If 2023 for Asia-Pacific (APAC) economies was about navigating challenges ranging from aggressive tightening of monetary policy to China’s economic deceleration, this year will be defined by stability, paving the way for more durable growth in 2025.

Improving domestic demand along with recovering tourism are underpinning economic activity in the region. Underlying inflation momentum has eased. Japan has exited from 25 years of deflation. Regional central banks have been reluctant to start cutting rates ahead of the Fed, fearing capital outflows and currency turbulence. But the Fed’s expected rate cuts later on this year should allow them to pivot. China is an outlier, struggling to reflate an economy besieged by deflation, a protracted property market slump and waning investor confidence.

APAC faces multiple risks: policy uncertainty, China’s slowdown, volatile energy markets and restrictive monetary conditions. Risks of geopolitical fragmentation are particularly onerous for APAC, given these nations’ integration into global value chains.

Following are our views on how major regional markets are poised to perform during the balance of 2024.

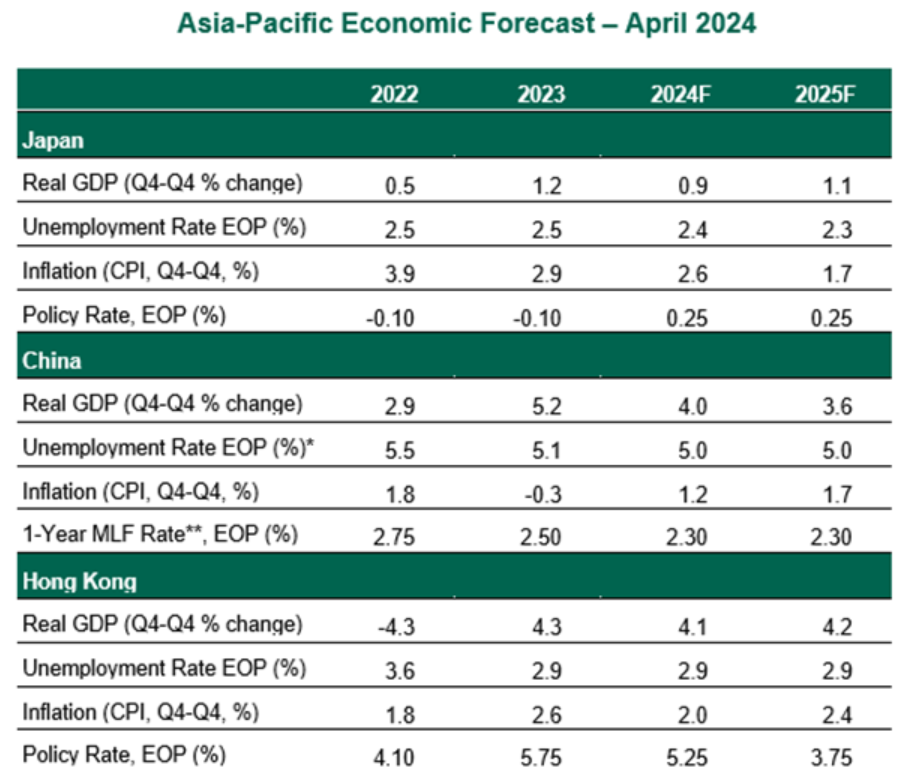

Japan

- Japan avoided a technical recession at the end of 2023 as the economy lacked a clear driver of growth. But we expect momentum to recover in the coming quarters, led by gradual improvement in all three key drivers of growth. Consumption, which contracted for three quarters in a row, will get a boost from large wage increases secured by workers in the spring negotiations. Investment and exports will be underpinned by a continued upturn in the chip cycle.

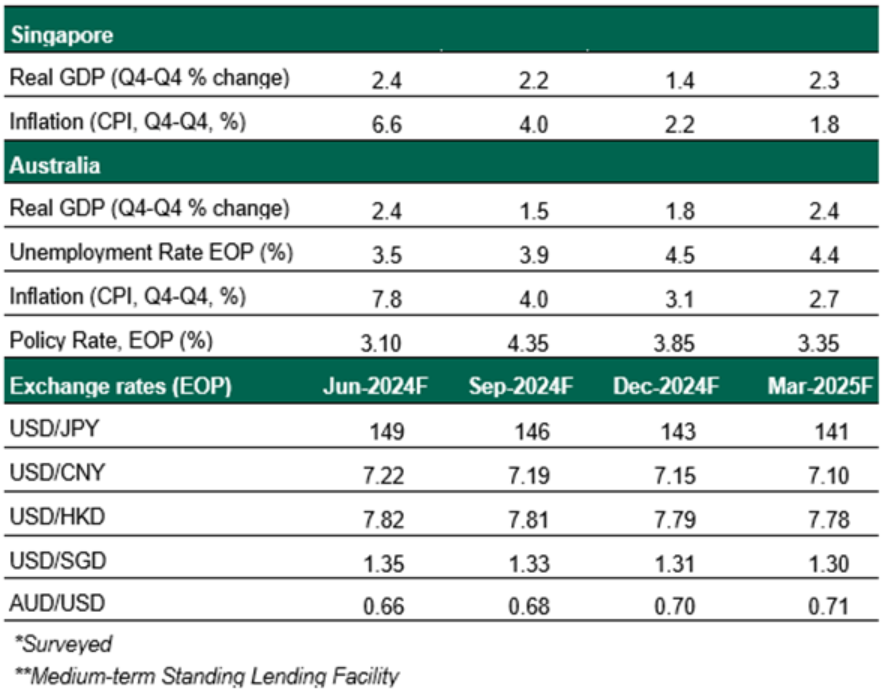

- The wage settlement also provided impetus to the Bank of Japan (BoJ) to abolish its yield curve control and negative interest rate policies. But room for aggressive tightening is limited as rapid adjustments to the policy rate will generate market volatility and complicate public debt dynamics. Contrary to fundamental expectations, the dovish hike by the BoJ has put the yen under pressure. The yen slid to its lowest level since 1990 against the dollar recently, triggering speculation of more than a verbal intervention by Japanese policymakers.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust