We spend our days immersed in data: digesting news, identifying trends and studying past episodes. Historically, many variables move together in predictable ways. Extrapolating these trends is one way to anticipate what lies ahead.

However, the pandemic cycle broke a number of past relationships, making it more difficult than ever to identify turning points in the cycle. The list of failed rules of thumb includes:

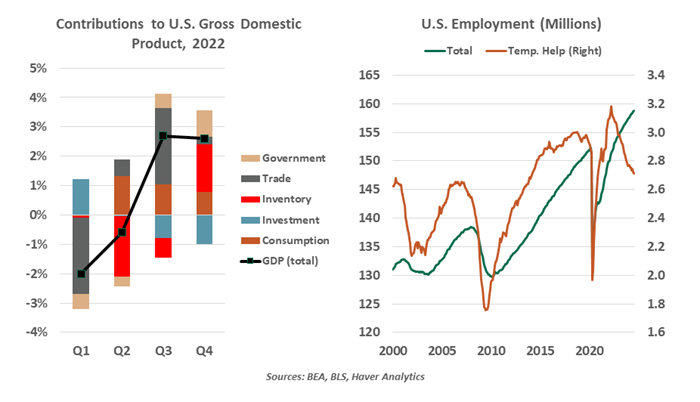

Two quarters of decline define a downturn. How do we determine when a recession has started? The complete answer is a nuanced review of a wide band of economic data, determined in arrears by the National Bureau of Economic Research (NBER). In practice, recessions are usually characterized by two consecutive quarters of economic contraction, which is the simple test that analysts often apply.

The U.S. economy declined during the first two quarters of 2022. But despite widespread fears, no recession took root. Amid unprecedented government support, job gains continued, consumer demand was sustained and business investment stayed buoyant.

Details are important when analyzing economic growth. The decline in the first half of 2022 was driven by unusually large shifts in highly variable components: inventory accumulation and net trade. Both of those series were whipsawed by pandemic disruptions. Final private domestic demand, which includes only consumption and investment, has grown throughout the cycle. This had happened only once before, in 1947, as the economy recalibrated after the global disruption of World War II.

Declines in temporary employment foreshadow broad job losses. As employers prepare to reduce headcount, they will usually start by cutting their temporary staff, who work on a contingent basis. In a normal cycle, those reductions spread to full-time staff reductions. In this cycle, temporary workers declined, but regular employment gains have held steady.

More than anything, this may illustrate a changing dynamic of the workforce. Employers are more likely to offer full-time employment, while gig workers may take sporadic assignments without the formality of working through a temporary staffing agency.

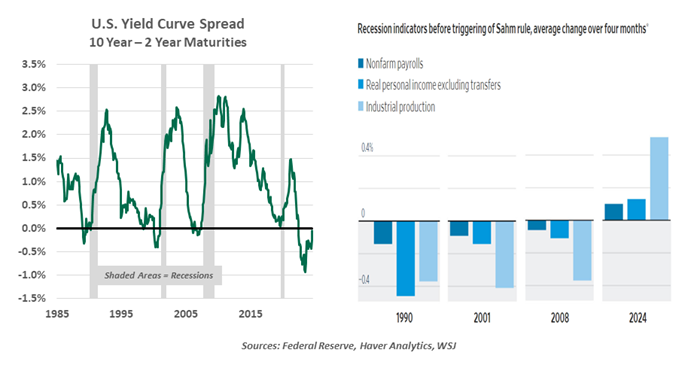

When the yield curve inverts, the economy is in trouble. We expect short-term yields to offer a lower return than long-term yields, reflecting the term premium required by investors to lock their money up for a longer time. When this relationship inverts, it can indicate that something is amiss.

We last discussed the limitations of the yield curve as a leading indicator in January 2023. While inversions have preceded most recessions, the curve gives us no clues as to the timing, cause or severity of the recession to follow. Since then, we have had a record-long curve inversion, but the economy and the equity markets have prospered throughout.

The challenge in using the yield curve as a cycle indicator is identifying what aspects of the fixed income market are out of equilibrium. If the short end falls because the Fed is lowering rates due to lower inflation, then the inversion can be corrected without a recession. What sounded like a tall tale in early 2023 has now become the base forecast.

We love simple rules, but they can mislead us.

The “Sahm Rule” is in play. Economist Claudia Sahm sought a more timely way to diagnose the onset of a recession than waiting for NBER’s expert judgment. Historically, when the three-month moving average unemployment rate rises by 0.5% from its prior-year low, a recession is unfolding. July’s 4.3% unemployment rate crossed this threshold.

Fortunately for us, Claudia Sahm is still a practicing economist, offering real-time commentary. She has frequently disclaimed she only identified a coincident pattern in the data, not a predictive or absolute rule. The unemployment rate is not at a worrisome level, having risen from a 50-year low, and its rise has been driven by greater participation. Other indicators of activity do not suggest an imminent recession. So many relationships have failed in this cycle, and her rule may be the next to fall.

The anomalies of the pandemic cycle (lockdowns, shortages, inflation, excess savings, revenge spending) have led to a series of failed economic relationships. I’m hoping that steadier times will allow us to find new rules to love.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust