Blackout Of Buybacks Threatens Bullish Run

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWith the last half of March upon us, the blackout of stock buybacks threatens to reduce one of the liquidity sources supporting the bullish run this year. If you don’t understand the importance of corporate share buybacks and the blackout periods, here is a snippet of a 2023 article I previously wrote.

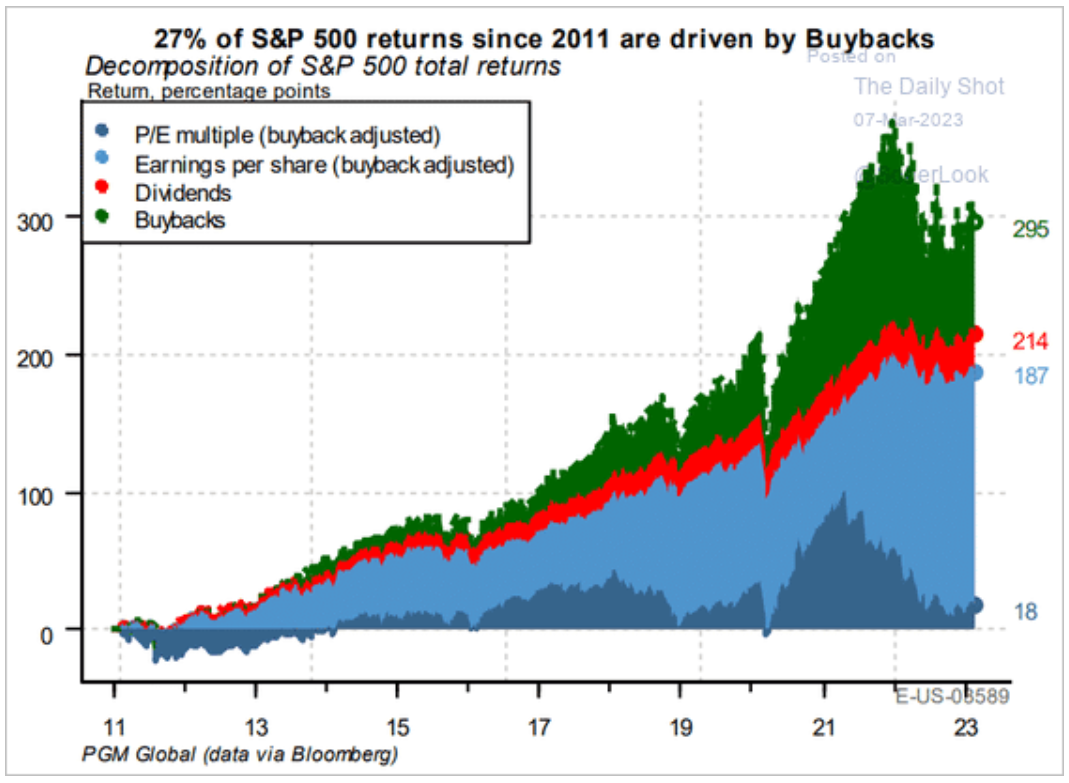

“The chart below via Pavilion Global Markets shows the impact stock buybacks have had on the market over the last decade. The decomposition of returns for the S&P 500 breaks down as follows:“

- 6.1% from multiple expansions (21% at Peak),

- 57.3% from earnings (31.4% at Peak),

- 9.1% from dividends (7.1% at Peak), and

- 27% from share buybacks (40.5% at Peak)

Yes, buybacks are that important.

As John Authers pointed out:

“For much of the last decade, companies buying their own shares have accounted for all net purchases. The total amount of stock bought back by companies since the 2008 crisis even exceeds the Federal Reserve’s spending on buying bonds over the same period as part of quantitative easing. Both pushed up asset prices.”

In other words, between the Federal Reserve injecting massive liquidity into the financial markets and corporations buying back their shares, there have been no other real buyers in the market.

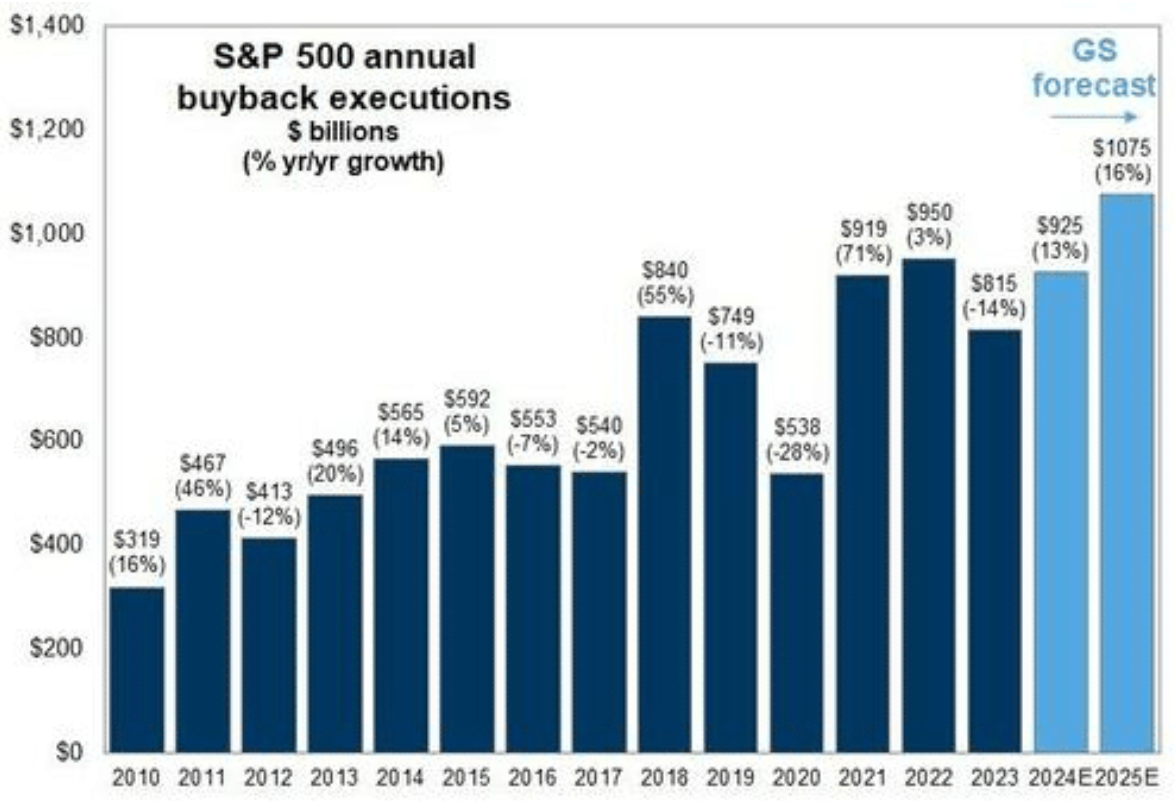

Given the increasing amount of corporate share buybacks, with 2024 expected to set a record, the importance of that activity has been a critical support for asset prices. As we noted in October 2023, near the bottom of the summer correction:

“Three primary drivers will likely drive markets from the middle of October through year-end. The first is earnings season, which kicks off in two weeks, negative short-term sentiment, and the corporate share buyback window reopens from blackout in November.”

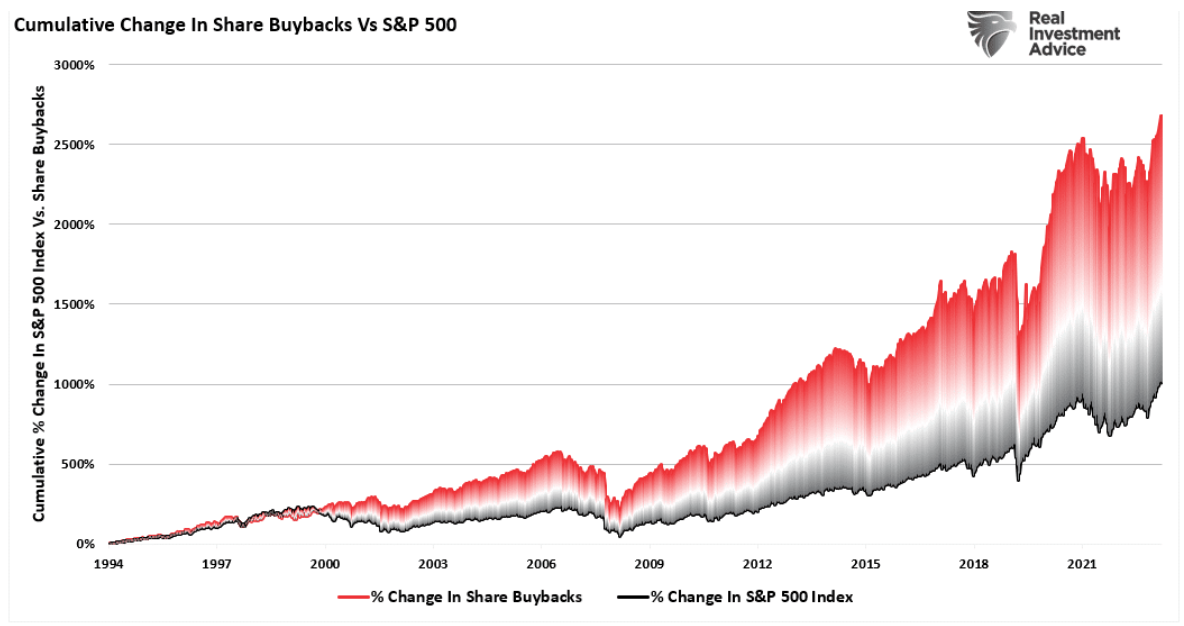

Notably, since 2009, and accelerating starting in 2012, the percentage change in buybacks has far outstripped the increase in asset prices.

As we will discuss, it is more than just a casual correlation, and the upcoming blackout window may be more critical to the rally than many think.

A High Correlation

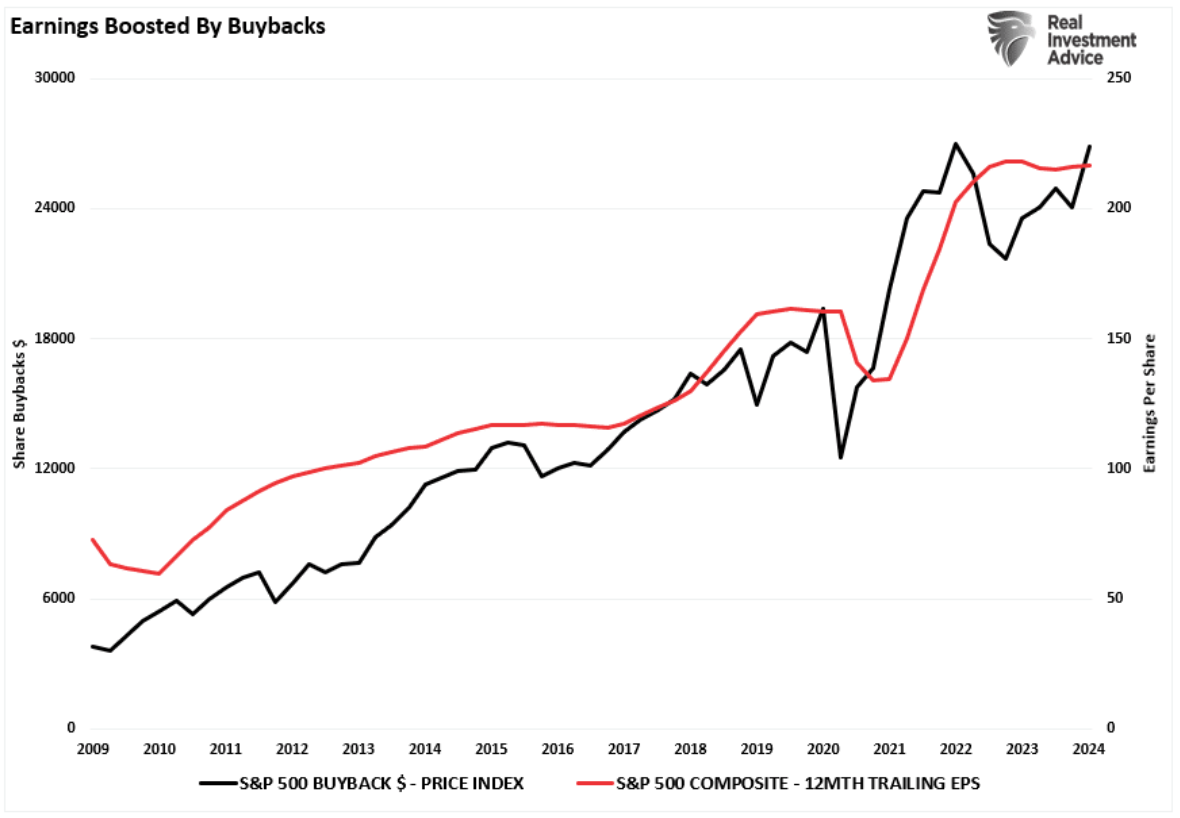

Unsurprisingly, the market rally that began in November correlated with a strong surge in corporate share repurchases. Interestingly, while the media touts the strong earnings growth shown in the recent reporting period, such would not have been the case without the surge in buybacks.

The result is not surprising given that the majority of earnings growth for the quarter came from the companies that are the most aggressive with share repurchases. However, given current valuation levels, it should make one question precisely what you are paying for.

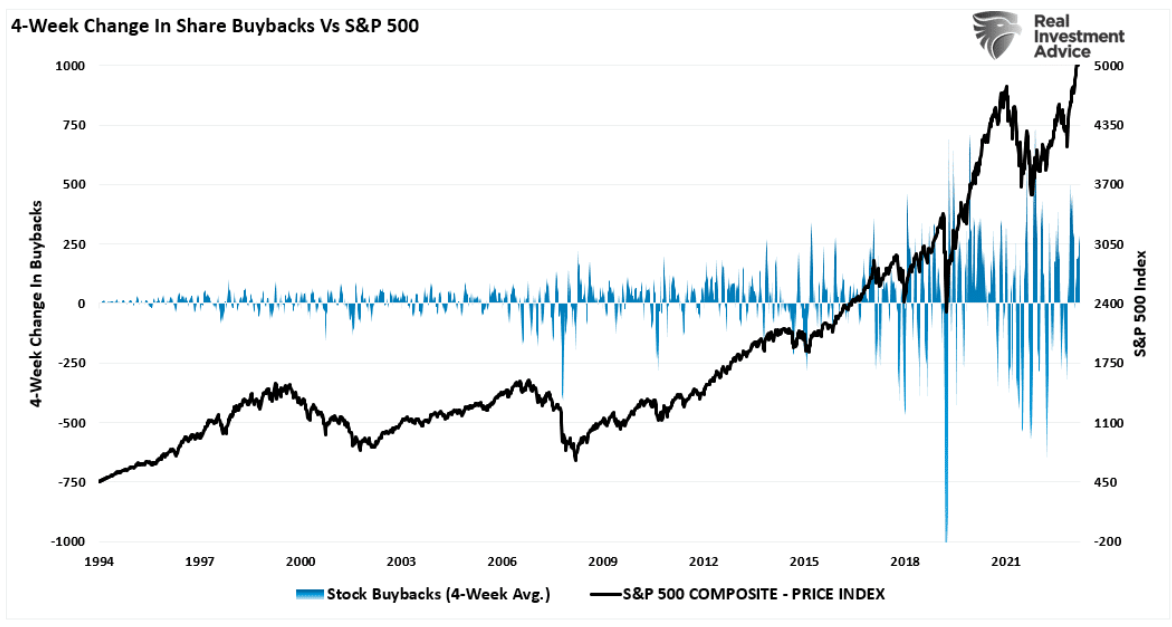

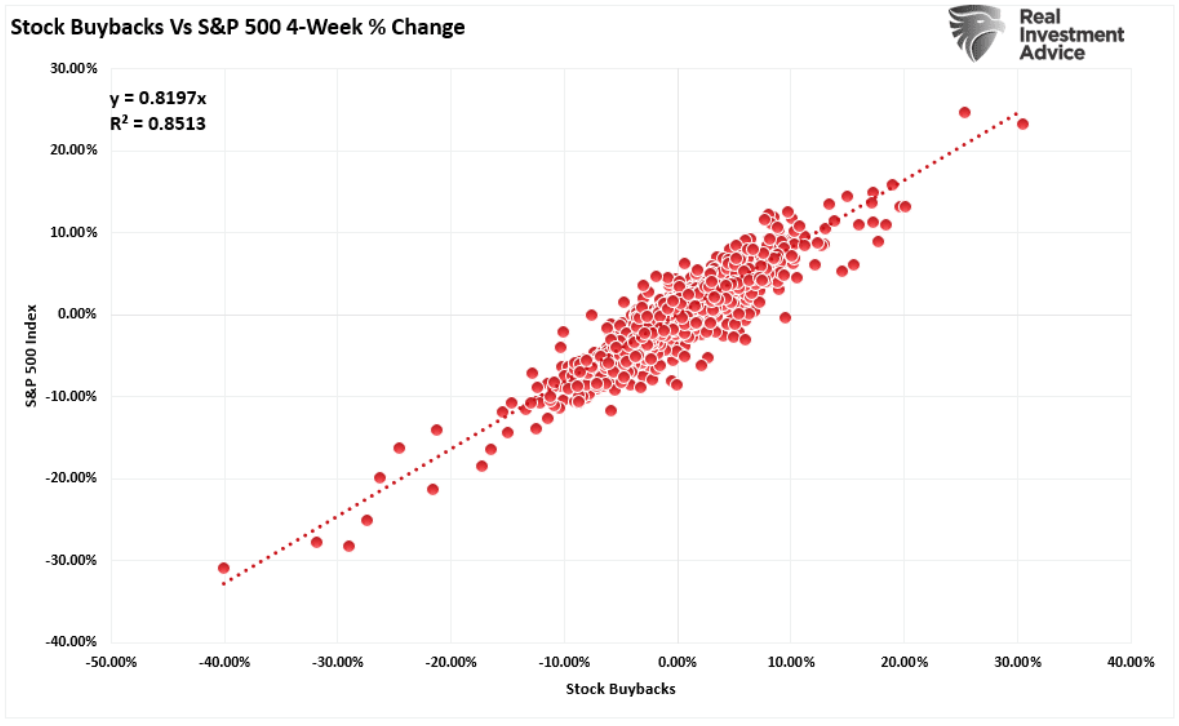

Nonetheless, the buyback surge has supported the market surge since the October 2023 lows. We saw the same at the bottom of the market in October 2022. The chart shows the 4-week percentage change in share buybacks versus the S&P 500.

The end of October tends to be the inflection point for the market, particularly over the last few years, because that is when the blackout period for share buybacks fully ends. While many argue that buybacks have little to do with market movements, a high correlation exists between the 4-week percentage change in buybacks versus the stock market. More importantly, since the act of share repurchases provides a buyer for those shares, the .85 correlation between the two suggests this is more than just a casual relationship.

Investors Are Really Bullish

Currently, investors are very exuberant about the current investing environment. As discussed in “Market Top or Bubble?”, little seems to deter investor enthusiasm.

“The ongoing ‘can’t stop, won’t stop’ bullish trend remains firmly intact.“

Investor sentiment is once again very bullish. Historically, when retail investor sentiment is exceedingly bullish combined with low volatility, such has generally corresponded to short-term market peaks.

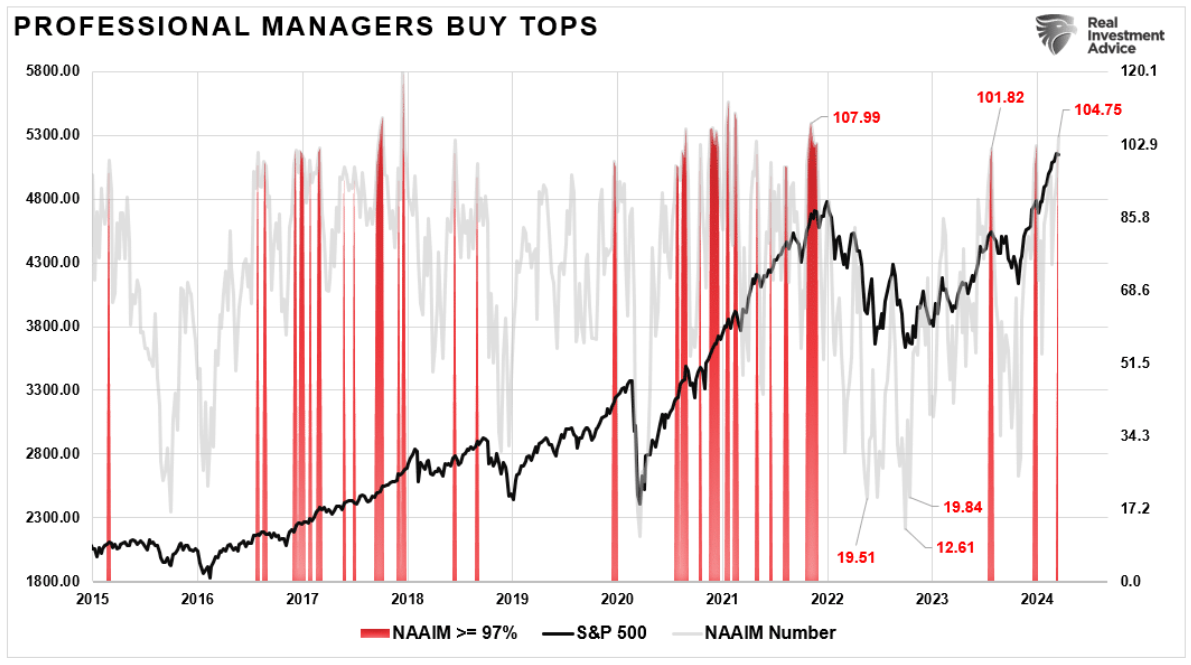

At the same time, professional managers are also very bullish and are leveraging portfolios to chase returns. When professional investor allocations exceed 97%, such has historically been close to short-term market peaks.

The risk to these more optimistic investors is that with the blackout period beginning, corporate demand, the largest buyers of equities, will drop by 35%. Therefore, given the correlation between buybacks and the market, a reversal of that corporate demand could lead to a market decline. Any decline will likely lead to a reversal of positioning by investors, further exacerbating that correction process.

While there is no guarantee of anything in the markets, it is likely a short-term risk worth paying attention to.

The Fed Will Support Buybacks

While the blackout of share buybacks may lead to a short-term market correction, the Federal Reserve may provide additional support over the long term.

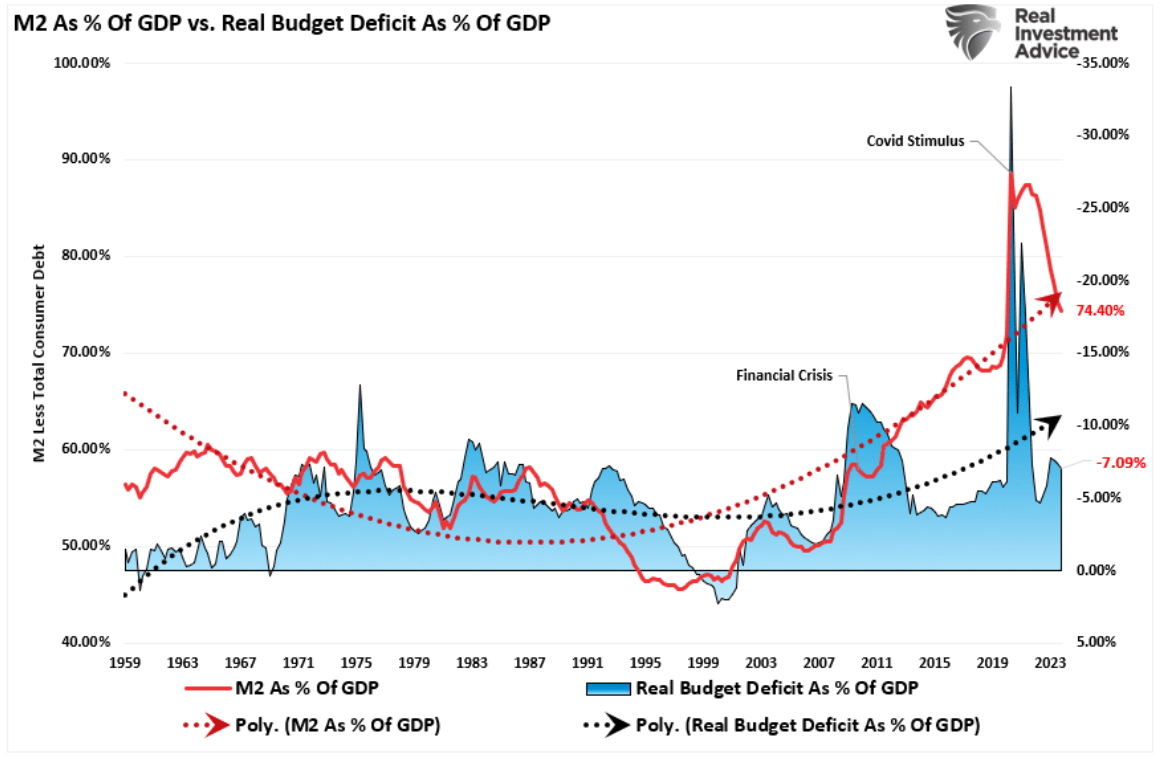

The Federal Reserve has been transparent and likely done with hiking interest rates for this cycle. Given the massive surge in the Fed funds rate, the economy has withstood that impact quite well. Of course, the reason was the enormous surge in fiscal support through deficit spending and a massive increase in the M2 money supply as a percentage of GDP.

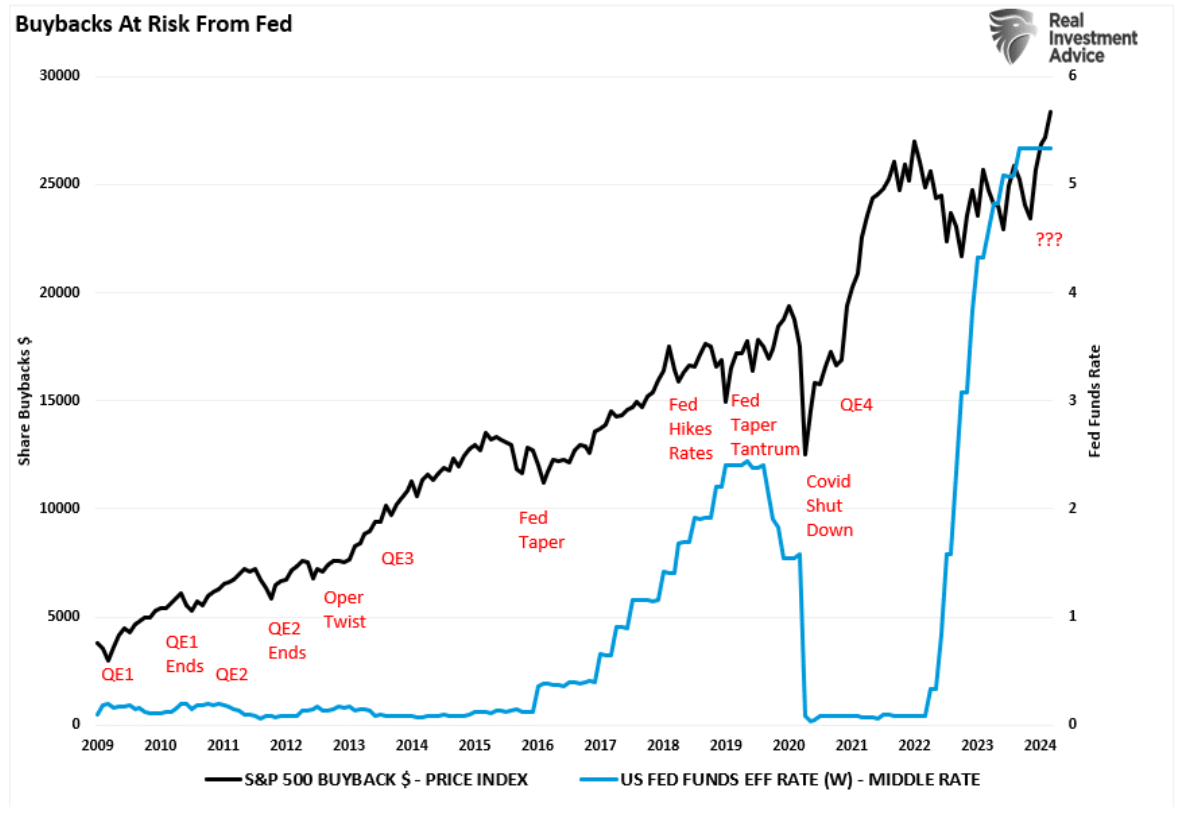

However, if the Federal Reserve lowers interest rates, it will reduce corporate borrowing costs, which has historically been a boon for share buybacks. Such is particularly the case for large corporations like Apple (AAPL), which can borrow several billion dollars at low rates and buy back outstanding shares. As shown, share buybacks rose sharply following the “Financial Crisis” but slowed during periods of higher rates. Corporations are now “front-running” the Federal Reserve in anticipation of increased monetary accommodation.

With corporate buybacks on track to set a new record this year, exceeding $1 Trillion, corporations will need lower rates to finance the purchases.

Conclusion

As we have discussed for the last month, the market is exceptionally bullish, extended, and deviated from long-term means. With the beginning of the “buyback blackout,” removing an essential buyer of equities is a risk worth watching.

Even if you are incredibly bullish on the markets, healthy bull markets must occasionally be corrected. Without such corrections, excesses are built, leading to more destructive outcomes.

What causes such a correction is always unknown. While the removal of buybacks temporarily may lead to a price reversal, those buybacks will return soon enough. And with $1 trillion in anticipated purchases, that is a lot of support for asset prices this year.

Does this mean the market will never face another “bear market?”

Of course not. There is a consequence for buying back shares at a premium. As Warren Buffet recently wrote:

“The math isn’t complicated: When the share count goes down, your interest in our many businesses increases. Every small bit helps if repurchases are made at value-accretive prices.

Just as surely, when a company overpays for repurchases, the continuing shareholders lose. At such times, gains flow only to the selling shareholders and to the friendly, but expensive, investment banker who recommended the foolish purchases.“

Eventually, the detachment of the financial markets from underlying economic realities will be reverted.

However, that is not likely a problem we will face between now and year-end.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors.

He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Disclosure

Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with over $1 billion in assets under management. As a team of certified and experienced professionals, we seek to provide our clients with educational services and the necessary information and tools to educate you in the field of finance, investing and economics. To this end, you can use the Real Investment Advice Platform to avail yourself of various video, audio and proprietary collections of information at your leisure to learn and gather the necessary information that you may need in the fields of investment news, investment opinion, financial news, financial opinion, economic news and economic opinion, finance, investing and economics. Utilizing the functionality and tools provided by Real Investment Advice, you can access this information in a variety of ways, including via video and audio programming, audio and visual media content streaming services, downloadable audio-visual media, uploaded, posted or tagged third-party videos, receiving or viewing audio and video clips, blogs, podcasts, and YouTube videos, all of which are accessible on the Real Investment Advice media platform and/or various Internet and communications links that are accessible via the Real Investment Advice Platform and allow for the broadcasting, transmission and streaming of the information and audio-visual content to your media devices and other communications platforms for your viewing and listening pleasure. All of these tools and sources of information are made available to you so that you can utilize the same to make the right financial, economic and investment decisions.

RIA Advisors offers multiple custodial arrangements, either directly of through wholly owned subsidiaries, with Fidelity and Interactive Brokers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All