A Story About the Drongo, the Meerkat and Debt Markets

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsOn the plains of Africa you’ll find a surprising cooperation between two typically adversarial animals—the drongo bird and the meerkat. What makes the relationship especially vexing is that they both covet the same food. But instead of being fierce adversaries, they maintain a symbiotic partnership. When predators to the meerkat are in the vicinity, the drongo bird will give out a warning cry, alerting the spirited mammals of the danger. The meerkats quickly scurry back to their burrows, and in their haste often drop a bit of food. The drongo swoops in and grabs the free meal, while the meerkat huddles in his hole avoiding the predator. A win-win.

In a similar manner (albeit generally not on the plains of Africa), the relationship between broadly syndicated loans (BSL) and direct lending (DL) could be considered more symbiotic than adversarial as well. While in recent months the media has presented it as an either-or situation, with headlines like “Private credit’s golden era may face strain amid a resurgence in the BSL market,”1 it is not necessarily so binary. In many instances borrowers can have their BSL cake and eat DL as well.

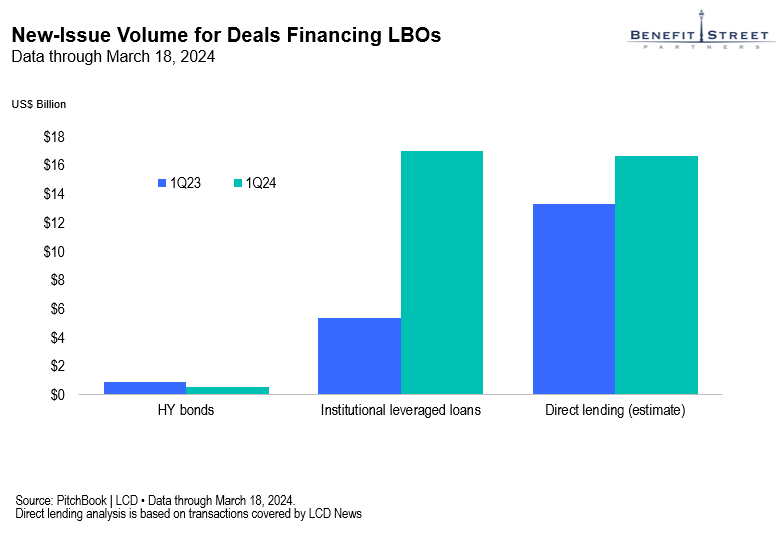

Increased deal flow—a win for credit investors

As banks increase their risk appetite, which they have in recent months given the strong macroeconomic backdrop, they will start putting more capital into the market in the form of BSL commitments. This bank action in some ways acts as a lubricant for the merger-and-acquisition (M&A) machine. The animal spirits come back and the pie grows. While DL may lose some share of the market to BSL as a result, in my experience there are enough deals with enough spread to keep both the drongo fat and the meerkat happy (Exhibit 1).

Any competition between BSL and DL, when it does occur, tends to happen in the upper middle market—companies with EBITDA2 >US$100 million. Direct lenders in that portion of the market may lose some market share and see spreads compressed. However, the core middle market—companies with EBITDA between US$25 million-US$100 million—will still benefit from increased deal flow, as financial sponsors (the lifeblood of this segment) get more comfortable doing deals after a period of dormancy. It is still a win-win. Business media outlets like Bloomberg and others tend to underreport these middle-market transactions, because they lack the sensational value of a US$1 billion+ headline. These under the radar transactions are where alpha may be captured. For example, the core middle market still has a healthy, albeit diminished, illiquidity premium. In contrast, the upper middle market has seen its illiquidity premium over syndicated deals get squeezed significantly.

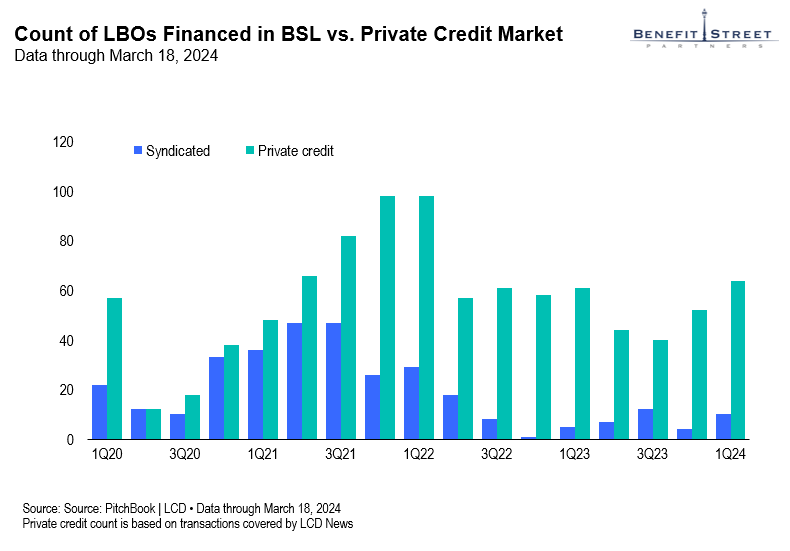

The bottom line is that it doesn’t have to be a binary selection between BSL or DL debt for allocators—there are opportunities in both. We see in Exhibit 2 that private credit deals continued to grow in number over the first quarter of 2024.

Exhibit 2: Direct Lending Is not Going Away

Ardonaugh Group Ltd. —Symbiosis demonstrated

The symbiotic relationship between BSL and DL is even more direct in some situations. More recently we are seeing deals that have both a BSL and DL structure. For example, in February of this year Ardonaugh Group Ltd.3 recapitalized its business with both DL and BSL components in the financing.

This practice isn’t abnormal. For many years, the typical LBO would have a first lien BSL component provided by collateralized loan obligations (CLOs), and a junior second-lien component provided by direct lending firms. Eventually lines got blurred and these structures became blended unitranche deals, where everyone was competing for the same pie. Today we’re seeing a return of second-lien deals, such as the financing to support the leveraged buyout of Truist Financial Corp.’s insurance business.4 In my view, this practice is a better way of slicing the pie—the risk gets allocated appropriately. Those who want lower risk (BSL lenders) get the lower risk senior debt (first lien), and those seeking higher spread get the second-lien junior debt.

Not always win-win: Covenant-light growth may be warning sign

While both BSL and DL can coexist in the same market, there can be a downside to increased competition between the two debt structures. When markets get more competitive in the upper- middle-market segment, we often begin to see more risk-taking. Symptoms of froth, such as a lack of financial maintenance covenants (cov-lite) in documents, may become more frequent in DL structures. This should be the exception not the norm. This heightened risk can spread to the core middle market as well, which is not fully immune from these trends despite being more sheltered from competition.

In conclusion, increased activity in the BSL space is not necessarily a bad thing for DL, and vice versa. They can coexist and even complement each other, providing a variety of financing options for different risk appetites. It is not an either/or condition, it is both/and. Even birds and cats get along sometimes.

Definitions

Broadly syndicated loans (BSLs) are a form of financing where a syndicate of lenders work together to provide a large loan to a single borrower.

Direct syndicated loans (DSLs) are a type of syndicated loan where the syndicate of lenders provides funds directly to the borrower without the use of an intermediary or arranger.

A first lien refers to the legal right of a creditor to be the primary claimant against the assets of a borrower if the borrower defaults on the loan. This means that in the event of a default, the holder of the first lien has the first priority to seize and sell the borrower’s assets to recover the owed amount.

A second lien is a type of debt that is subordinate to a first lien, meaning it has a lower priority in terms of repayment in the event of a borrower’s default or asset liquidation. If a borrower defaults, any second-lien debt gets paid only after the first or original first lienholder is paid off.

A blended unitranche refers to a type of debt financing that combines senior and subordinated debt into a single loan structure with a blended interest rate. This hybrid loan structure simplifies the borrowing process by providing a single set of terms for the entire debt amount, rather than having separate agreements for each tranche of debt.

Collateralized loan obligations (CLO) are securities backed by a pool of debt, often low-rated corporate loans.

A leveraged buyout (LBO) is the purchase of a company away from its outside equity shareholders by its management, financed by means of that company issuing a large amount of debt to cover the cost of the purchase.

Liquidity refers to the degree to which an asset or security can be bought or sold in the market without affecting the asset’s price.

A syndicated loan is a loan offered by a group of lenders (called a syndicate) who work together to provide funds for a single borrower.

WHAT ARE THE RISKS?

All investments involve risks, including possible loss of principal.

Equity securities are subject to price fluctuation and possible loss of principal.

Fixed income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. Changes in the credit rating of a bond, or in the credit rating or financial strength of a bond’s issuer, insurer or guarantor, may affect the bond’s value. Low-rated, high-yield bonds are subject to greater price volatility, illiquidity and possibility of default.

Investments in many alternative investment strategies are complex and speculative, entail significant risk and should not be considered a complete investment program. Depending on the product invested in, an investment in alternative strategies may provide for only limited liquidity and is suitable only for persons who can afford to lose the entire amount of their investment. An investment strategy focused primarily on privately held companies presents certain challenges and involves incremental risks as opposed to investments in public companies, such as dealing with the lack of available information about these companies as well as their general lack of liquidity.

Diversification does not guarantee a profit or protect against a loss.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com

___________________

1. Source: “Moody’s Says Private Credit Returns Will Be Pressured by Banks.” Bloomberg. March 5, 2024.

2. EBITDA = Earnings before interest, taxes, depreciation, and amortization.

3. Source: “Banks Spoil Private Credit’s Record Ardonagh Deal With $2 Billion Bond.” Bloomberg. February 4, 2024.

4. Source: “Market Shift: $1.9 Billion Second-Lien Loan for Truist Insurance LBO Signals Resurgence.” Supernews. March 1, 2024.

Copyright © 2024 Franklin Templeton. All rights reserved.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All