Hot Summer, Cool Data

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsDuring the hottest, muggiest waves of summer weather, we are glad to have indoor jobs with comfortable air conditioning. But when we look at recent economic developments, we detect a cooling wind blowing.

Inflation is falling, but so are employment gains. Talk of overheating is well in the past, and our focus has shifted to how quickly we will get some relief from high interest rates. Cuts are all but ensured; the debate is now over how large and frequent the upcoming reductions will be.

Following are our thoughts on recent data and developments.

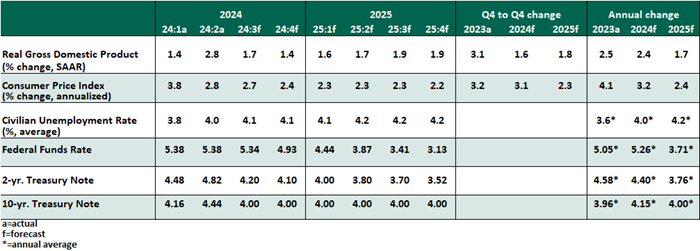

KEY ECONOMIC INDICATORS

Influences on the Forecast

- The employment situation summary for July 2024 showed a slow gain of 114,000 jobs. Growth in the labor force pushed the unemployment rate up by two-tenths to 4.3%. Average hourly earnings posted a cycle-low increase of 3.6% over the past year.

Viewed alone, these figures are acceptable; job creation continues, wage-driven inflation risk has faded, and unemployment in the low 4% range is historically good. But viewed relative to readings from earlier in the year, the report was something of a setback. The increase in the jobless rate triggered the “Sahm Rule,” which can indicate the start of a downturn.

Markets took an extremely risk-off turn in the wake of the report, amid fear of a recession taking hold and the Federal Reserve waiting too long to ease. We are mindful of the risks but do not draw the same catastrophic conclusions.

- U.S. gross domestic product grew at an annualized rate of 2.8% in the second quarter, well above expectations. Inventory accumulation was an important contributor, but real final sales to domestic purchasers grew 2.6%. Consumers and businesses remain in good shape. A notable soft spot was construction spending, with both residential and business investment in structures turning negative. Lower rates may offer some help to this sector going forward.

- Other labor market indicators suggest a stabilizing but not deteriorating jobs market. Job openings through June showed that openings are steady, but the rate of private sector hiring fell to a post-pandemic low. Weekly initial and continuing unemployment claims trended up through July. The challenge will be to keep the labor market steady at these levels and not see further deterioration.

- Inflation readings that disappointed to start the year were encouraging in the second quarter. The consumer price index (CPI) for July declined slightly from June, supported by lower energy prices. Core inflation (excluding food and energy) moderated to 3.3% over the last 12 months, a three-year low. The July reading showed a long-awaited improvement in the rate of increase for shelter costs, which must be sustained.

The June reading of the price index on personal consumption expenditures (PCE), the basis of the Federal Reserve’s 2% target, was similarly encouraging, gaining 2.5% overall and 2.6% on a core basis over the past year.

- At their July 31 meeting (preceding the employment report), the Federal Open Market Committee did not change monetary policy. Wording changes to the accompanying press release hinted at evidence of moderating inflation and softer employment conditions. Pressed on future intentions for the Fed Funds rate, Chair Powell remarked that “A reduction in the policy rate could be on the table as soon as the next meeting in September.”

Powell stated that the “totality of the data” must be consistent with loosening policy. Between improving inflation and worrying employment, those conditions are in place and unlikely to change, allowing a first cut at the September meeting.

In light of growing signs of economic moderation, we now anticipate easing at a pace of 25 basis points at each Fed meeting for the next year. Conditions do not warrant an out-of-cycle emergency action. Another disappointing employment report for August could compel an initial 50 basis point cut. The specific path of easing has always been unclear, but the case for caution has become less compelling.

A clearer path to Fed easing started some repricing of U.S. Treasury yields. Recent volatility across equity and foreign exchange markets then spurred a flight to quality, with flows to U.S. Treasuries weighing on yields. We expect the bond markets to settle.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All