Active Exchange-Traded Funds (ETFs) represent a significant evolution in the investment landscape, offering the best of both active management and the structural advantages of ETFs. With transparency, liquidity, lower cost, tax efficiency, and access to professional expertise, active ETFs can provide investors with a versatile tool to achieve their investment objectives.

It is crucial, however, to take a closer look. At one end of the spectrum, passive ETFs are designed to track a specific index aiming to replicate its performance by holding the same or a representative sample of the index's components. At the other end of the spectrum, pure, active ETFs engage managers to make specific investment decisions with the goal of outperforming a benchmark.

In between, there are a multitude of ETF products that incorporate elements of both passive and active strategies. That can lead to confusion among investors regarding their true nature. In our experience, these hybrid investment vehicles are often mistaken for truly active ETFs due to their active components but they fundamentally differ in their approaches.

A deeper look

ETFs can be labelled as active even if they make just slight modifications to the standard index-tracking approach. Quant-based active ETFs, for example, use sophisticated mathematical models and algorithms to select securities based on quantitative analysis. Although they employ advanced data-driven strategies, quant-based ETFs are typically more systematic and rules-based and don’t rely on discretionary decisions made by portfolio managers. This systematic approach can blur the lines between active and passive management but it does not equate to the traditional active management we would expect to come with an “active” label.

Another example of hybrid or “quasi-active” ETFs are so-called Smart Beta ETFs. They aim to slightly outperform a benchmark index by making minor, strategic deviations from the index. These ETFs use quantitative methods or fundamental analysis to identify opportunities for incremental gains while maintaining a portfolio that closely resembles the index. Enhanced indexing incorporates elements of both passive and active management but it lacks the full discretionary approach of active ETFs.

These types of “quasi-active” ETFs can offer benefits for investors but challenges can occur if there are misunderstandings on the investors’ part over the scope and capability of these vehicles. For example, some investors may take the view that actively managed ETFs can mitigate risks more effectively than passive ETFs. However, if a “quasi-active” ETF is perceived as being a pure active ETF, some investors could have a misconceived higher expectation of its risk management capability.

The highs and lows

In our view, there is a world of difference between an active ETF that seeks to outperform benchmark indices through the skill of its manager using strategic stock selection, versus one that implements only minor changes, for example, based on enhanced indexing or quantitative methods.

Not only may investors miss out on the potential benefits of true active management, such as tactical asset allocation and stock picking, which could enhance returns in certain market conditions. But by believing their ETFs are actively managed, they might not seek other opportunities that offer genuine active management. They may also believe that their investment is being actively managed to outperform the market, which is not the case. This misunderstanding can lead to misinformed investment decisions and mismatched expectations regarding performance and risk.

“Quasi-active” ETFs may not always incorporate real-time adjustments to market conditions. If labelled as active, investors might expect these adjustments, leading to disappointment when the ETF does not respond to market volatility or take advantage of short-term opportunities.

Some investors argue that “quasi-active” ETFs that are slightly adjusted or optimized can potentially deliver better risk-adjusted returns. These vehicles can, for example. incorporate minimal active elements such as small factor tilts for value or momentum, which can enhance returns without significantly deviating from the ETF’s passive nature.

The biggest potential advantage of “quasi-active” ETFs lies in their cost efficiency. They generally have lower expense ratios compared with truly actively ETFS because they do not require intensive research, frequent trading, or management oversight. But while investors might perceive these ETFs as actively managed it pays to take a look under the hood. Are they are getting access to strategic, expertise-driven management?

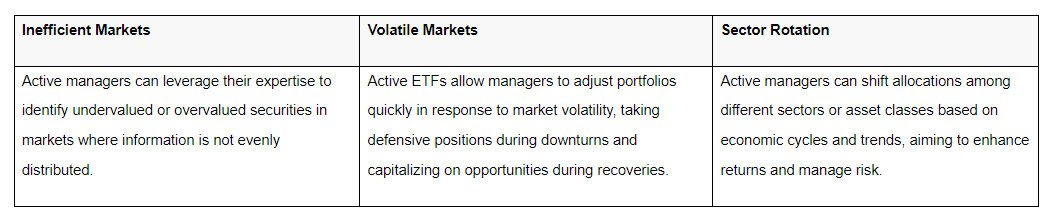

What it means to be active

Unlike traditional passive or “quasi-active” ETFs, which typically aim to replicate the performance of a specific index, truly active ETFs provide flexibility, transparency, and potential for higher returns through the expertise of professional portfolio managers. Skilled managers can exploit market inefficiencies, conduct thorough research, and make tactical adjustments in response to market conditions. This performance potential is particularly compelling in certain environments:

Truly active ETFs are generally managed by experienced portfolio managers who actively select and manage securities to outperform their benchmarks. This active oversight leverages deep market insights and research to identify investment opportunities and manage risks effectively.

While active ETFs typically have higher expense ratios than passive or “quasi-active” ETFs, they often have lower costs compared to traditional actively managed mutual funds. The ETF structure reduces operational and administrative expenses, enhancing net returns for investors. The in-kind creation and redemption process of ETFs minimizes capital gains distributions, making them more tax-efficient compared with mutual funds.

The ETF structure also allows for the creation of specialized and innovative investment strategies. Active ETFs can focus on specific sectors, themes, or investment styles, providing targeted exposure to niche areas of the market that may not be available in traditional mutual funds. With the potential to achieve significant returns by identifying and investing early in high-growth sectors like biotechnology and artificial intelligence (AI), skilled managers can exploit market inefficiencies, conduct research, and make tactical adjustments in response to market conditions.

Understanding the differences

In conclusion, taking a closer look at the full spectrum of active ETFs is key for investors. While many ETFs incorporate active elements, their management philosophies can differ significantly. Active ETFs rely on the expertise and judgment of portfolio managers to select investments, aiming to outperform benchmarks through strategic decisions. In contrast, quant and enhanced indexing ETFs use systematic, rule-based approaches to achieve their objectives, often blending passive indexing with active elements to enhance returns or manage risks.

Understanding these differences empowers investors to make informed decisions, ensuring they select investment strategies that align with their specific goals and risk tolerance. For those seeking the potential for higher returns who are comfortable with the associated risks, truly active ETFs may be suitable. Conversely, investors looking for a more systematic approach with lower fees and less active risk might prefer quant or enhanced indexing ETFs.

By recognizing the unique characteristics and philosophies along the ETF spectrum, investors can better navigate the ETF landscape and construct portfolios that effectively meet their financial objectives.

At Matthews, we believe in the power of active management. Our range of active ETFs benefit from the firm’s 30+ years of active investment experience in Asia and Emerging Markets. Our ETFs use the same fundamental research and macro-aware process to create unique portfolios that aim to generate above-index returns by investing in companies not typically found in most broad international strategies.

Learn more about investing in Matthews Active ETFs at matthewsasia.com/ETFs.

Michael Barrer

VP, Head of ETF Capital Markets

IMPORTANT INFORMATION

The views and information discussed in this report are as of the date of publication, are subject to change and may not reflect current views. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. Investment involves risk. Investing in international and emerging markets may involve additional risks, such as social and political instability, market illiquidity, exchange-rate fluctuations, a high level of volatility and limited regulation. Investing in small- and mid-size companies is more risky and volatile than investing in large companies as they may be more volatile and less liquid than larger companies. Past performance is no guarantee of future results. The information contained herein has been derived from sources believed to be reliable and accurate at the time of compilation, but no representation or warranty (express or implied) is made as to the accuracy or completeness of any of this information. Matthews Asia and its affiliates do not accept any liability for losses either direct or consequential caused by the use of this information.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Matthews Asia

Read more commentaries by Matthews Asia