The Costco Economy

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey Takeaways

- Both Costco and Ross Stores are experiencing increased foot traffic and higher sales of previously less popular products, indicating a strong and resilient U.S. consumer.

- The shift in consumer behavior toward buying more discretionary items is attributed to the deceleration of inflation, according to Costco management.

- Constellation Brands, including its Modelo beer brand, is also not seeing any issues with the U.S. consumer and is investing in capacity to meet the demand.

Earnings season never really ends. It is a slow, steady drip of useful—sometimes conflicting—data. But listening closely can be powerful for uncovering both positive and negative trends. For example, American Airlines signaling a weaker-than-expected summer should be taken with a grain of Boeing. Norwegian Cruise Lines is not seeing a problem with its travelers. Not every headline should be taken as a sign. It takes a bit of digging.

When it comes to top-notch operators, Costco is up there with the best of them. The company has a rather wide view of the consumer. From food to furniture, Costco sells it. What did it have to say about the health of the consumer?

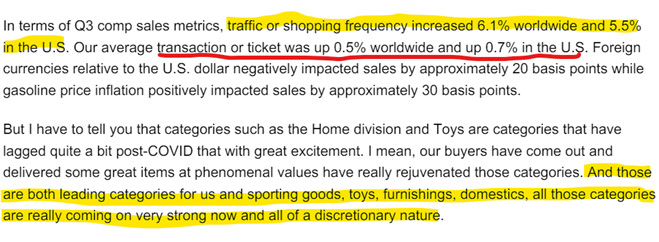

Source: Costco.

For Costco, there is little to no worry about the health of the consumer. The retailer’s envied foot traffic? Strong. The categories that have been weak in the post-pandemic period? Those were the leading categories for Costco. That does not align with the narrative of a slowing, struggling consumer. And it should not be readily dismissed, either.

Partly, the shift in consumer behavior—according to Costco management—is due to the deceleration of inflation. With less inflation pressure came a shift in consumer behavior back toward buying more of other categories. While specific to the experience of Costco, the data points should not be dismissed. Not only is the U.S. consumer alive and well, it is buying the more discretionary stuff.

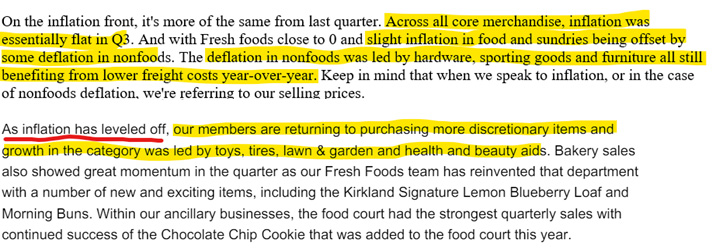

Source: Costco.

But surely this is a Costco-specific phenomenon? No, it is not.

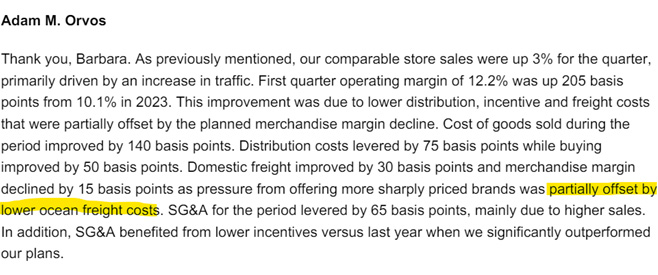

Source: Ross Stores.

Ross Stores called out better foot traffic as well. And it sold more “sharply priced” products—that is code for “expensive.” The consumer is shopping more (foot traffic) and buying stuff that was shunned for the past several quarters. That is a meaningful pushback to the narrative of a potentially problematic U.S. consumer.

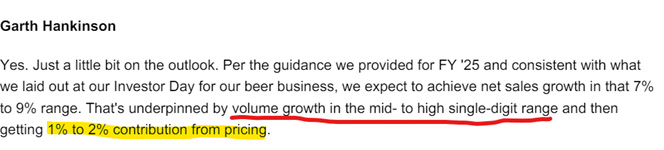

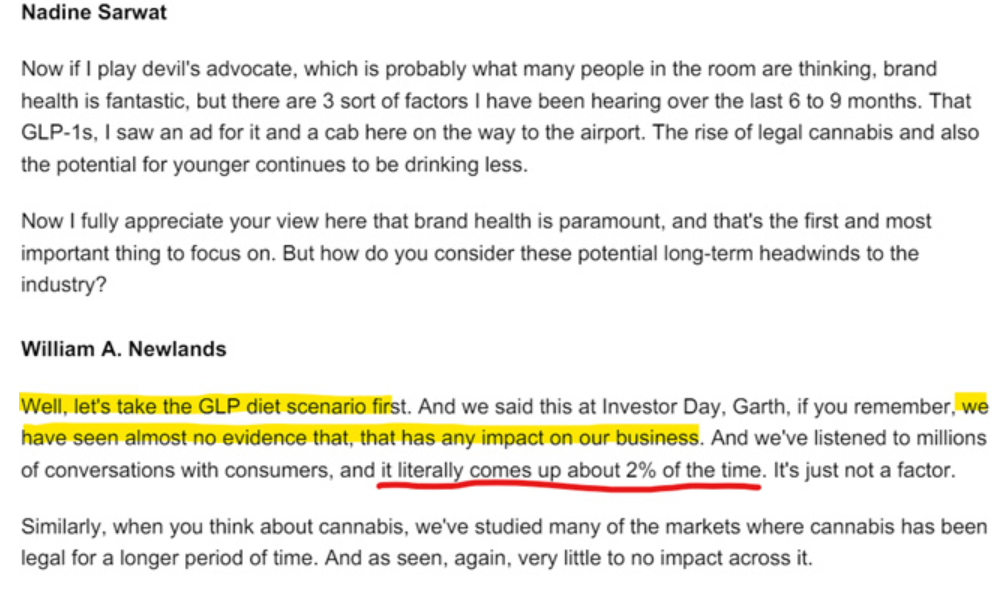

Then, there is commentary from Constellation Brands. Its Modelo beer brand is the #1 brand in the U.S., and the commentary around the outlook was similar to Costco’s. The consumer? No issues there.

There are certainly headwinds, though. The rise of GLP-1s could be an issue for beer consumption. After the meteoric success of weight loss drugs, many of the staples companies were viewed as at risk. But that might be overplayed for the beer category.

Source: Constellation Brands.

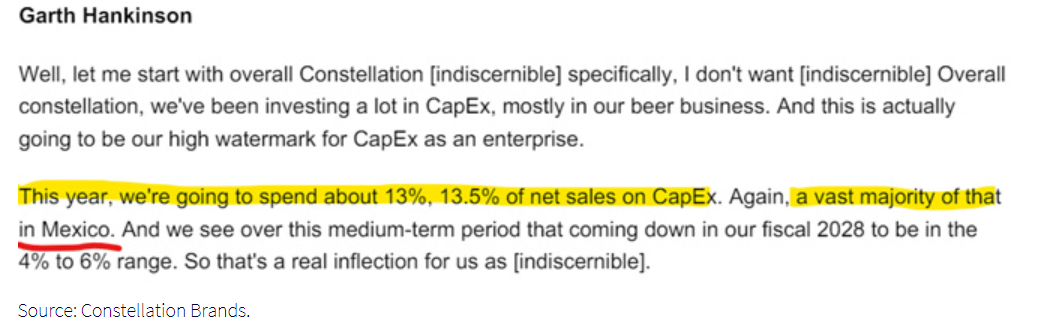

In fact, Modelo and Constellation’s broader beer business has been so successful that it is playing catch-up with its capital expenditures. Where is that capital being invested? Mexico. Again, that is more signal than noise. And it is being done in size.

Why does any of this matter? Because it is the reality of the economy, not a sentiment about the direction. Costco is seeing prices “level off” and the consumer begin to shift spending habits. Both Costco and Ross Stores are seeing foot traffic increase. Constellation is not seeing a consumer slowdown and is investing in capacity to keep up with the demand. None of that is a “maybe.” All of that is the reality of the U.S. consumer. Yes, the consumer sentiment numbers have been horrid. But what the surveys say and what the consumer is doing are two wildly different things.

Welcome to the Costco Economy.

U.S. investors only: Click here to obtain a WisdomTree ETF prospectus which contains investment objectives, risks, charges, expenses, and other information; read and consider carefully before investing.

There are risks involved with investing, including possible loss of principal. Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, currency, fixed income and alternative investments include additional risks. Please see prospectus for discussion of risks.

Past performance is not indicative of future results. This material contains the opinions of the author, which are subject to change, and should not to be considered or interpreted as a recommendation to participate in any particular trading strategy, or deemed to be an offer or sale of any investment product and it should not be relied on as such. There is no guarantee that any strategies discussed will work under all market conditions. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This material should not be relied upon as research or investment advice regarding any security in particular. The user of this information assumes the entire risk of any use made of the information provided herein. Neither WisdomTree nor its affiliates, nor Foreside Fund Services, LLC, or its affiliates provide tax or legal advice. Investors seeking tax or legal advice should consult their tax or legal advisor. Unless expressly stated otherwise the opinions, interpretations or findings expressed herein do not necessarily represent the views of WisdomTree or any of its affiliates.

The MSCI information may only be used for your internal use, may not be reproduced or re-disseminated in any form and may not be used as a basis for or component of any financial instruments or products or indexes. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each entity involved in compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties. With respect to this information, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including loss profits) or any other damages (www.msci.com)

Jonathan Steinberg, Jeremy Schwartz, Rick Harper, Christopher Gannatti, Bradley Krom, Kevin Flanagan, Brendan Loftus, Joseph Tenaglia, Jeff Weniger, Matt Wagner, Alejandro Saltiel, Ryan Krystopowicz, Brian Manby, and Scott Welch are registered representatives of Foreside Fund Services, LLC.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

You cannot invest directly in an index.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All