Benchmarking Your Portfolio May Have More Risk Than You Think

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDuring ripping bull markets, investors often start benchmarking. That is comparing their portfolio’s performance against a major index—most often, the S&P 500 index. While that activity is heavily encouraged by Wall Street and the media, funded by Wall Street, is benchmarking the right for you?

Let’s begin with why Wall Street wants you to compare your performance to a benchmark index.

Comparison-created unhappiness and insecurity are pervasive, judging from the amount of spam touting everything from weight loss to plastic surgery. The basic principle seems to be that whatever we have is enough until we see someone else who has more. Whatever the reason, comparison in financial markets can lead to terrible decisions.

This ongoing measurement against some random benchmark index remains the key reason investors have trouble patiently sitting on their hands and letting whatever process they are comfortable with work for them. They get waylaid by some comparison along the way and lose their focus.

Clients are pleased if you tell them they made 12% on their account. Subsequently, if you inform them that “everyone else” made 14%, you’ve upset them. As it is constructed now, the financial services industry is predicated on upsetting people so they will move their money around in a frenzy.

Therein lies the dirty little secret. Money in motion creates revenue. Creating more benchmarks, indexes, and style boxes is nothing more than creating more things to compare against, allowing clients to stay in a perpetual state of outrage.

This also explains why “indexing” has become a new mantra for financial advisors. Since most fund managers fail to outperform their relative benchmark index from one year to the next, advisors suggest buying the index. This is particularly true as the increasing market share of indexing (and passive, or systematic, investing in general) has made markets less liquid.

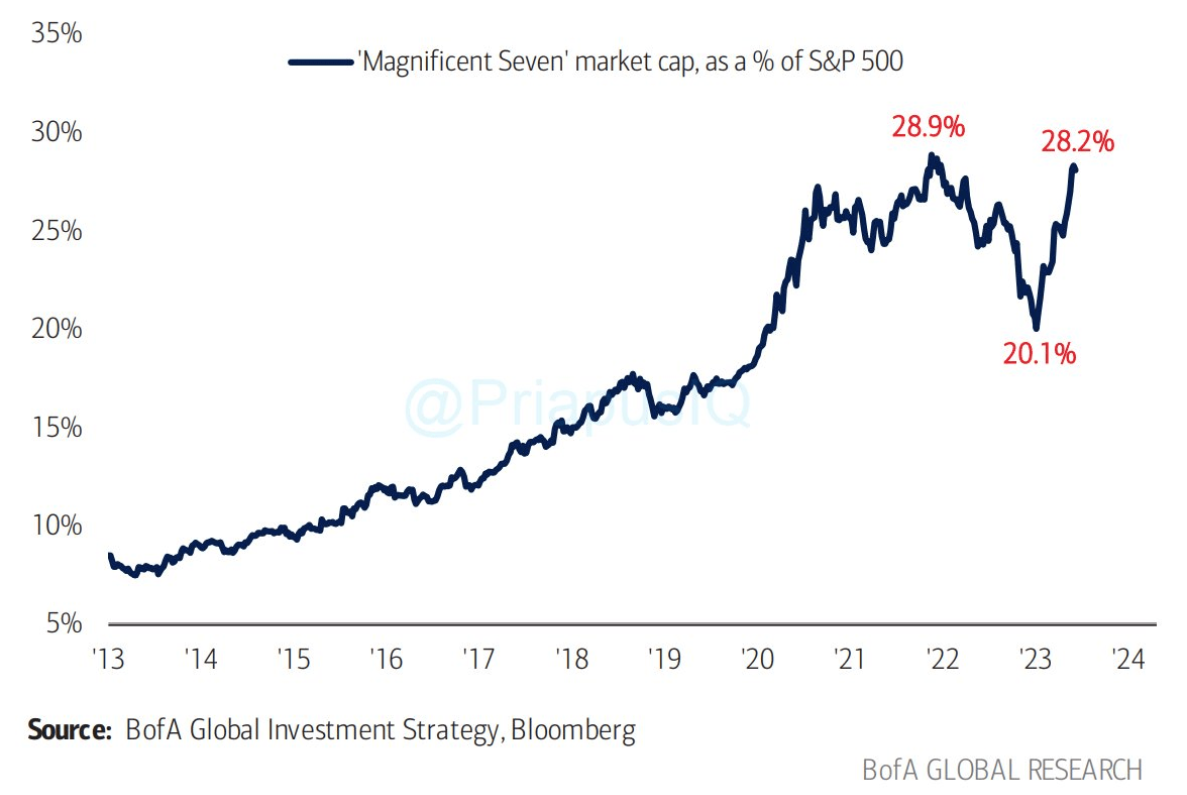

However, the rise in indexing has resulted in a concentration of dollars into a decreasing number of assets. The combined market capitalization of the top seven companies in the S&P 500 index is around $12.3 trillion. That is more than four times the size of the nearly $3 trillion market capitalization of the Russell 2000 Index, which consists of 2,000 small-cap stocks.

While that statistic may be shocking, it also represents the most significant risk in benchmarking your portfolio.

Market Cap Weighting Your Portfolio

When most investors or financial advisors build portfolios, they invest in companies they like. They then compare the portfolio’s performance to an index. This benchmarking process is where the risk lies, more so today than previously. The reason is in an article we wrote previously:

“In other words, out of roughly 1750 ETF’s, the top-10 stocks in the index comprise approximately 25% of all issued ETFs. Such makes sense, given that for an ETF issuer to ‘sell’ you a product, they need good performance. Moreover, in a late-stage market cycle driven by momentum, it is not uncommon to find the same ‘best performing’ stocks proliferating many ETFs.”

The issue of asset consolidation is exacerbated as investors buy shares of an indexed ETF or mutual fund. Each purchase of a passive index requires the purchase of the shares of all the underlying companies. Therefore, the rise in the overall index is unsurprising. The massive inflows into passive indexes force-fed the top-10 market capitalization-weighted companies.

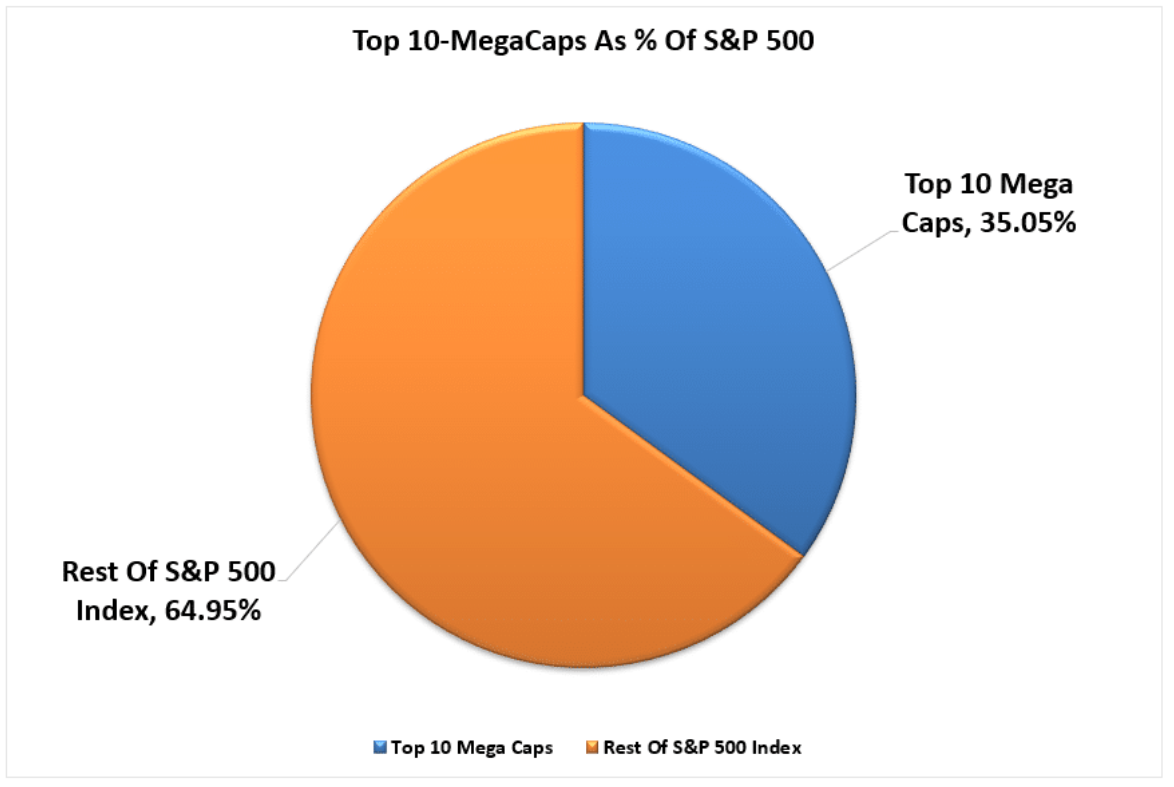

Here is how it works. When $1 is invested in the S&P 500 index, $0.35 flows directly into the top 10 stocks. The remaining $0.65 is divided between the remaining 490 stocks.

Investors who benchmark their index risk failing unless 35% of the portfolio is invested in those 10 stocks. With the market capitalization weighting of the largest companies nearing a record, taking on a 35% stake in those companies increases the portfolio’s risk profile significantly more than many investors think.

Notably, we are discussing only the risk involved in “matching” the index.

Trying to beat the index consistently from one year to the next is a far more challenging process.

A perfect example is Bill Miller from Legg Mason, who achieved 15 consecutive years of beating the S&P. That put him on the cover of magazines. Investors poured billions into the Legg Mason Value Fund in 2005 and 2006. Unfortunately, that was just before his strategy ran into headwinds and stopped working. The same occurred with Peter Lynch at Fidelity.

Here is the point. The probability of beating the S&P for 15 consecutive years is 1 in 2.3 million.

A Well Managed Portfolio Can Beat The Index Over The Long Term

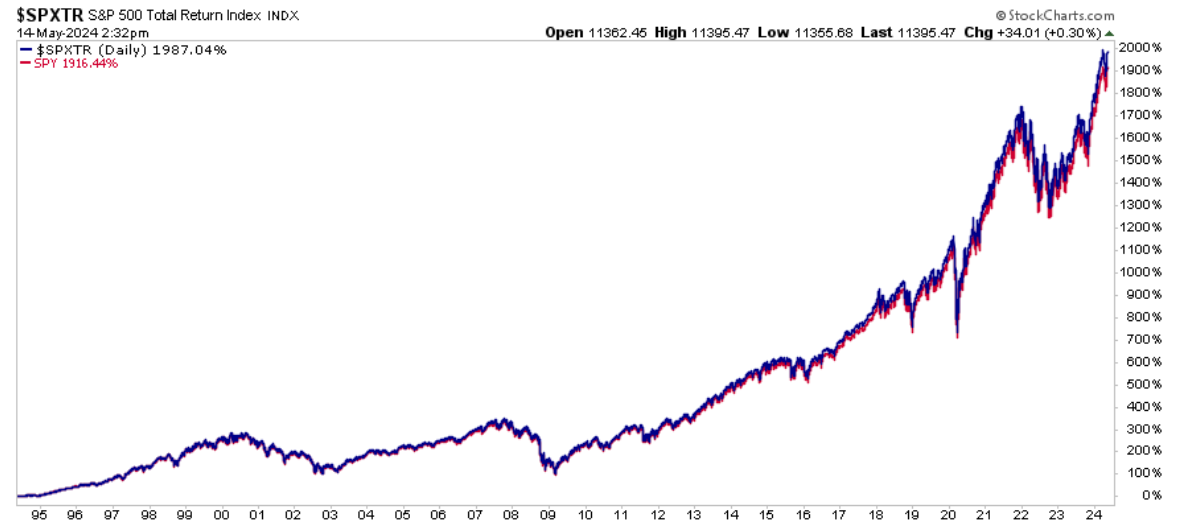

The problem with mainstream benchmarking analysis is that it always focuses on the trailing one-year performance. The reality is that even if you buy an index, you will still underperform it over time. Over the last 30 years, the S&P 500 Index has risen by 1987% versus the ETF’s gain of 1916%. The difference is due to the ETF’s operating fees, which the index does not have.

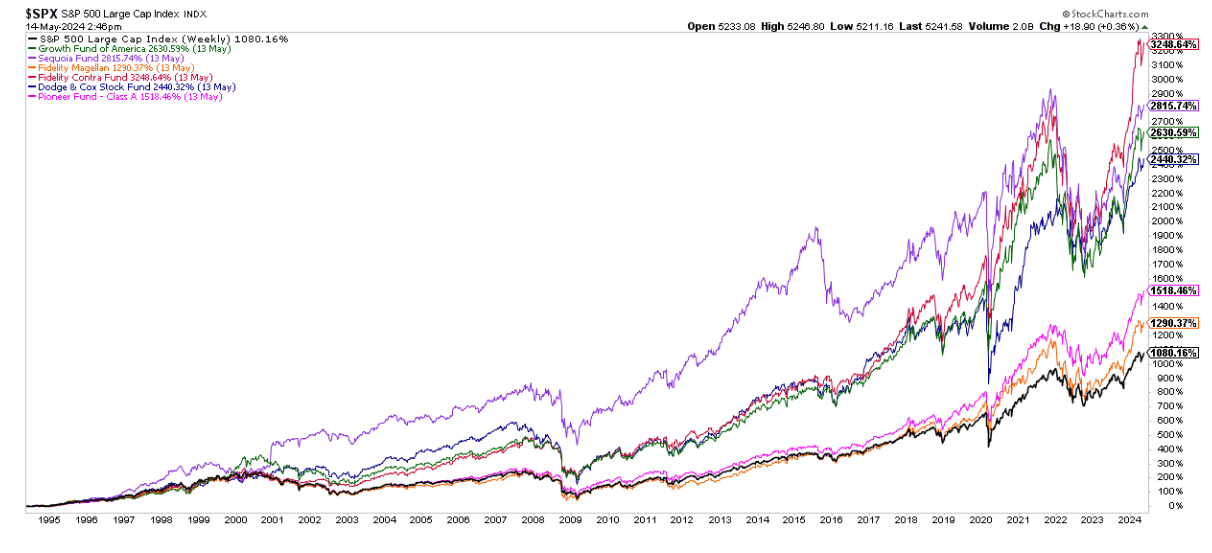

However, while a fund manager may NOT beat the index from one year to the next, it doesn’t mean that a sound investment strategy won’t outperform significantly, with lower risk, over the long term. Finding funds with long-term track records is difficult because many mutual funds didn’t launch until the late “go-go 90s” and early 2000s. However, I quickly looked up some of the largest mutual funds with long-term track records. The chart below compares Fidelity Magellan and Contrafund, Pioneer Fund, Sequoia Fund, Dodge & Cox Stock Fund, and Growth Fund of America to the S&P 500 Index.

I don’t know about you, but investing in quality, actively managed funds over the long term seems a better bet. Crucially, they did it without heavily concentrated positions in just a handful of stocks.

Financial Resource Corporation summed it up best;

“For those who are not satisfied with simply beating the average over any given period, consider this: if an investor can consistently achieve slightly better than average returns each year over a 10-15 year period, then cumulatively over the full period they are likely to do better than roughly 80% or more of their peers. They may never have discovered a fund that ranked #1 over a subsequent one or three-year period. That ‘failure,’ however, is more than offset by their having avoided options that dramatically underperformed.

For those that are looking to find a new method of discerning the top ten funds for the next year, this study will prove frustrating. There are no magic short-cut solutions, and we urge our readers to abandon the illusive and ultimately counterproductive search for them.

For those who are willing to restrain their short-term passions, embrace the virtue of being only slightly better than average, and wait for the benefits of this approach to compound into something much better.”

The Only Thing That Matters

There are many reasons why you shouldn’t chase an index over time and why you see statistics such as “80% of all funds underperform the S&P 500” in any given year. The impact of share buybacks, substitutions, lack of taxes, no trading costs, and replacement all contribute to the index’s outperformance over those investing real dollars who do not receive the same advantages.

More importantly, any portfolio allocated differently than the benchmark to provide for lower volatility, income, or long-term financial planning and capital preservation will also underperform the index. Therefore, comparing your portfolio to the S&P 500 is inherently “apples to oranges” and will always lead to disappointing outcomes.

“But it gets worse. Often times, these comparisons are made without even considering the right way to quantify ‘risk’. That is, we don’t even see measurements of risk-adjusted returns in these ‘performance’ reviews. Of course, that misses the whole point of implementing a strategy that is different than a long only index.

It’s fine to compare things to a benchmark. In fact, it’s helpful in a lot of cases. But we need to careful about how we go about doing it.” – Cullen Roche

For all these reasons and more, comparing your portfolio to a “benchmark index” will ultimately lead you to take on too much risk and make emotionally based investment decisions.

But here is the only question that matters in the active/passive debate:

“What’s more important – matching an index during a bull cycle, or protecting capital during a bear cycle?”

You can’t have both.

If you benchmark an index during the bull cycle, you will lose equally during the bear cycle. However, while an active manager focusing on “risk” may underperform during a bull market, preserving capital during a bear cycle will salvage your investment goals.

Investing is not a competition, and as history shows, treating it as such has horrid consequences. So, do yourself a favor and forget what the benchmark index does from one day to the next. Instead, match your portfolio to your personal goals, objectives, and time frames.

In the long run, you may not beat the index, but you are likely to achieve your personal investment goals, which is why you invested in the first place.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors.

He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Disclosure

Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with over $1 billion in assets under management. As a team of certified and experienced professionals, we seek to provide our clients with educational services and the necessary information and tools to educate you in the field of finance, investing and economics. To this end, you can use the Real Investment Advice Platform to avail yourself of various video, audio and proprietary collections of information at your leisure to learn and gather the necessary information that you may need in the fields of investment news, investment opinion, financial news, financial opinion, economic news and economic opinion, finance, investing and economics. Utilizing the functionality and tools provided by Real Investment Advice, you can access this information in a variety of ways, including via video and audio programming, audio and visual media content streaming services, downloadable audio-visual media, uploaded, posted or tagged third-party videos, receiving or viewing audio and video clips, blogs, podcasts, and YouTube videos, all of which are accessible on the Real Investment Advice media platform and/or various Internet and communications links that are accessible via the Real Investment Advice Platform and allow for the broadcasting, transmission and streaming of the information and audio-visual content to your media devices and other communications platforms for your viewing and listening pleasure. All of these tools and sources of information are made available to you so that you can utilize the same to make the right financial, economic and investment decisions.

RIA Advisors offers multiple custodial arrangements, either directly of through wholly owned subsidiaries, with Fidelity and Interactive Brokers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All