The second half of 2024 will likely be heavily dominated by the election, inflation, and interest rates in the U.S. These narratives create challenges, as well as opportunities for investors in the latter half of the year. Morgan Stanley recently discussed the outsized impact of fiscal policy as well as the U.S. dollar looking ahead on their blog, The BEAT.

Fiscal Policy Takes Root

Morgan Stanley cautions that the dominance of fiscal policy is likely to grow in the next six to 18 months. The U.S. election this fall will likely showcase fiscal policy as it pertains to government spending and taxes. The impact on markets and narratives in the second half cannot be understated.

Moving beyond the election, increased government spending and debt play a growing, influential role on the economy, and potentially inflation. Add in the likelihood of tariffs as a means to resolve geopolitical conflicts and “fiscal policy may then dominate monetary policy, which has the effect of increasing market uncertainties and risk premia,” according to the authors. They caution that this is the likely outcome regardless of which candidate wins the presidential election.

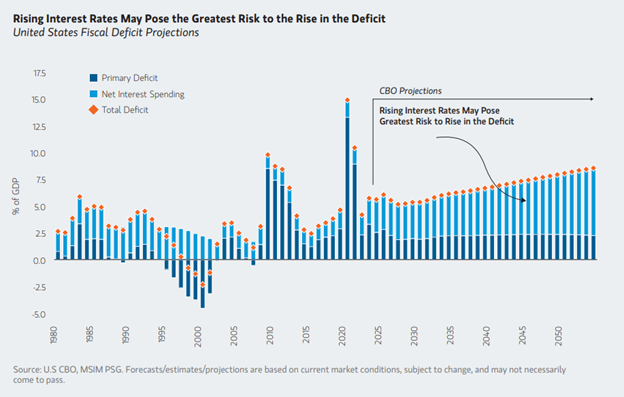

The potential of spiraling U.S. deficits on interest payments also looms large. The primary U.S. government deficit (revenues minus spending) is forecast to remain stable at approximately 2%.

However, “the interest payments on the debt are ultimately the culprit that drives the total deficit higher,” the authors explained. This leads to a “vicious cycle that creates economic instability.”

It also creates heightened risk for foreign investors in U.S. Treasuries. A real return of 1.8% (real GDP growth) may not account for the added risk investors take on. Asset price discounting may be a necessary lever that is pulled to accommodate the added risk. The authors note that it creates tension.

The U.S. Dollar

Concerns around burgeoning U.S. deficits, spending, debts, and more create potential challenges for U.S. dollar valuations. That alongside the “weaponization of the dollar” in the wake of Russia’s invasion of Ukraine resulted in an increasing number of central banks globally looking to alternatives to the U.S. dollar.

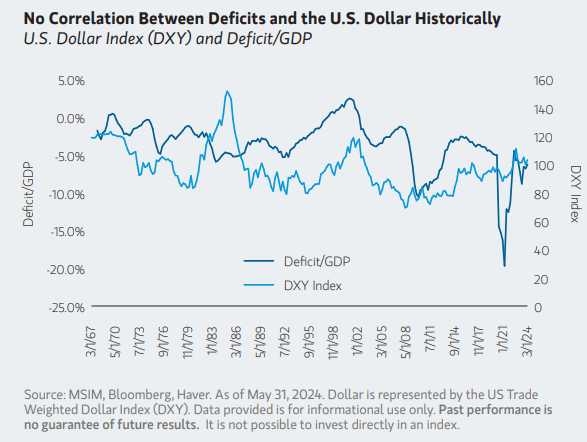

Morgan Stanley research did not reveal notable correlations between lingering deficits and currency weakness over the course of the last 50 years. They attribute this largely to the “monetary sovereignty, strong institutions and control over its own currency” that the U.S. has.

While central banks may be shifting away from the dollar, they still remain invested in the U.S. China reduced the amount of U.S. Treasuries it owned while simultaneously buying more into U.S. mortgage-backed securities as well as agency bonds.

Despite efforts by China to increase the use of the yuan in international dealings with countries in its region, it currently accounts for just 2% of payments made globally. “The dollar continues to dominate due to a lack of viable alternatives,” Morgan Stanley wrote.

Dollar valuations in recent years is driven primarily by differing growth rates between the U.S. and other countries as well as relative interest rate. The Fed’s aggressive response to inflation beginning in 2022 resulted in a strong dollar compared to other currencies. That alongside continued, outperforming U.S. economic growth contributed to dollar strength.

That growth appears to be slowing, however, as other economies globally begin to recover. It creates a compelling case for international currencies looking ahead, particularly because the U.S. dollar is well outside of trend currently.

“The current dollar appreciation cycle is the longest on record,” the authors noted. Most dollar strength and weakness cycles last approximately seven years. The run-up to September 2022 resulted in 14 years of dollar appreciation, with the dollar holding at heightened levels ever since. Changing interest rate narratives and growth rates create a strong case for non-U.S. currencies in the months to come.

For more news, information, and analysis visit The ETF Yield Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by VettaFi