At Mutual Series, we do not believe the packed and contentious 2024 global election season will upend the major long-term trends around supply-chain links, energy security and defense—all of which can further support certain value stocks.

Much of the world votes in 2024, and the potential for heightened geopolitical uncertainty and greater equity market volatility abounds. With citizens in more than 50 countries going to the polls, representing nearly half of the world’s gross domestic product, a change in some countries’ domestic policies could inevitably follow. Regardless of the outcomes, we believe that countries’ long-term focus on supply chain resilience, energy security and defense spending should continue—a potential boon to various companies in the value universe.

Reforging supply chains

From the slate of elections to the grinding Russia-Ukraine war and flashpoints across the Middle East, the world is on greater edge in 2024 than it has been in some time. As a result, company supply chains have come under increasing pressure. Most recently, Houthi attacks on shipping through the Red Sea has led some to abandon the shorter routes through the Suez Canal to take the much longer route around Africa. This rerouting increases the time it takes goods to reach their destination and can raise shipping costs.

Potential inflation aside, what the Red Sea tensions—and geopolitical uncertainties—demonstrate is the ongoing need for companies—and countries—to reforge their global supply chains. Efforts that began during the pandemic to bring manufacturing closer to home and fortify supply chains should continue apace, in our view. Companies are weighing the risks of maintaining manufacturing facilities in far-off countries against the cost of reshoring. As such, supply chains that stretch around the world are starting to be unlinked in favor of ones that are closer to home or that run through friendly countries.

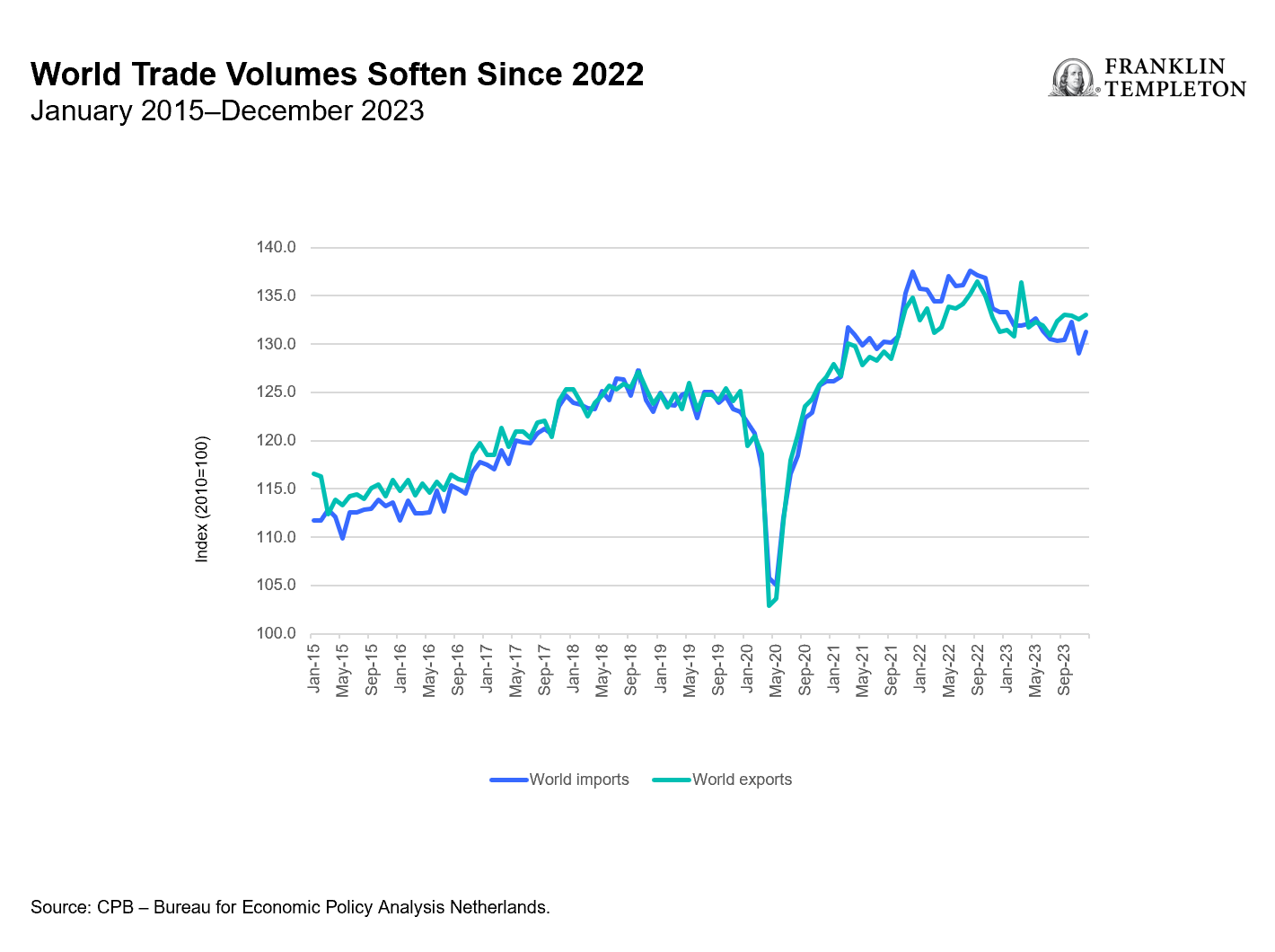

Global trade growth is softening as a result. According to the International Monetary Fund’s January World Economic Outlook, world trade should grow at 3.3% and 3.6% in 2024 and 2025, respectively, below the historical average of 4.9% growth. Weaker trade underscores the softer global growth, greater trade distortions and the unwinding of global economic integration, partly due to a tenser geopolitical environment.1 Overall, we have seen global trade soften since peaking in August 2022 (see Exhibit 1). As supply chains move, we see a greater need for the materials to build new plants, for the tools to automate them, and for new shipping routes—all areas where value companies are heavily involved.

Exhibit 1

Renewables for independence

As supply chains break, the global links between energy suppliers and energy importers are also shifting. Since the Russia-Ukraine war began in 2022, Europe, for one, is much more cognizant of the risks of depending so heavily on one country for its energy needs. While Europe had been moving toward greater renewable power generation before the 2022 war, it has more investment earmarked to reach its green energy goals. Upcoming parliamentary elections in the European Union (EU) are unlikely to change this trajectory, in our view.

Following the start of the war, the EU announced REPowerEU to wean itself from a heavy dependence on Russia for energy supplies. The program seeks to diversify energy supplies, increase gas storage, focus on energy savings and invest more in renewables. The EU is looking to raise its binding 2030 target for renewable energy to 42.5%, nearly double what renewables make up in energy production currently.2

Meanwhile, we are seeing a similar focus on cleaner energy elsewhere in the world. Recent US legislation, backed by both Democrats and Republicans, has allocated more funds toward climate change mitigation and energy security that could create additional investment opportunities. Countries are building more liquified natural gas terminals, wind farms, carbon capture facilities and pipelines. Energy giant Shell estimates that liquified natural gas demand should climb 50% by 2040 as the world transitions to cleaner fuels, resulting in increased spending on the shipping and regasification infrastructure to support its transportation and use.3

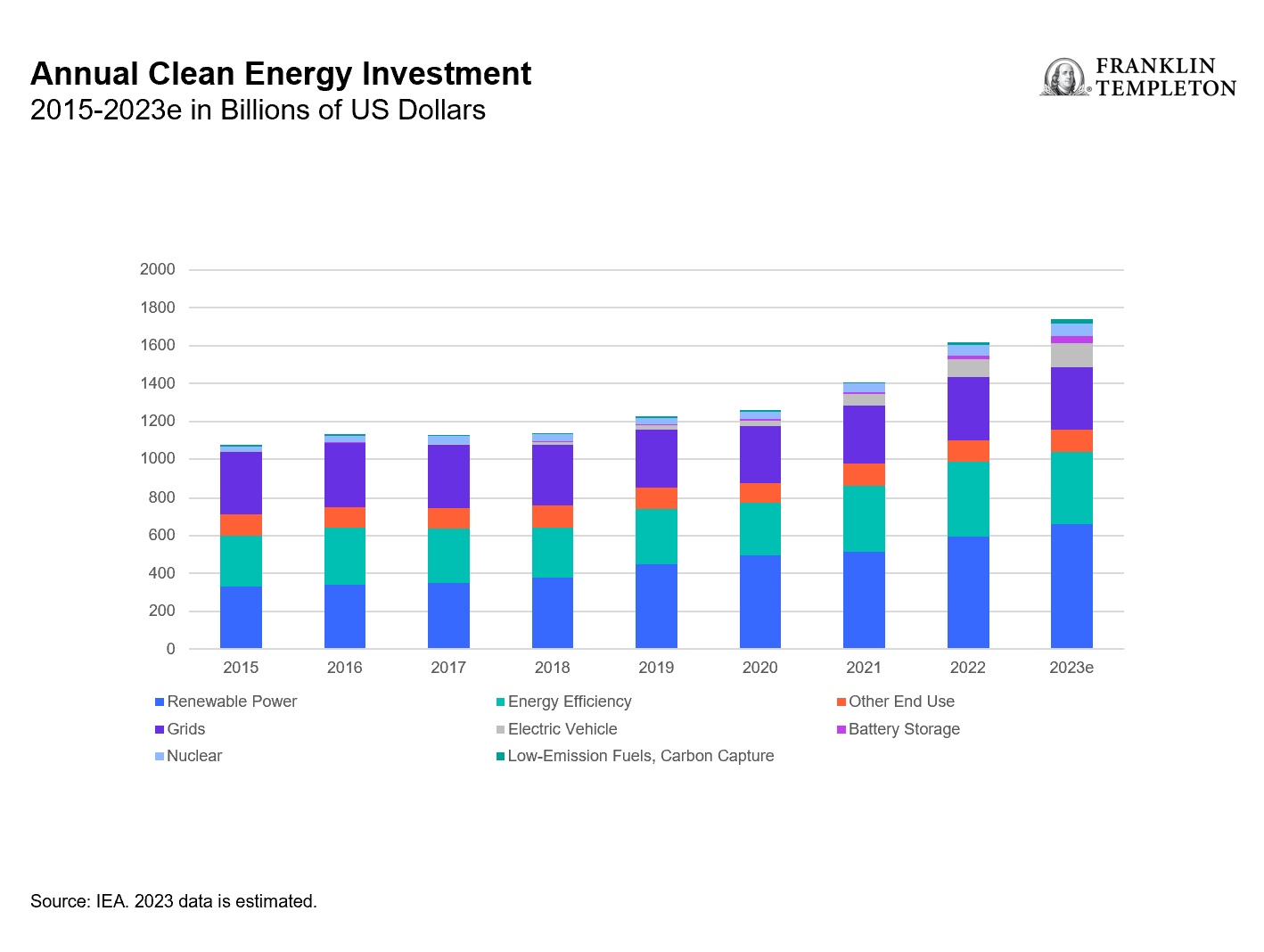

Since the start of the COVID-19 pandemic, governments have been spending on a host of “green” initiatives, including low-carbon electricity, mass transit and energy efficient buildings. They have plowed nearly US$900 billion into those three areas alone in recent years, according to data from the International Energy Agency (IEA). And clean energy investments continue to rise across a range of areas (see Exhibit 2).

Exhibit 2

In our analysis, other infrastructure spending is also geared toward sectors that trade at “value” multiples across the energy, industrials and materials sectors. US government spending on building new semiconductor and electric vehicle battery plants should lead to greater spending on the metals, cement and industrial equipment used to build them. With the US$39 billion in the CHIPS and Science Act earmarked for manufacturing incentives over the coming years and many plants being built in so-called Red States, we believe the spending program will be hard to reverse should a new US administration or change in control of Congress come to pass in November.

Moreover, the United States is not alone in spurring domestic semiconductor manufacturing activity. China, Europe, Japan and South Korea all have earmarked significant funds to support their own domestic chip manufacturing—a further boon to global infrastructure spending.

A stronger defense

In addition to shoring up supply chains and energy security, the tetchier geopolitical environment is also prompting countries to ramp up their defense spending. While the United States spends the most on its military at over US$810 billion in 2023, the EU and Japan are also boosting spending to deal with rising tensions. We would expect this trend to continue regardless of the outcome of the slate of elections this year. Western countries need to replenish depleted stockpiles while continuing to invest in next generation weapons systems, in our view.

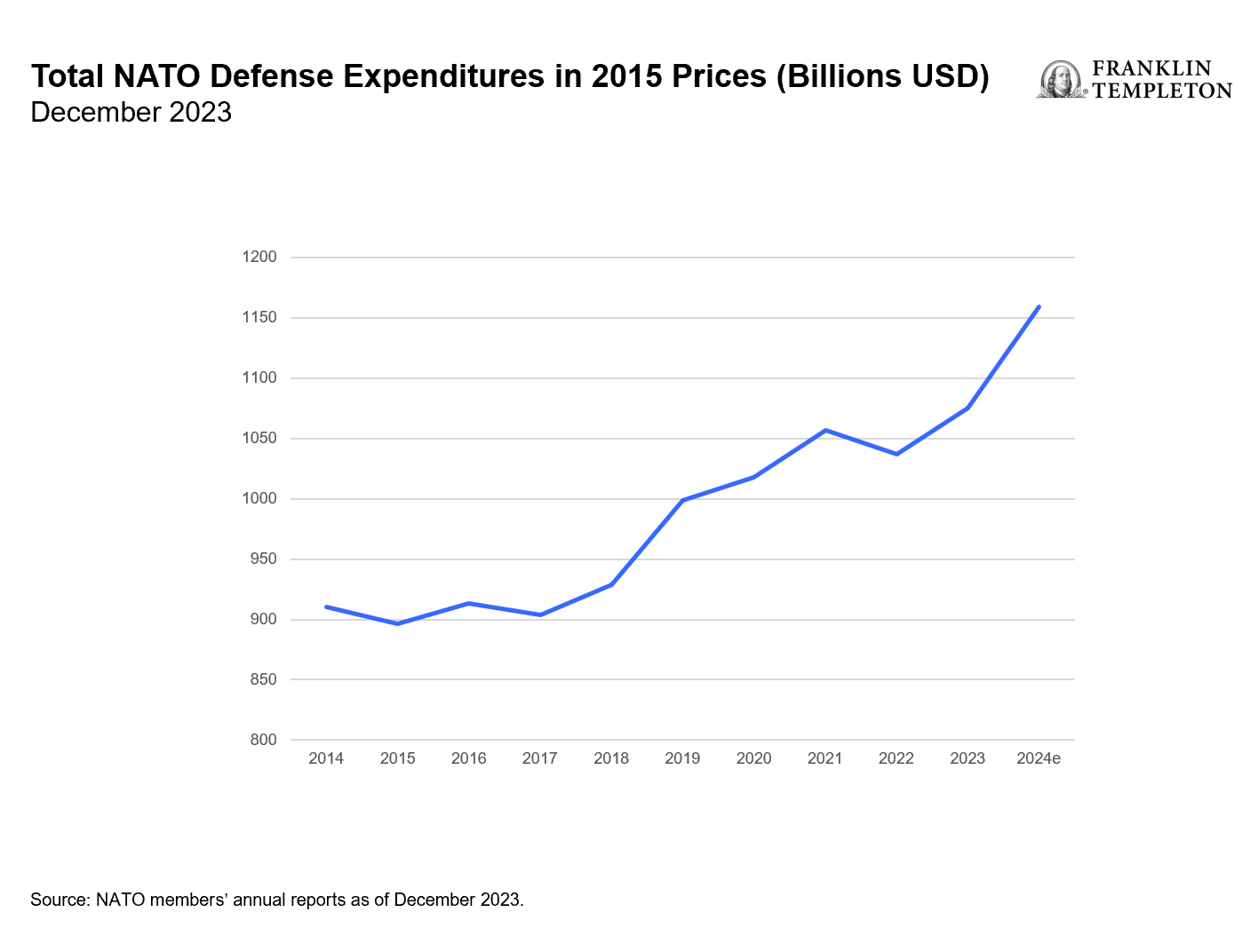

In February 2024, North Atlantic Treaty Organization (NATO) Secretary-General Jens Stoltenberg said that European NATO allies would spend about US$380 billion on defense this year (see Exhibit 3).4 Many European countries are spending more money on defense than they have historically, with a focus on dealing with the greater security needs since the Russia-Ukraine war. Additionally, Germany created a €100 billion fund in 2022 to spend on strengthening its defense capabilities, with most of the fund having already been spent on large-scale equipment.

Exhibit 3

Japan is also building its defense capabilities, as it eyes increasing tensions with China, North Korea and Russia. Its draft budget for fiscal 2024, which starts in April, is up sharply from the year earlier budget. In all, greater geopolitical uncertainty is forcing countries to spend more on munitions, aircraft, equipment and security systems.

Whichever parties win their respective national elections in 2024, we believe value stocks can win investors’ votes.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

International investments are subject to special risks, including currency fluctuations and social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Value securities may not increase in price as anticipated or may decline further in value. The investment style may become out of favor, which may have a negative impact on performance.

Active management does not ensure gains or protect against market declines.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

1. Source: “World Economic Outlook Update.” International Monetary Fund. January 2024.

2. Source: “Energy Transition in the EU.” European Union. November 2023.

3. Source: “Shell LNG Outlook 2024.” Shell.com. February 2024.

4. Source: “NATO chief says Europe meeting spending targets after Trump criticism.” Reuters. February 15, 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Franklin Templeton Investments

Read more commentaries by Franklin Templeton Investments