After decades of economic stagnation, the Japanese economy appears to have rooted out deflation, albeit with some help from external forces. But the recent bout of market volatility suggests that Japan’s exit from easy money might not be that easy.

Last week, the Bank of Japan (BoJ) raised its policy rate by 15 basis points to 0.25%, the highest level since October 2008. The central bank also unveiled a roadmap for reducing its investment holdings, another step toward policy normalization. But the decision to start quantitative tightening and hike interest rates at the same meeting has drawn the ire of markets.

The Japanese Nikkei 225 stock market index closed down more than 12% on Monday, the most since Black Monday in 1987. The index covering Japanese banks recorded its biggest one-day plunge in history. Futures trading was suspended for the first time since the Fukushima nuclear plant incident in 2011. The yield on 10-year Japanese government bonds slid by the most in two decades.

The Japanese yen (JPY) has been appreciating in recent weeks in anticipation of further policy normalization. After the July meeting, the currency rallied further, rising sharply to levels not seen since the start of the year. The gain led to a rapid unwinding of yen “carry trades.”

A carry trade involves borrowing in a currency with a low interest rate, then reinvesting the principal in another country’s assets that offer higher returns. The strategy has been one of the biggest sources of flows in the global currency market. In fact, ultra-low interest rates and low volatility had made the yen the most popular funding currency in recent years.

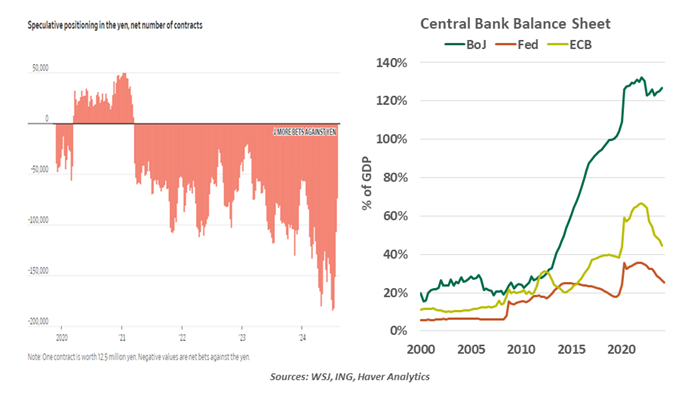

But when Japanese interest rates rise and the yen appreciates, the economics of carry trades fade. Investors rushed to the exits to avoid losses. According to Commodity Futures Trading Commission data, hedge funds and other speculative investors were holding over 180,000 contracts betting on a weaker yen on a net basis, worth over $14 billion, at the start of July. By the end of the month, those positions fell to around $6 billion.

While market volatility has put the BoJ’s plans for tightening on ice for now, the roadmap for trimming the bond buying program will likely remain unaffected. After an extraordinary expansion of its balance sheet over the past decade, the BoJ has decided to halve its pace of Japanese government bond (JGB) purchases by early 2026. The plan will reduce the central bank’s share of outstanding government bonds to 45% from 48% in two years.

The Bank of Japan shouldn’t rush to normalization.

The BoJ will have to tread cautiously in normalizing policy. The central bank not only needs to take into account market stability concerns, but also the macroeconomic fundamentals. Growth lacks legs to run, with real gross domestic product contracting in two of the last three quarters on an annualized basis. While summer bonuses helped real wages to turn positive for the first time in more than two years, consumption remained weak in June. Consumer spending, in real terms, has shrunk for four quarters in a row. The “core-core” inflation, which excludes fresh food and energy, has decelerated from a peak of 4.3% year over year in mid-2023 to 2.2% in June 2024.

Considering Japan’s decades-long experience with deflation, the BoJ should accept the risk of higher-than-target inflation. Aggressive tightening that jeopardizes the long-awaited normalization would be snatching defeat from the jaws of victory.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: Here is the latest news on the bond market, interest rates, and other fixed income sectors.

© Northern Trust

Read more commentaries by Northern Trust