Parents of young children will recognize the danger of a one-word question: “Why?” By persistently asking why, a child can frustrate and unravel the thinking of their caregivers.

We are re-learning the power of that simple question. We had expected the Federal Reserve to start cutting rates in June. But as more of our audiences asked why, we saw the case was not strong. This week’s inflation reading seals the deal: we now expect the easing cycle to start in September.

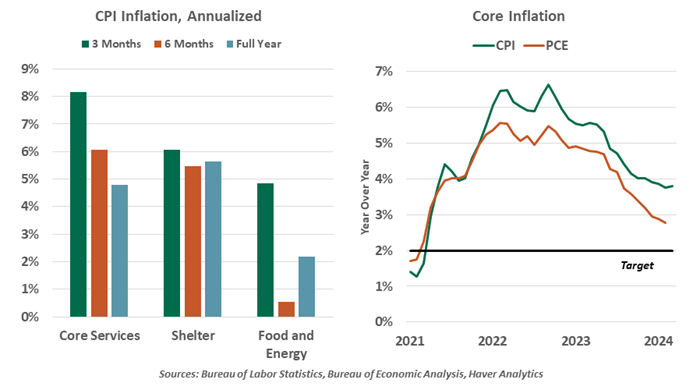

The consumer price index (CPI) for March was above expectations, rising 0.4% for the month on both a headline and core basis. The details were all too familiar: shelter inflation remains stubbornly elevated. Core services excluding housing ticked upward, led by volatile categories like vehicle maintenance and insurance. On a year over year basis, core service prices have been rising since October 2023; components of this category share a common dependency on labor. New immigration has not yet relieved the limited supply of skilled workers, and their wage gains are passing through to prices.

While the Fed targets personal consumption expenditure (PCE) inflation rather than CPI, the two indices have moved in tandem in this cycle. And while the target excludes the volatile categories of food and energy, higher gasoline prices will keep this matter top-of-mind for consumers.

FIRM INFLATION ADDS TO THE REASONS FOR THE FED TO DEFER RATE CUTS.

Another factor arguing against reducing rates is the persistent strength of the American economy. In 2019, the Fed cut rates by 75 basis points in anticipation of weakening growth. We see no softening today, and no need for a similar proactive cut. Employment and personal income are both exceptionally strong. Sectors that were shocked by the rise in interest rates, like banking and homebuilding, have adjusted to the new rate regime. Risk assets are rallying, credit spreads are narrow, and financial conditions are easy.

The Fed has emphasized their data-dependent approach, but they do risk putting too much weight on recent readings. The uncooperative start to 2024 follows a good disinflationary run in 2023. The risk of a new reflationary cycle remains low, absent any further supply shocks. A dovish policymaker could make a case for cuts in light of the long-run improvement. On this basis, we do still expect to see easing later in the year. However, the current Fed governors remain committed to their objective of taming inflation. Further progress will be needed, more than can be seen between now and June.

The last mile of the inflation recovery always loomed to be the hardest. Initial progress down from the peak was easy as stimulus programs ended and supply chains healed, but the remaining distance will require policy discipline. If we ultimately achieve a soft landing, holding rates higher for even longer will be an important reason why.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust