In this article, Russ Koesterich discusses the reason that bonds are not providing the same diversification benefit to equities as in prior decades.

Key takeaways

- Lower macro stability has resulted in a different stock/bond dynamic. With the economy improving and recession fears all but gone, investors are more concerned about ‘sticky’ inflation and the Fed.

- In this environment, the dollar is likely to respond positively if fewer rate cuts translate into a stock market correction, serving as a hedge to equities.

Stocks are rallying, bonds are (mostly) stable and fears of a recession are rapidly receding. In most respects we’re a long way from the dark days of 2022. That said, one thing has not changed: bonds are still a less reliable hedge then in years past.

After surging in January and mid-February, long-term yields have slipped in recent weeks. However, while the bond market has been calmer, there are still lingering questions regarding inflation, more specifically how quickly it will revert to the Federal Reserve’s (Fed) long-term target of 2%. Both the level and volatility of inflation are important for how stocks and bonds co-move. Until inflation is both lower and more stable, we may remain in an environment in which bonds are a less consistent hedge of equity risk.

I last discussed the role of bonds as a hedge in the summer of ‘23. At the time, I suggested that despite inflation improving and financial conditions easing, we were still a long way from the pre-pandemic norms. While there has been further progress on the inflation front, as the Fed has been at pains to highlight, returning the U.S. economy to low and stable inflation is still a work in progress.

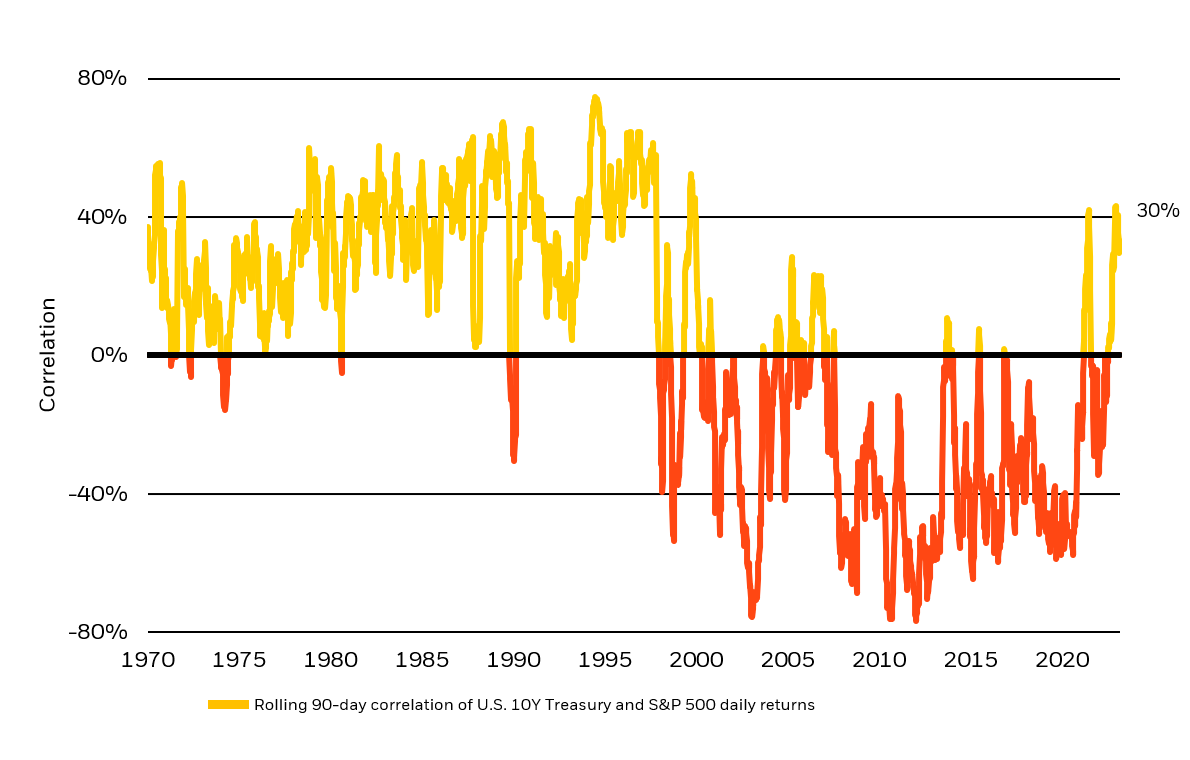

Less macro stability has led to a different stock/bond dynamic. Prior to 2021, stock bond correlations (i.e. extent to which prices change together) were stable and negative for nearly 20 years. That began to change in 2021 and we have still not gone back to the norms of previous decades. Correlations across most time frames remain positive and significantly higher than they were pre-pandemic (see Chart 1).

While numerous factors influence asset correlations, for stocks and bonds, an important metric to watch is the volatility of inflation. Stock/bond correlations tend to be negative when the volatility, i.e., standard deviation of inflation is low and stable. And while inflation volatility, along with headline inflation, is slowly falling it remains elevated compared to the pre-pandemic average.

Portfolio Implications

Until we see a further stabilization in inflation, where to look for equity hedges? As has been the case since 2022, the dollar still appears the best bet. Dollar/stock correlations remain significantly negative, suggesting a large dollar position may provide a decent hedge when equities are falling.

Why should this still be the case? With the economy improving and recession fears all but gone, investors are more concerned about ‘sticky’ inflation and the Fed. In this environment, the dollar is likely to respond positively if fewer rate cuts translate into a stock market correction. For this reason, at least until the inflation risk completely fades, staying overweight the dollar may be the better hedge. Investors can accomplish this through a variety of mechanisms, including international ETF’s which hedge currency exposure and, ironically, remaining overweight U.S. stocks.

Russ Koesterich, CFA, JD

Managing Director and portfolio manager

Russ Koesterich, CFA, JD, Managing Director and portfolio manager, is a member of the Global Allocation team as well as the lead portfolio manager on the GA Selects model portfolio strategies.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© BlackRock

Read more commentaries by BlackRock