My first professional turn as an economist came when I worked in consulting. And I do mean worked: Late nights and weekend deadlines were routine. In contrast, the work-life balance of bank employment has been a tremendous relief. With rare exceptions, weekend time is our own.

One memorable exception came last March, as the failure of Silicon Valley Bank (SVB) carried the risk of contagion to the entire financial sector—as I learned while on an emergency Sunday conference call. High stress endured through the closure of First Republic Bank on May 1, 2023.

A year later, we can see that weekends across the financial sector are more relaxed. Last week, the Federal Reserve published its semiannual Financial Stability Report. The report was broadly encouraging, noting that banks maintain capital ratios well above statutory minimums, with ample liquidity. Bank profits have been stable in spite of a volatile rate environment, as interest income has nearly kept pace with rising interest expense. Deposit outflows were a point of great concern in the wake of SVB, but they stabilized and returned to net inflows in the fourth quarter of 2023.

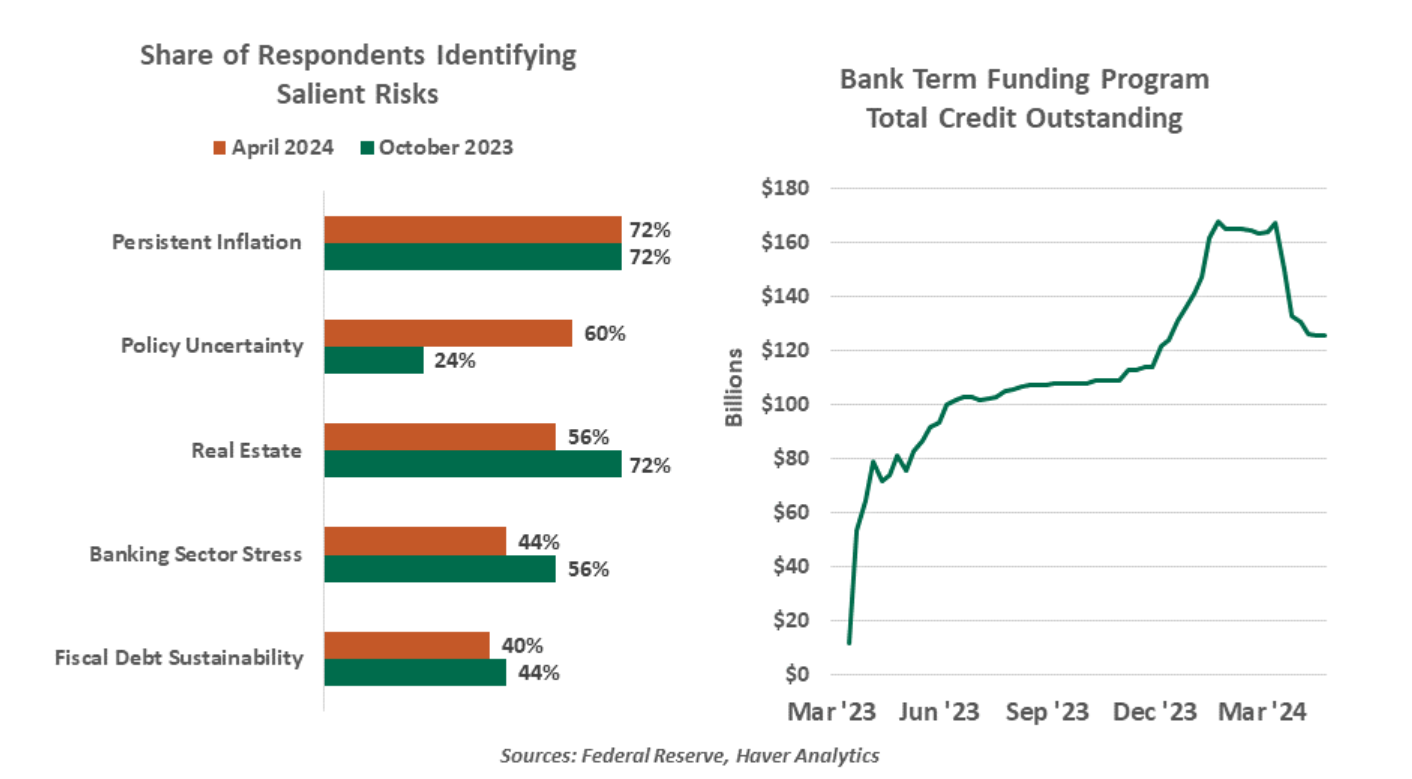

Still, the report noted a bevy of risks: Banks carry unrealized market value losses on their fixed-income portfolios. Office commercial real estate is an albatross for many lenders. Subprime consumer credit delinquencies are on the rise, as are some small business loans. Financial sector participants reported inflation and its corresponding impact on monetary policy as the top risk.

PRESSURE ON THE BANKING SYSTEM HAS DIMINISHED OVER THE PAST YEAR.

The report also spotlighted the Bank Term Funding Program (BTFP), the Fed’s special facility launched to ameliorate last year’s distress. After injecting $168 billion of liquidity into the system, BTFP was closed on schedule this past March; its loans will wind down to zero by March 2025. We have now learned that BTFP extended advances to 1,804 depository institutions, 95% of which were institutions with total assets below $10 billion.

This suggests that the liquidity challenges facing the system last year were fairly widespread. The BTFP provided a very effective bridge to a more normal environment, and will likely be resurrected in the event of future financial instability.

In sum, risks facing the U.S. banking system are still present, but they are well-understood and not nearly as pressing as they were a year ago. That should keep our weekends clear.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Northern Trust

Read more commentaries by Northern Trust