Strong Q1 earnings were a bright spot as sticky inflation and dimmed expectations for rate cuts cast some shade on U.S. equity markets. Fundamental Equities investor Carrie King looks beyond the headlines to offer four takeaways from the most recent earnings season.

1. Tech+ shines again

S&P 500 earnings growth of 5% was driven primarily by the mega-cap tech+ stocks. Removing the top seven index constituents by market cap brings index earnings growth to -2% for the quarter.

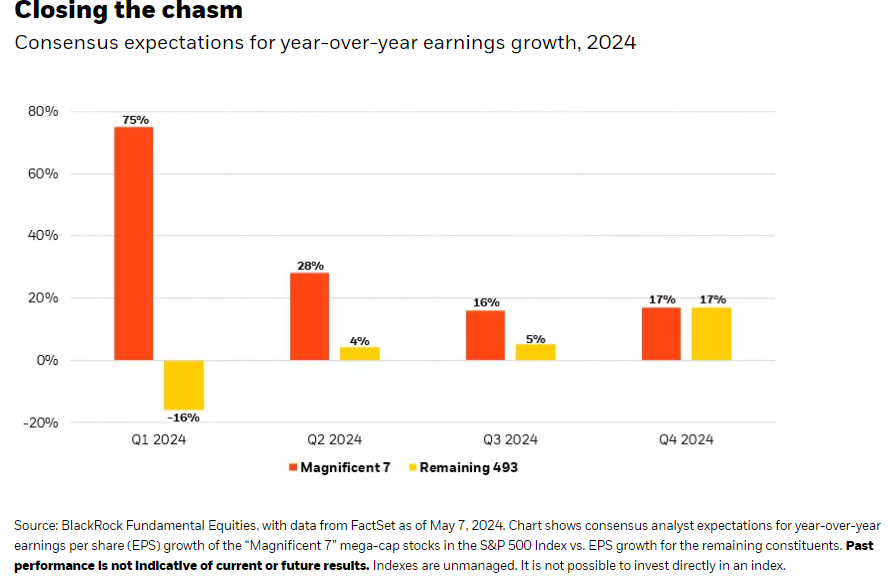

We remain positive on technology and internet stocks but expect the earnings growth chasm between these leaders and the rest to close as two divergent business cycles each normalize. The tech-led cycle is ahead of the broader market, having soared, declined and reaccelerated since COVID. Other sectors are just now working off their pandemic malaise and looking to a brighter future, as we discussed last quarter. We expect the earnings growth of the rest of the market to catch up to today’s leaders by the end of this year, as shown in the chart below.

Amid the broadening, we see opportunity for stock pickers to parse through the fundamentals to identify those companies with the potential to lead in the next leg of the business cycle.

Investment takeaway: Broaden your investment lens as the earnings growth gap narrows and opportunities open in other areas of the economy. We prefer healthcare, where innovation is robust and valuations are below the market average. We also see improving prospects in industrials as years of underinvestment are poised for reversal. The American Society of Civil Engineers calculates an infrastructure spending gap of about $2.5 trillion, and the federal government is demonstrating bipartisan support for helping to close it. Momentum here should present stock selection opportunities among industrials.

2. Capex pours in

Not only are tech companies earning, but they are also spending. S&P 500 capex this quarter was up 10% year-over-year (yoy) versus 4% in Q4, according to Bank of America analysis. Artificial intelligence (AI) is the driver.

Hyperscalers, a term applied to the largest cloud service providers, have all signaled increased capex. Overall spending on AI infrastructure and cloud is set to rise this year and accelerate even further in 2025. Our Global Technology team’s estimates of hyperscaler capex are well above Wall Street consensus estimates, consistent with their higher estimates of AI data center power demands.

A company’s stock price is often punished with the announcement of capex spending. We saw it this quarter when one of the Mag 7 hyperscalers had impressive earnings alongside big capex intentions. But there’s a difference between spending and success-based spending. While some capex may be ill-fated when business plans don’t pan out, capex applied to high-potential initiatives can reap rewards. We believe capex directed at generative AI advancement has major tailwinds that should validate the spend and multiply into returns given AI’s potential to transform businesses across the economy.

Investment takeaway: As spending on AI infrastructure increases and enables greater penetration of the technology, look for opportunities in the next layers of the AI technology stack. We see great potential in companies that supply data ― the fuel that allows AI to work ― and those that provide the memory to store it.

3. Clouds gather for consumers

We’ve noted before the signs of stress seen in the consumer. Those signs are starting to flash red in spots, particularly among the lower-income cohort. A major fast-food chain cited the word “value” 60 times in its Q1 earnings remarks, 4x more than last quarter ― a point Lisa Yang, co-head of our Fundamental Equities consumer group, made on a recent episode of The Bid podcast.

Consumer confidence, as measured by the Conference Board, fell to its lowest since July 2022 in April. Survey data also showed dips in buying plans for homes and big-ticket appliances as well as declines in vacation plans.

Inflation and higher rates have consumers watching their discretionary spend. Some companies are noting the softening in their earnings guidance, citing the end of the COVID stimulus and restart of student loan debt repayments that had been on a pandemic-era hiatus.

COVID aftereffects are playing out in other areas as well. We’re seeing inventory destocking in places like autos and semiconductors. Some chips (those needed for AI optimization) are doing great, but not the ones used in smart phones and other electronic equipment, for example, which had a renewal cycle during COVID ― pressuring supply then and resulting in an inventory glut now as companies had overordered into a demand decline.

Investment takeaway: Be wary and be selective. In consumers, we look for resilient companies that have strong competitive advantages and healthy balance sheets to prevail and grow market share no matter the economic backdrop.

4. Brightening skies for healthcare

The healthcare sector saw the lowest yoy earnings growth (-26%) for the quarter, sitting at the bottom alongside energy and materials. Yet this paints only a partial ― and overly bleak ― picture. A couple of notable outliers, one taking temporary losses on M&A expenses, dragged on the averages.

Yet the healthcare sector had a high percentage of sales and earnings per share (EPS) beats for the quarter, at 72% and 89%, respectively. This compared to sales beats of 63% and EPS beats of 83% for the S&P 500 broadly. We believe the trend is positive in the sector as lingering COVID-related effects are worked off in some places and innovation abounds in others. This could bode well for the undervalued defensive sector after a long stretch of underperformance.

Investment takeaway: Valuations are compelling and the healthcare sector offers a good mix of defense and growth through innovation. Stock picking is important. Case in point: Amid a looming flood of patent expirations in the U.S., we prefer European pharmaceuticals given a stronger patent expiry profile. Drug distributors are attractive, as they benefit when large-cap pharma companies lose patent protection, allowing them to distribute an increasing volume of generics, which have a more attractive margin profile.

Long-range forecast

A positive earnings growth outlook (see chart above) bodes well for U.S. stocks overall. Yet the nature of the outlook is particularly favorable for stock selection, in our view. As a highly concentrated market grows broader and more diverse, we see opportunity for skilled stock picking to parse potential leaders and laggards in pursuit of returns beyond that offered at the index level.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© BlackRock

Read more commentaries by BlackRock