Western Influence

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits- The sun may well rise in the east, but it is the west that is vital for the economic sunshine in eastern economies. Western demand and monetary policy are having an important impact on economic prospects for the Asia-Pacific (APAC) region.

- APAC economies have witnessed improved exports, partly led by the chip cycle upturn, but are struggling with weak domestic demand. Disinflation has been uneven across the region. Most regional central banks continue to stand pat, awaiting further progress on disinflation and movements from the U.S. Federal Reserve.

- Asian exports could remain resilient for a while longer, but they face a challenging backdrop amid rising trade tensions and policy uncertainty. Renewed geopolitical frictions will likely be a significant headwind for a region that has benefitted immensely from trade openness.

- Following are our views on how major regional markets are poised to perform during the balance of 2024.

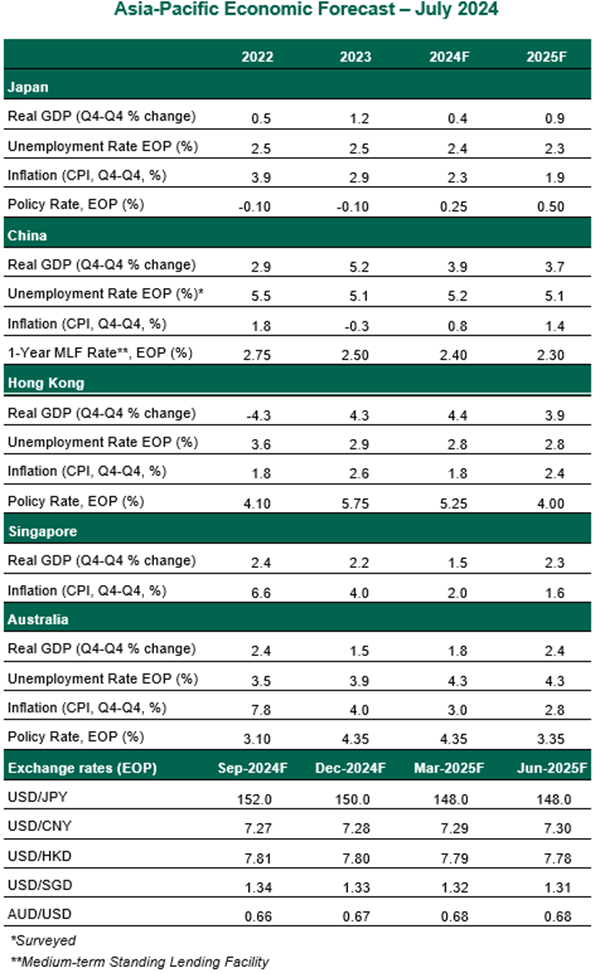

Japan

- First quarter real gross domestic product (GDP) growth contracted at a 2.9% annualized rate, led by a large decline in public fixed investment. While this result is disappointing, the weakness is unlikely to persist. Strong wage gains will help the economy bounce back in the coming months. Gains in exports will be gradual, as softer external demand will partially offset the boom in microchip exports. We have lowered our 2024 growth estimate, mainly to reflect the weak start to this year.

- The Bank of Japan (BoJ) maintained its policy rate at the June meeting, but announced its decision to start reducing its holdings of Japanese government bonds by a substantial scale in August. This month’s BOJ meeting will be closely watched for further signals on the pace of policy normalization on the back of recent weakness in the yen. While another hike at this month’s meeting cannot be ruled out completely, we expect the BoJ to wait until September to confirm the impact of the strong wage settlement on consumption and prices.

China

- In line with our expectations, the Chinese economy’s recent outperformance proved to be transient. Real GDP growth slowed six-tenths to 4.7% year over year in the second quarter. Strong manufacturing and exports continued to boost growth, but weak domestic demand remains an obstacle. The outlook for China remains cloudy. Stagnating household spending, low consumer confidence, and the ongoing property slump will prevent a clear turnaround anytime soon. Exports, a bright spot, also face downside risks from rising trade barriers and tariffs.

- Amid weakening economic momentum and persistent deflationary pressures, the People’s Bank of China cut its major short-term and long-term policy rates by 10 basis points in July. This small increment is unlikely to have much of an effect in a deleveraging economy. The decision to lower rates came just days after the release of the communiqué for the Third Plenum, which failed to shift economic reform into higher gear.

Singapore

- Advance estimates showed that Singapore’s economy grew 0.4% in the second quarter, up slightly from an upwardly revised 0.3% rise in the first three months of the year. Exports were the main driver of growth, led by the tech upturn. The domestic economy suffers from cautious consumer spending amid softening labor market conditions. The semiconductor sector could provide a lasting lift to exports, but an easing of global financing conditions will be required for investment and consumption to return to their old vigor.

- Headline inflation decelerated sharply to 2.4% year over year in June, down from 3.1% in May. But core inflation remains elevated at 2.9%. Further disinflation in core components will be required for the Monetary Authority of Singapore (MAS) to start unwinding its tight policy settings. The MAS will keep the policy band parameters unchanged at the July meeting; the path of inflation will inform their eventual easing.

Hong Kong

- Readings for April and May showed that growth likely slowed in the second quarter. Domestic demand remains tepid. Tight global monetary policy settings, a focus on fiscal consolidation, and a widening travel services deficit suggest a bumpy road ahead. The housing market is struggling amid elevated interest rates. Reforms like scrapping decade-old property cooling measures have not helped, with prices still declining at a double-digit rate. Hong Kong’s economy is also sensitive to the structural slowdown in mainland China.

- Disinflationary trends have persisted. But given the Hong Kong dollar's peg to the U.S. dollar, the Hong Kong Monetary Authority (HKMA) is not just data-dependent but also Fed-dependent. If the Federal Reserve begins to ease in September, the HKMA is likely to follow.

Australia

- Growth came to a near-standstill in the first quarter, with real GDP growing 0.1% quarter over quarter. Cost-of-living pressures and the associated tight monetary policy settings are dragging activity down. While household consumption was surprisingly firm, the boost was largely due to a revision to the methodology to calculate tourism imports. Consumer confidence is low, with spending concentrated in non-discretionary components. Private investment fell in the first quarter, and the unemployment rate is starting to climb. While all of this points towards soft momentum, the personal income tax cut will underpin growth in the second half of 2024.

- The Reserve Bank of Australia (RBA) left the cash rate unchanged at 4.35% at the last meeting, but turned more hawkish. Given the breadth and persistence of domestic inflation pressures, we expect the RBA to remain on hold until early 2025, which will also dampen the impact of stimulative fiscal policy on inflation.

Asia Pacific Economic Forecast July 2024

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability as an Illinois corporation under number 0014019. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation.

This material is directed to professional clients only and is not intended for retail clients. For Asia-Pacific markets, it is directed to expert, institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

For legal and regulatory information about our offices and legal entities, visit northerntrust.com/disclosures. The views, thoughts, and opinions expressed in the text belong solely to the author, and not necessarily to the author’s employer, organization, committee or other group or individual.

The following information is provided to comply with local disclosure requirements: The Northern Trust Company, London Branch, Northern Trust Global Investments Limited, Northern Trust Securities LLP and Northern Trust Investor Services Limited, 50 Bank Street, London E14 5NT. Northern Trust Global Services SE, 10 rue du Château d’Eau, L-3364 Leudelange, Grand-Duché de Luxembourg, incorporated with limited liability in Luxembourg at the RCS under number B232281; authorised by the ECB and subject to the prudential supervision of the ECB and the CSSF; Northern Trust Global Services SE UK Branch, UK establishment number BR023423 and UK office at 50 Bank Street, London E14 5NT; Northern Trust Global Services SE Sweden Bankfilial, Ingmar Bergmans gata 4, 1st Floor, 114 34 Stockholm, Sweden, registered with the Swedish Companies Registration Office (Sw. Bolagsverket) with registration number 516405-3786 and the Swedish Financial Supervisory Authority (Sw. Finansinspektionen) with institution number 11654; Northern Trust Global Services SE Netherlands Branch, Viñoly 7th floor, Claude Debussylaan 18 A, 1082 MD Amsterdam; Northern Trust Global Services SE Abu Dhabi Branch, registration Number 000000519 licenced by ADGM under FSRA #160018; Northern Trust Global Services SE Norway Branch, org. no. 925 952 567 (Foretaksregisteret), address Third Floor, Haakon VIIs gate 6 0161 Oslo, is a Norwegian branch of Northern Trust Global Services SE supervised by Finanstilsynet. Northern Trust Global Services SE Leudelange, Luxembourg, Zweigniederlassung Basel is a branch of Northern Trust Global Services SE. The Branch has its registered office at Grosspeter Tower, Grosspeteranlage 29, 4052 Basel, Switzerland, and is authorised and regulated by the Swiss Financial Market Supervisory Authority FINMA. The Northern Trust Company Saudi Arabia, PO Box 7508, Level 20, Kingdom Tower, Al Urubah Road, Olaya District, Riyadh, Kingdom of Saudi Arabia 11214-9597, a Saudi Joint Stock Company – capital 52 million SAR. Regulated and Authorised by the Capital Market Authority License #12163-26 CR 1010366439. Northern Trust (Guernsey) Limited (2651)/Northern Trust Fiduciary Services (Guernsey) Limited (29806)/Northern Trust International Fund Administration Services (Guernsey) Limited (15532) are licensed by the Guernsey Financial Services Commission. Registered Office: Trafalgar Court, Les Banques, St Peter Port, Guernsey GY1 3DA. Northern Trust International Fund Administration Services (Ireland) Limited (160579)/Northern Trust Fiduciary Services (Ireland) Limited (161386), Registered Office: Georges Court, 54-62 Townsend Street, Dublin 2, D02 R156, Ireland.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All