I was recently asked about the seemingly strong “economic growth” rate as the Federal Reserve prepares to start cutting rates.

“If economic growth is so strong, as noted by the recent GDP report, then why would the Federal Reserve cut rates?”

It’s a good question that got me thinking about the trend of economic growth, the debt, and where we will likely be.

Since the end of the financial crisis, economists, analysts, and the Federal Reserve have continued to predict a return to higher levels of economic growth. The hope remains that the Trillions of dollars spent during the pandemic-driven economic shutdown will turn into lasting organic economic growth. However, the problem is that while the artificial stimulus created a surge in inflationary pressures, it did little to spark organic economic activity that would outlive the stimulus-related spending.

Pulling Forward Growth

Pulling forward growth over the last decade remains the Federal Reserve’s primary tool for stabilizing financial markets while economic growth rates and inflation remain weak. From repeated rounds of monetary and fiscal interventions, asset markets surged, increasing investor wealth and confidence, which, as Ben Bernanke stated in 2010, would support economic growth. To wit:

“This approach eased financial conditions in the past and, so far, looks to be effective again. Stock prices rose and long-term interest rates fell when investors began to anticipate the most recent action. Easier financial conditions will promote economic growth. For example, lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending.” – Ben Bernanke

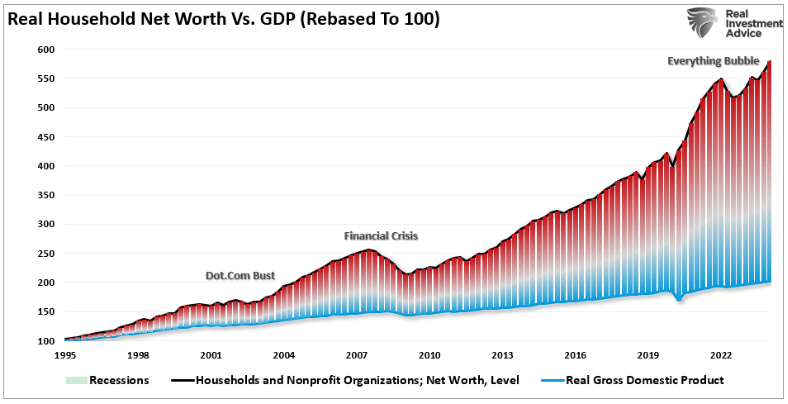

That certainly seemed to be the case as Federal Reserve interventions kept the financial markets and economy stable each time the economy stumbled. However, there is sufficient evidence that “monetary policy” leads to other problems, most notably a surge in wealth inequality without a corresponding increase in economic growth.

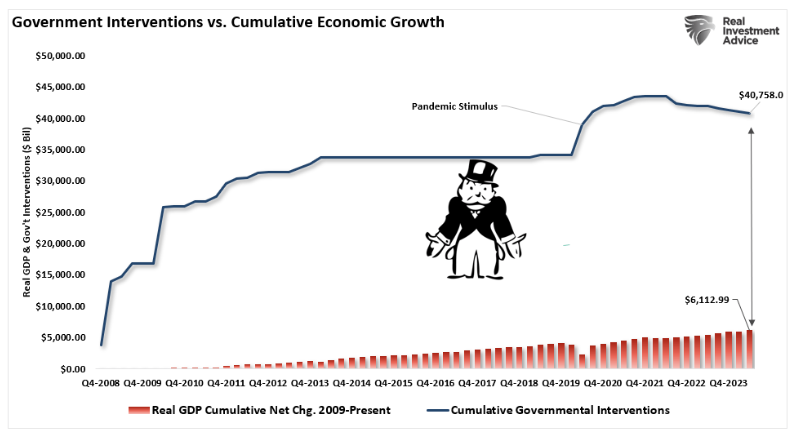

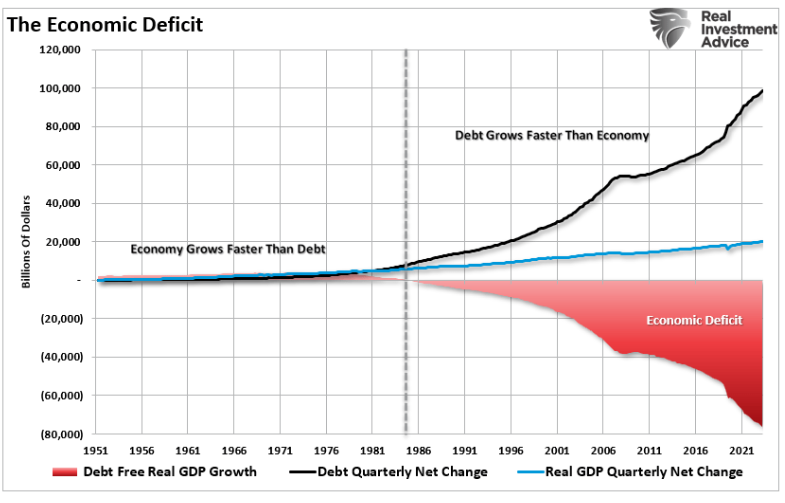

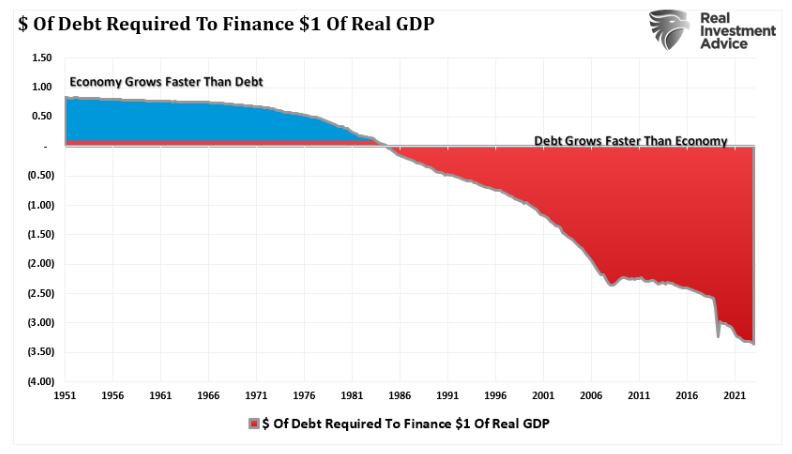

The inherent problem of pulling forward consumption is that while it may solve short-term economic concerns, it leaves an ever-larger “void” in the future that must be filled. The problem, unsurprisingly, is that “monetary policy” is not expansionary. As shown, since 2008, the total cumulative growth of the economy has been just $6.1 trillion. In other words, each dollar of economic growth since 2008 required nearly $6.7 of monetary stimulus. Such sounds okay until you realize it came solely from debt issuance.

Of course, the apparent problem is that sustaining this amount of debt-driven monetary policy is not realistic. But therein lies the issue of the “strong economic growth” narrative.

The Lack Of Economic Growth

While economists, politicians, and analysts point to current data points and primarily coincident indicators to create a “bullish spin” for the investing public, the underlying deterioration in economic prosperity is a much more critical long-term concern. The question that we should be asking is, “Why is this happening?”

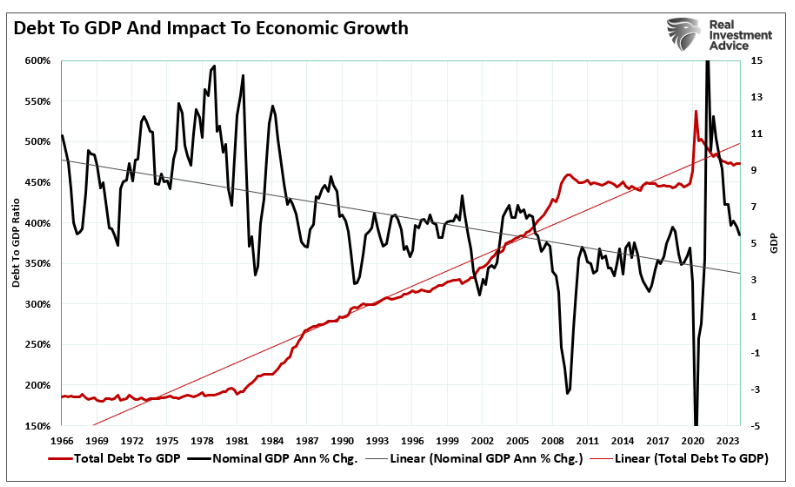

From 1950-1980, nominal GDP grew at an annualized rate of 7.55%, accomplished with a total credit market debt to GDP ratio of less than 150%. The CRITICAL factor is that economic growth trended higher during this span, going from roughly 5% to a peak of nearly 15%. There were a couple of reasons for this. First, lower debt levels allowed personal savings to remain robust, which fueled productive investment in the economy. Secondly, the economy was focused primarily on production and manufacturing, which had a high multiplier effect on the economy. This feat of growth also occurred in the face of steadily rising interest rates, which peaked with economic expansion in 1980.

The Lack Of Economic Growth

While economists, politicians, and analysts point to current data points and primarily coincident indicators to create a “bullish spin” for the investing public, the underlying deterioration in economic prosperity is a much more critical long-term concern. The question that we should be asking is, “Why is this happening?”

From 1950-1980, nominal GDP grew at an annualized rate of 7.55%, accomplished with a total credit market debt to GDP ratio of less than 150%. The CRITICAL factor is that economic growth trended higher during this span, going from roughly 5% to a peak of nearly 15%. There were a couple of reasons for this. First, lower debt levels allowed personal savings to remain robust, which fueled productive investment in the economy. Secondly, the economy was focused primarily on production and manufacturing, which had a high multiplier effect on the economy. This feat of growth also occurred in the face of steadily rising interest rates, which peaked with economic expansion in 1980.

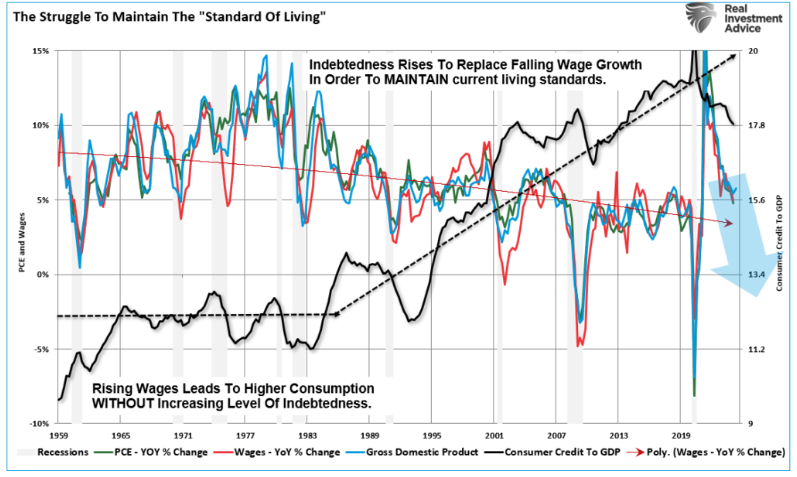

That is why the economic prosperity of the last 40-years has been a fantasy. While America, at least on the surface, was the world’s envy for its apparent success and prosperity, the underlying cancer of debt expansion and declining wages was eating away at the core. The only way to maintain the “standard of living” was to utilize ever-increasing debt levels. The now-deregulated financial institutions were only too happy to provide that “credit” as it was a financial windfall of mass proportions.

Why “Socialism” Is Rising

The massive indulgence in debt, what the Austrians call a “credit-induced boom,” has likely reached its inevitable conclusion. The unsustainable credit-sourced boom, which led to artificially stimulated borrowing, has continued seeking ever-diminishing investment opportunities. Ultimately, these diminished investment opportunities repeatedly lead to widespread mal-investments. Not surprisingly, we saw it play out “real-time” in everything from subprime mortgages to derivative instruments in 2008, which were only to milk the system of every potential penny regardless of the apparent underlying risk. We see it again in the “chase for yield” in everything from junk bonds to equities. Not surprisingly, the result will not be any different.

The struggle of the American middle class continues growing, with the wealth gap between the rich and poor glaringly apparent. That is why the cries for socialism are becoming so loud. The demands for free healthcare, education, and housing are the “siren’s song” for politicians to enact more legislation to expand Government control and redistribute wealth from the middle class and poor to the ruling elite.

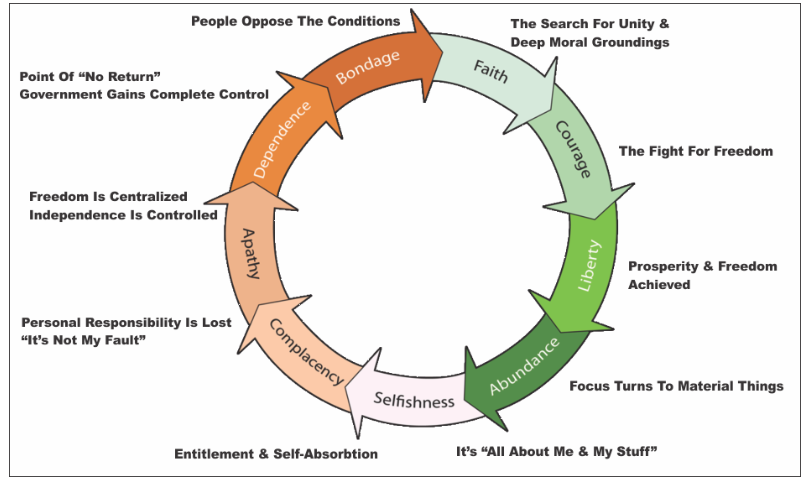

The Tytler Cycle

But such shouldn’t be a surprise. It is the cycle of all economic civilizations over time as we “forget our history” and become doomed to repeat it. Scottish economist Alexander Tytler, who, in 1787, commented on the then-new American Republic as follows:

“A democracy is always temporary in nature; it simply cannot exist as a permanent form of government. A democracy will continue to exist up until the time that voters discover they can vote themselves generous gifts from the public treasury. From that moment on, the majority always votes for the candidates who promise the most benefits from the public treasury, with the result that every democracy will finally collapse due to loose fiscal policy, which is always followed by a dictatorship.

The average age of the world’s greatest civilizations has been about 200 years. These nations always progressed through this sequence:“

The idea of socialism sounds excellent in theory. However, debt for non-productive investments such as social welfare and free college doesn’t produce the promised economic benefit. Instead, the resulting inflation from the influx of “free money” crimps economic growth. Furthermore, inflation “taxes” the bottom 50% of income earners the most.

The promise of something for nothing will never lose its luster. However, no society ever prospered through socialism or communism. The poor remained poor, the middle class became poor, and the wealthy prospered. Therefore, we should view socialism as political propaganda rather than economic or public policy. And like all propaganda, we must fight it with appeals to reality. Socialism, where deficits don’t matter, is an unreal place.

Conclusion

It is likely that “something has gone wrong” for the Federal Reserve as the efficacy of pulling forward future consumption through monetary interventions has been reached. Despite ongoing hopes of “higher growth rates” in the future, such will likely not be the case until the debt overhang is eventually cleared.

Does this mean that all is doomed? Of course not. However, we will likely remain constrained in the current “spurt and sputter” growth cycle we have witnessed since 2009. Such will be marked by continued volatile equity market returns and a stagflationary environment as wages remain suppressed while living costs rise. Ultimately, clearing the excess debt levels will allow personal savings rates to return to levels promoting productive investment, production, and consumption.

The end game of four decades of excess is upon us, and we can’t deny the weight of the debt imbalances that are currently in play.

But more socialism is not the answer.

Lance Roberts is a Chief Portfolio Strategist/Economist for RIA Advisors.

He is also the host of “The Lance Roberts Podcast” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance on Facebook, Twitter, Linked-In and YouTube

Customer Relationship Summary (Form CRS)

Disclosure

Real Investment Advice is powered by RIA Advisors, an investment advisory firm located in Houston, Texas with over $1 billion in assets under management. As a team of certified and experienced professionals, we seek to provide our clients with educational services and the necessary information and tools to educate you in the field of finance, investing and economics. To this end, you can use the Real Investment Advice Platform to avail yourself of various video, audio and proprietary collections of information at your leisure to learn and gather the necessary information that you may need in the fields of investment news, investment opinion, financial news, financial opinion, economic news and economic opinion, finance, investing and economics. Utilizing the functionality and tools provided by Real Investment Advice, you can access this information in a variety of ways, including via video and audio programming, audio and visual media content streaming services, downloadable audio-visual media, uploaded, posted or tagged third-party videos, receiving or viewing audio and video clips, blogs, podcasts, and YouTube videos, all of which are accessible on the Real Investment Advice media platform and/or various Internet and communications links that are accessible via the Real Investment Advice Platform and allow for the broadcasting, transmission and streaming of the information and audio-visual content to your media devices and other communications platforms for your viewing and listening pleasure. All of these tools and sources of information are made available to you so that you can utilize the same to make the right financial, economic and investment decisions.

RIA Advisors offers multiple custodial arrangements, either directly of through wholly owned subsidiaries, with Fidelity and Interactive Brokers.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Real Investment Advice

Read more commentaries by Real Investment Advice