempt market. However, given our patient approach earlier in the year, we would welcome a market correction and view any material backup as an opportunity to put cash to work at more attractive absolute and relative valuations.

Strategy insights

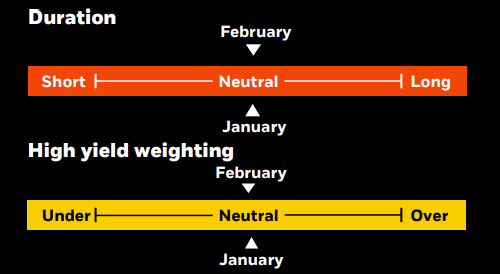

We favor a neutral duration posture overall. We continue to advocate a barbell yield curve strategy, pairing front-end exposure with an increased allocation to the 15 - 20-year part of the curve. We prefer single-A rated credits but think high yield offers an attractive risk-reward opportunity, given favorable structures and the ability to generate alpha through security selection.

Overweight

- States that primarily rely on consumption taxes

- Essential-service revenue bonds

- Flagship universities

- Select issuers in the high yield space

Underweight

- States overreliant on personal income taxes, especially California Speculative projects with weak sponsorship, unproven technology, or unsound feasibility studies

- Senior living and long-term care facilities

- Lower-rated private universities

- Stand-alone and rural health providers

Reserves cushion rising budgets

Illinois: Governor Pritzker proposed a $52.7 billion fiscal year (FY) 2025 general fund budget that closes an initial $721 million gap with roughly $800 million in additional revenue, particularly by raising the sports-betting tax to 35% from 15% and capping corporate tax deductions. Spending is projected to rise by a modest 1.4% from the current FY 2024 level, with education increasing 3.7% to $13.4 billion, or about 25% of expenditures. Pension contributions total $10.1 billion, or almost 20% of spending. While the current statutory mandate calls for a 90% funding level by 2045, the governor has proposed a plan to lift the funding level to 100% by 2048. The FY 2025 executive budget is expected to add $170 million to the rainy-day fund, bringing the total to $2.3 billion, an historical high, but still a modest 4.4% of total expenditures.

New Jersey: Governor Murphy proposed a $55.9 billion FY 2025 spending plan that approximates current FY 2024 adjusted appropriations. Perhaps the most controversial revenue-raising proposal is the reinstatement of a 2.5% corporate surcharge (11.5% total corporate tax rate) on companies with net annual incomes over $10 million. This “corporate transit fee” is expected to raise $1 billion in FY 2025 for NJ Transit and could be a continuing dedicated revenue stream for the agency. The FY 2025 executive budget forecasts a 3.6% increase in total revenue but will use reserve drawdowns for the second consecutive year. K12 education remains a key driver of increased outlays, with direct aid rising to $11.7 billion, +8% from the prior FY and 21% of FY 2025 spending. The budget also includes a $7.1 billion pension contribution, the fourth consecutive year of a full actuarially determined contribution. While reserves are forecast to decline by roughly $2 billion at FYE 2025, the $6.1 billion ending surplus balance, at 11% of total appropriations, significantly exceeds pre-COVID-19 levels.

Investment involves risk. The two main risks related to fixed income investing are interest rate risk and credit risk. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from tax-exempt bonds may be taxable. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. Past performance is no guarantee of future results.

This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of March 7, 2024, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. There is no guarantee that any forecasts made will come to pass. Any investments named within this material may not necessarily be held in any accounts managed by BlackRock. Reliance upon information in this material is at the sole discretion of the reader.

©2024 BlackRock, Inc or its affiliates. All Rights Reserved. BlackRock is a trademark of BlackRock, Inc or its affiliates. All other trademarks are those of their respective owners.

Prepared by BlackRock Investments, LLC, member FINRA.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© BlackRock

Read more commentaries by BlackRock