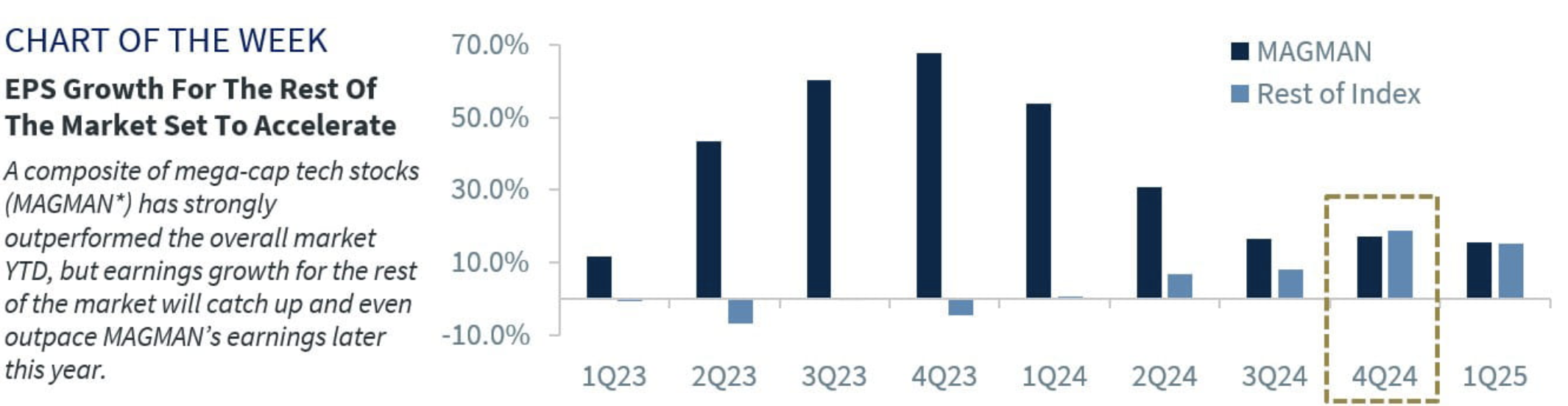

Key Takeaways

- The Fed will cut rates twice to support growth

- Interest rates are poised to tip lower

- The equity market should keep climbing longer term

Let’s go Team USA! The opening ceremonies for the Paris Summer Olympics are less than a month away (July 26). For the first time since the pandemic, fans will cheer for their favorite sports events in person. But that’s not all, there are other firsts – an opening ceremony held outside a stadium, an unusual mascot and medals infused with a piece of the Eiffel tower. So we borrow from the Summer Olympics for our quarterly theme. But rather than using some of the most popular sporting events (swimming and gymnastics) to convey our views, we use the lesser-followed sports, such as surfing, beach volleyball and breakdancing. Yes, breakdancing makes its debut at these Olympics! For more insights on our quarterly outlook, join our Quarterly Coordinates webinar on Monday, July 8 at 4 p.m. In the meantime, here’s a sneak peek:

- Economy has been ‘riding a wave’ of strength | Despite the most aggressive tightening cycle in four decades, the economy has been riding the wave of consumer strength since the post-COVID recovery. But with the consumer showing signs of fatigue (e.g. rising delinquencies, slower discretionary spending, fewer splurges), the labor market starting to slow and inflation taking its toll (particularly for lower-income consumers), the Fed needs to start dialing back some of its policy restraint to keep the recovery going. The Fed’s trick will be to cut interest rates in time to avoid an economic wipeout (aka recession) without further stoking inflation pressures. We think there is an opening to keep the surf up with two rate cuts by year end and some additional easing in 2025. This should keep GDP growth near trend at 2.1% in 2024 and 2.0% in 2025.

- Interest rates are poised to ‘tip’ lower | The bond market is guided by two key dynamics – growth and inflation. But just as beach volleyball brings new challenges for the players (sand, sun and unpredictable weather), the bond market is facing its own set of challenges – record government debt issuance, the Fed’s balance sheet and demand unease. With inflation and the economy set to cool for the remainder of the year, interest rates should tip lower. In fact, we expect the 10-year Treasury yield to fall to 4.0% by year-end and 3.75% over the next twelve months. Cash remains an attractive alternative with yields still hovering above 5.0%, but that is unlikely to last. Therefore, slowly locking in duration ahead of the Fed’s easing cycle appears prudent. Areas to consider: intermediate Treasury’s, high-quality corporates and longer-maturity municipals.