Eight years after turning to negative interest rates and 17 years after its last rate hike, the Bank of Japan (BoJ) raised rates into positive territory this week. The move ended the most aggressive monetary stimulus program in recent times, and marks the end of the era of negative interest rates.

The small rate adjustment was part of a comprehensive change to monetary policy. The meeting also saw the end of yield curve controls on Japanese government bonds (JGBs). The central bank ended purchases of exchange-traded funds and domestic real estate investment trusts.

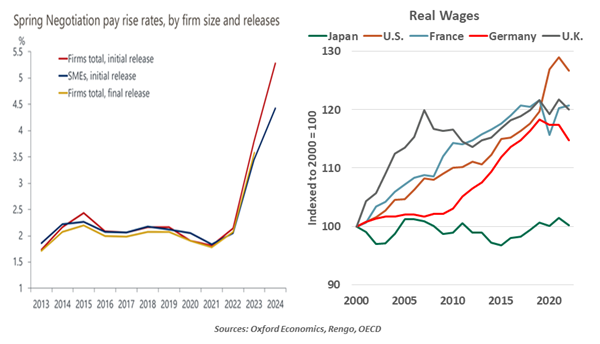

Inflation brought about the end of the negative rate regime, and its drivers were varied. The pandemic, the Ukraine war and weaker domestic currency values all helped Japan exit from entrenched deflationary pressures. The annual Shunto spring wage negotiations delivered the biggest pay increase in more than three decades, gave the BoJ further conviction about the sustainability of inflation.

DISRUPTIONS FROM COVID AND THE UKRAINE WAR DELIVERED WHAT DECADES OF MONETARY AND FISCAL POLICY COULDN’T.

The strong wage settlement amid labor shortages will boost real wages and underpin underlying price pressures, supporting the case for further hikes. But Japan’s room for aggressive tightening is limited. The economy lacks clear drivers of growth, and inflation expectations are not anchored at the 2% target. Actual inflation is likely to drop back below 2% by the end of next year. This was the reason the BoJ stressed that monetary policy will continue to remain easy for the time being, and that the bank will continue to purchase JGBs.

Higher interest rates would make it harder for the government to finance the country’s massive debt, which is twice the size of its economy and the largest among developed nations. Businesses could also be shocked by higher borrowing costs. Narrowing interest rate differentials will lead to a stronger yen, which will counteract inflation and lower export earnings.

Japan has exited a prolonged period of deflation and its workers secured strong pay increases, but the virtuous cycle between wages and prices won’t become permanent until the economy addresses its long-term structural challenges. The era of negative interest rates in Japan has ended, but the march towards a neutral policy stance is ongoing.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© Northern Trust

Read more commentaries by Northern Trust