QT-Lite: Quantitative Tightening's Limited Impact

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsQuick read:

- The Federal Reserve’s balance sheet is one of the world’s most important security portfolios. Yet, its ongoing importance for markets and financial conditions is often underappreciated.

- Over the last 15 years, both the size and duration profile of the Fed’s balance sheet have expanded meaningfully. As a share of GDP, the Fed’s securities portfolio is 7x as large in notional terms and 9x as large in terms of duration equivalents compared to the beginning of 2009.

- The composition of the asset side of the Fed’s balance sheet offsets some of the intended tightening effects of higher policy rates. Research by the Federal Reserve and our own analysis suggest that current Fed holdings of long-dated Treasuries and mortgages exert a powerful downward force on bond yields – equivalent to a policy rate easing of about 2%.

- Going forward, we think there is an underappreciated likelihood that the Fed could be more active with regards to shifting the composition of its balance sheet towards shorter duration securities if further policy tightening is needed. This transition would pose downside risks for long-dated US government bond prices and the US dollar.

First, I would like to see the Fed's agency MBS holdings go to zero…Second, I would like to see a shift in Treasury holdings toward a larger share of shorter-dated Treasury securities…This is an issue the FOMC will need to decide in the next couple of years.

Federal Reserve Governor Christopher Waller, March 1, 2024

The Federal Reserve’s balance sheet is one of the world’s most important security portfolios. So it was surprising that market commentary treated the recently-announced decision to slow the pace of asset runoff as barely a sidenote compared to the focus and analysis that accompanied the numerous rounds of quantitative easing (QE) during balance sheet expansion. The decision to reinvest a larger share of maturing bonds despite a surprisingly strong economy also highlights an institutional asymmetry in the Fed’s management of the balance sheet – QE rounds have been deployed, resized, and framed as policy actions subject to evolutions in the real economy whereas quantitative tightening (QT) modifications have been managed as either a set-and-forget pace or subject to liabilities-driven technical adjustments. This asymmetry has cumulated over fifteen years to result in a massively impactful balance sheet – as a share of GDP the Fed’s securities portfolio is 7x as large in notional terms and 9x as large in terms of duration equivalents compared to the beginning of 2009.

A recent speech by Fed Governor Waller, quoted above, indicates that there are voices on the committee now advocating for a substantial reassessment of the balance sheet. Materially shifting the composition and maturity of holdings would likely necessitate active asset sales; a form of policy tightening thus far only undertaken by foreign central banks. If the economy continues to expand strongly and inflation remains sticky, we see a growing chance that future tightening discussions could involve altering the composition of balance sheet holdings. Though financial markets have largely ignored the possibility of a more active approach to shrinking or recasting the balance sheet, we view this as an underappreciated risk, particularly after the US election. Transitioning to a shorter duration balance sheet would likely drive up long-dated government bond yields and be negative for the US$, two sets of exposures that we hold in the Tactical Opportunities Fund.

It's not the size that matters

The composition of the balance sheet, specifically the duration of the asset holdings, is what matters for financial conditions and the economy.1 The link between shifts in balance sheet duration and the real economy was described succinctly in the announcement of Operation Twist in 2011. “To support a stronger economic recovery and to help ensure that inflation, over time, is at levels consistent with the dual mandate, the Committee decided today to extend the average maturity of its holdings of securities... This program should put downward pressure on longer-term interest rates and help make broader financial conditions more accommodative.” Although recent shifts in balance sheet policy have focused on the notional pace of asset purchases or sales, the more important variable for financial markets remains shifts in duration.

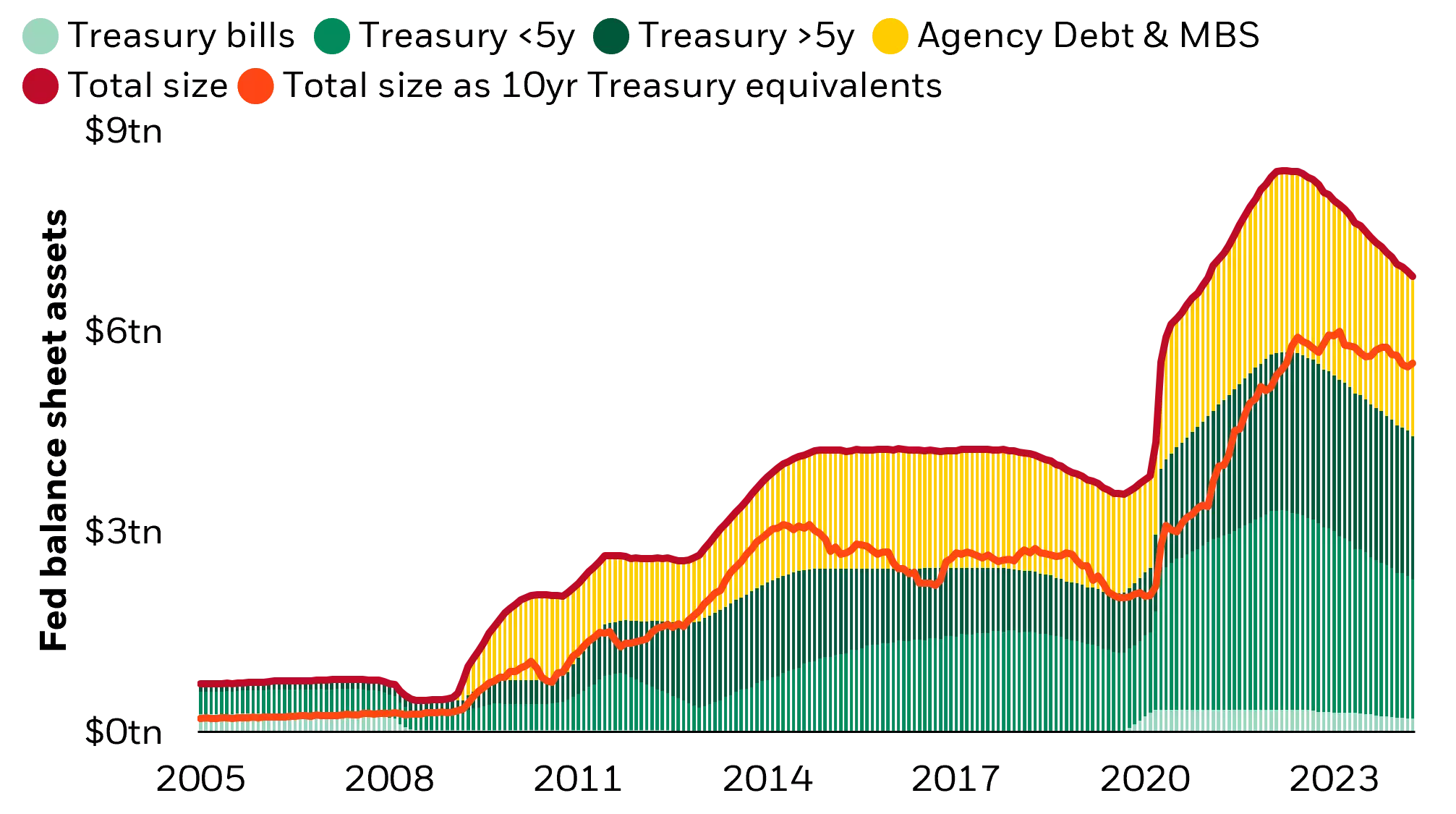

Both the size and duration profile of the Fed’s balance sheet have expanded over the last 15 years

Source: BlackRock with data from Federal Reserve, March 2024

The visual above shows the evolution of the balance sheet size broken down by maturity bucket and type – Treasuries and Agency mortgage backed securities (MBS). We also overlay an estimate of the 10-year duration equivalents of those aggregate holdings. A few noteworthy observations stand out to us:

- All of the growth in the size of the balance sheet since the financial crisis has been in longer-dated bonds that have materially lengthened the duration of the balance sheet.

- Agency MBS comprise nearly a one third share of the long-dated bond holdings and their duration contribution to the balance sheet has tripled over the past four years, helping to offset the asset sales during QT.2

- The duration-adjusted size of the balance sheet has often fluctuated independently of the notional size in numerous periods and has only declined by just under 10% during the most recent round of QT after rising over 200% during the latest round of QE.

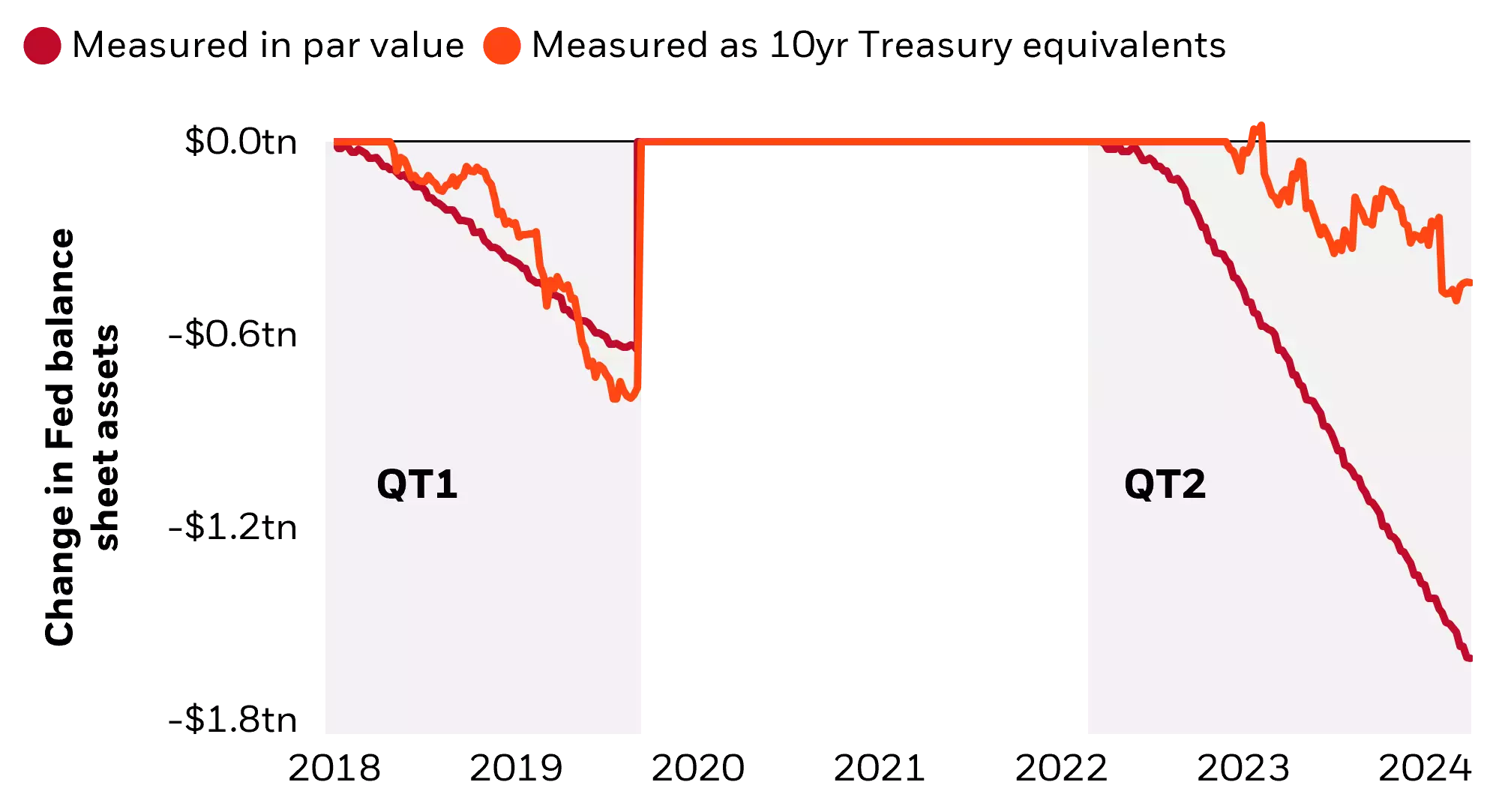

“Like watching paint dry”

Part of the market’s relative disinterest in the Fed’s balance sheet innovations during the two rounds of QT is by design. Describing the principles for the first quantitative tightening (QT) in 2017, former Fed Chair Yellen described the design of runoff to be “like watching paint dry, … something that runs quietly in the background.”3 The Fed has undertaken this most recent QT with the same passive and notionally-focused approach, but with a much more aggressive monthly pace of runoff compared to QE1.4 However, QT2 has removed less duration from a much larger balance sheet and therefore delivered materially less financial markets tightening than was intended.

The most recent quantitative tightening has had a more limited impact on the duration profile of the Federal Reserve balance sheet

Source: BlackRock with data from Federal Reserve, March 2024.

The visual above compares the balance sheet impacts of both QT episodes in terms of notional asset holdings as well as the associated duration impact. Since the Fed is only running down its holdings of maturing securities, it is only reducing holdings of assets that are, by definition, associated with very low duration risk. Whereas QE purchases were focused on the long-end of the yield curve, QT runoff has been implemented at the short-end of the yield curve. That asymmetry has translated into successively larger holdings of high duration assets during each round of QE that have barely been released back into the market during QT. The continued maintenance of a long-dated balance sheet continues to hold down the yields of long-dated bonds.

Hidden rate cuts

A couple of facts help to explain the mechanics for how this size and the asset mix on the Fed’s balance sheet continues to suppress long-term bond yields5:

- The Federal Reserve portfolio still holds over 30% of all of the aggregate outstanding 10+ year Treasuries, thereby removing a significant amount of the supply of long-dated government securities and creating scarcity.

- The Federal Reserve continues to reinvest assets in excess of the monthly runoff caps. In 2023 those purchases totaled $860 billion, meaning that the Fed purchased nearly 10% of the new supply of 10 & 30yr bonds at Treasury auctions last year.

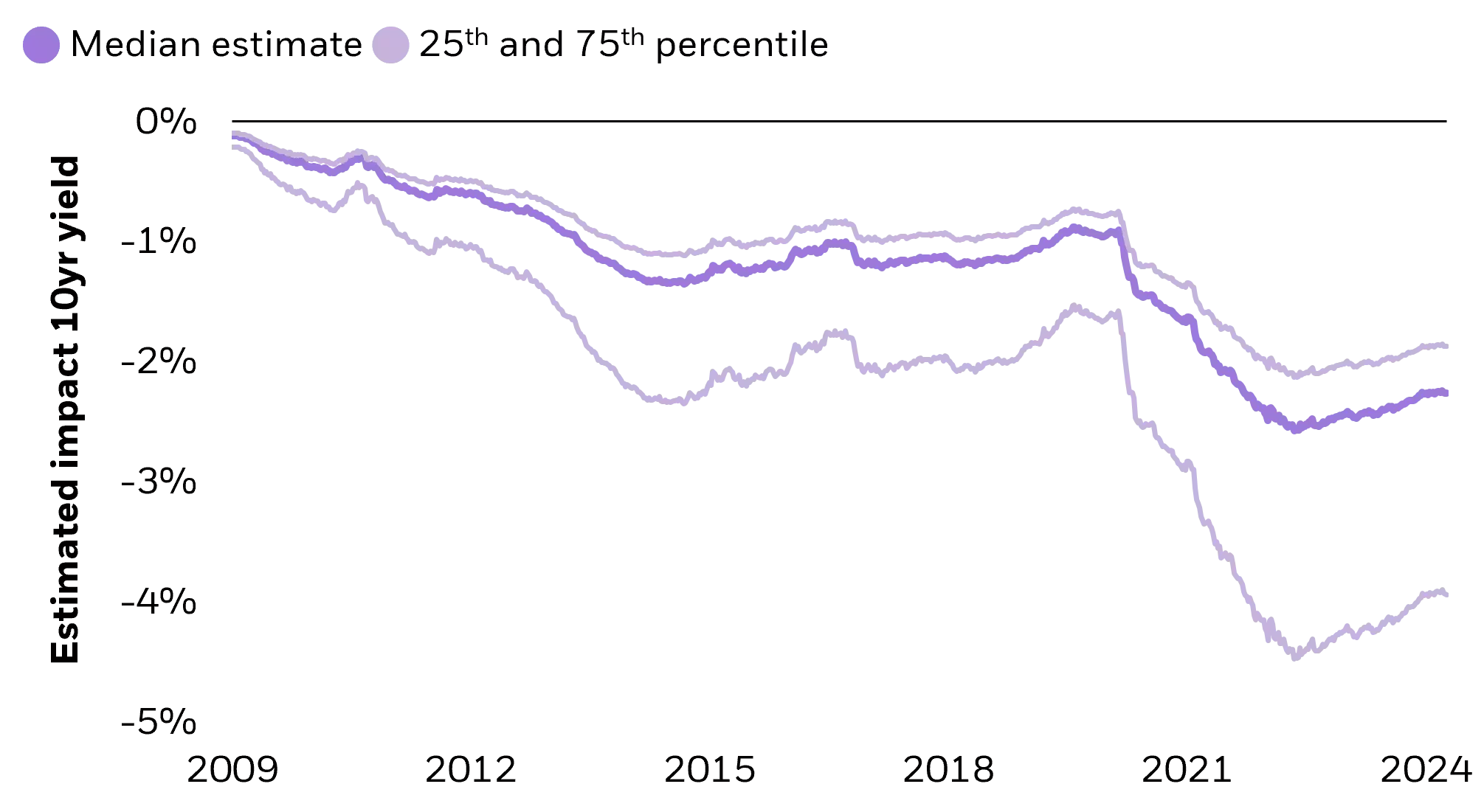

To estimate the net easing effects of the Fed’s current balance sheet and ongoing reinvestment purchases, we replicate the approach used in a 2022 Kansas City Fed research paper.6 That method multiplies the Fed’s duration-adjusted balance sheet size by a range of estimates from the macroeconomic literature of the yield impact of the Fed’s holdings. That allows us to estimate a range of potential easing effects along with a median estimate. Those results, shown in the graphic below, are historically consistent with the Kansas City Fed researchers’ findings but extend through to the first quarter of 2024.

The Federal Reserve’s portfolio holdings exert a powerful downward force on 10-year US Treasury yields

Source: BlackRock with data from Federal Reserve, March 2024.

The results highlight the degree to which the balance sheet continues to exert a powerful downward force on US bond yields. The composition of the balance sheet today is likely suppressing 10-year yields by over 2% and potentially by as much as 4%. The current easing effects of the balance sheet are also in excess of any of the estimated magnitudes in the decade prior to the pandemic. This helps to explain the resilience of the economy to the policy tightening of 2022 and 2023 as well as continued inversion of the US yield curve. The recent dynamics also suggest that the Fed’s current QT has barely begun to remove the outsized accommodation delivered by the latest round of QE – the range of estimated tightening are between 0.25-0.50%, following a delivered balance sheet easing of between 1.4-2.9% in 2020 and 2021

Conclusion

The Fed’s balance sheet remains a powerful and under-appreciated policy tool that continues to apply significant downward pressure on long-dated bond yields. The current size and composition help to explain both the apparent absence of term premium in the U.S. yield curve and why monetary policy is less restrictive than would be suggested by the current level of federal funds rate. Fed Governor Chris Waller’s preferred balance sheet would likely shift reinvestments of maturing securities into short-dated bills but could also require active asset sales – a policy choice that is currently being undertaken by a number of foreign central banks but would be a major policy shift for the Federal Reserve.

In portfolios, we are positioned for the degree of restrictiveness of US monetary policy to continue to be called into question with resilient economic growth and inflation stubbornly above target. Our analysis of fiscal-monetary entanglement and the Fed’s balance sheet as described in this article make us think that future monetary tightening discussions could potentially consider balance sheet adjustments. Though the likelihood of any policy changes happening this year are exceedingly low, we think the risks for a tightening from balance sheet changes could grow once we get through the US elections in November.

Source:

1 Brian Sack, who implemented the initial rounds of asset purchases on the NY Fed markets desk describes it as follows: “My view is that QE does have effects and it does have effects on financial conditions and lower long term interest rates…I see those effects as associated with the overall size of the balance sheet rather than the monthly flow and I think that’s conventional wisdom within inside the Federal Reserve System as well… This is really getting into the details, but I think of it as 10yr equivalents, which is a way of adjusting for the duration.”

2 Higher mortgage rates have deterred mortgage borrowers from refinancing existing loans, reducing mortgage prepayment and shifting anticipated cashflows of MBS into the future, in effect lengthening the duration of the security. To illustrate, the duration of the benchmark Bloomberg index of U.S. MBS was less than 2 years at the beginning of the COVID pandemic when rates were at their trough but has since increased to more than 6 years.

3 That approach has used notional caps for the monthly pace of runoff with a passive reinvestments of additional maturing securities.

4 The initial pre-set pace of Treasury runoff for QT2 was $60bn a month, which was more than double the pace of QT1. Agency MBS runoff set at $35bn per month, but has rarely approached that cap (the current pace is ~$17bn per month) because low levels of mortgage prepayment activity have meant that MBS securities have been redeemed very slowly. Starting in June the cap for US Treasury runoff will be reduced to $25bn per month, which will result in meaningfully larger reinvestment purchases at future Treasury auctions.

5 NY Fed’s 2023 Open Market Operation Report

6 The Evolving Role of the Fed's Balance Sheet: Effects and Challenges

Performance data quoted represents past performance and is no guarantee of future results. Investment returns and principal values may fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. All returns assume reinvestment of dividends and capital gains. Current performance may be lower or higher than that shown. Refer to blackrock.com for most recent month-end performance.

To obtain more information on the fund, including the Morningstar time period ratings and standardized average annual total returns as of the most recent calendar quarter and current month-end, please visit Tactical Opportunities Fund.

The Morningstar RatingTM for funds, or "star rating," is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period actually has the greatest impact because it is included in all three rating periods.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Live Virtual Event: Join Now

Upcoming Virtual Events View All