Economic indicators are released every week to provide insight into a country’s overall economic health. They serve as essential tools for policymakers, advisors, investors, and businesses because they allow them to make informed decisions regarding business strategies and financial markets. In the week ending August 22, the SPDR S&P 500 ETF Trust (SPY) rose 0.57%, while the Invesco S&P 500 Equal Weight ETF (RSP) was up 1.02%.

This article examines three indicators from last week – existing home sales, new home sales, and the Conference Board’s leading economic index. The housing indicators provide an update on the state of the housing market and could impact home builders and residential real estate ETFs such as Invesco Dynamic Building & Construction ETF (PKB), iShares U.S. Home Construction ETF (ITB), SPDR S&P Homebuilders ETF (XHB), and iShares Residential and Multisector Real Estate ETF (REZ). Meanwhile, the leading economic index can provide an early indication of significant turning points in the business cycle.

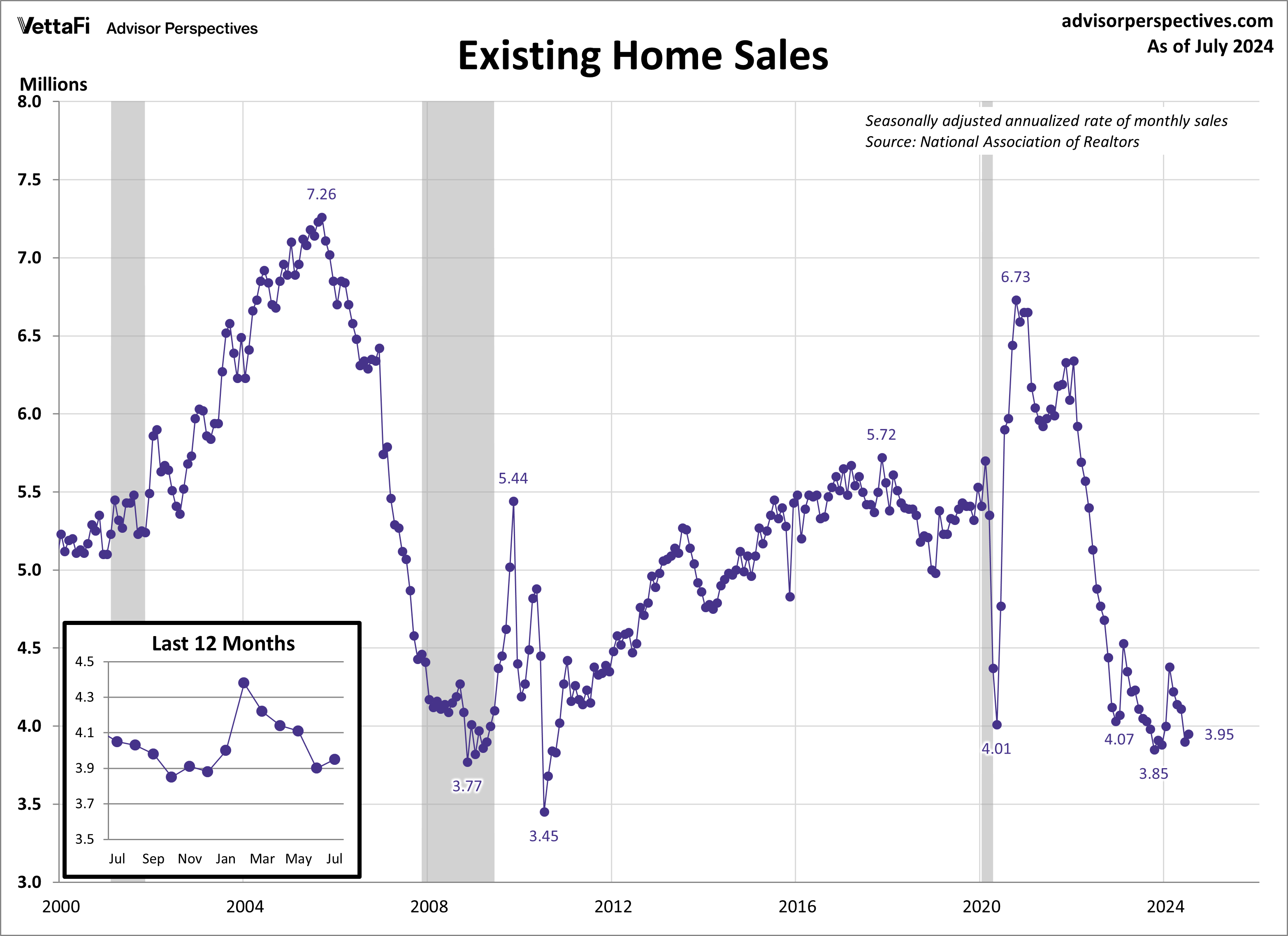

Existing Home Sales

Existing home sales rose for the first time since February, breaking a four-month decline. In July, sales increased by 1.3% from the previous month, reaching a seasonally adjusted annual rate of 3.95 million units. This figure was slightly higher than expected, surpassing the projected 3.94 million units. Despite this uptick, sales remain at historically low levels, comparable to those seen during the Great Recession. However, there is optimism among potential buyers as improved supply and declining mortgage rates offer hope for increased activity in the near future.

The median price for an existing home fell for the first time since January, dropping to $422,600. With that said, the median price sits just below its all-time high from June of $426,900. Compared to a year ago, the median price for an existing home is up 4.2%, marking the thirteenth consecutive month of year-over-year increases for existing homes.

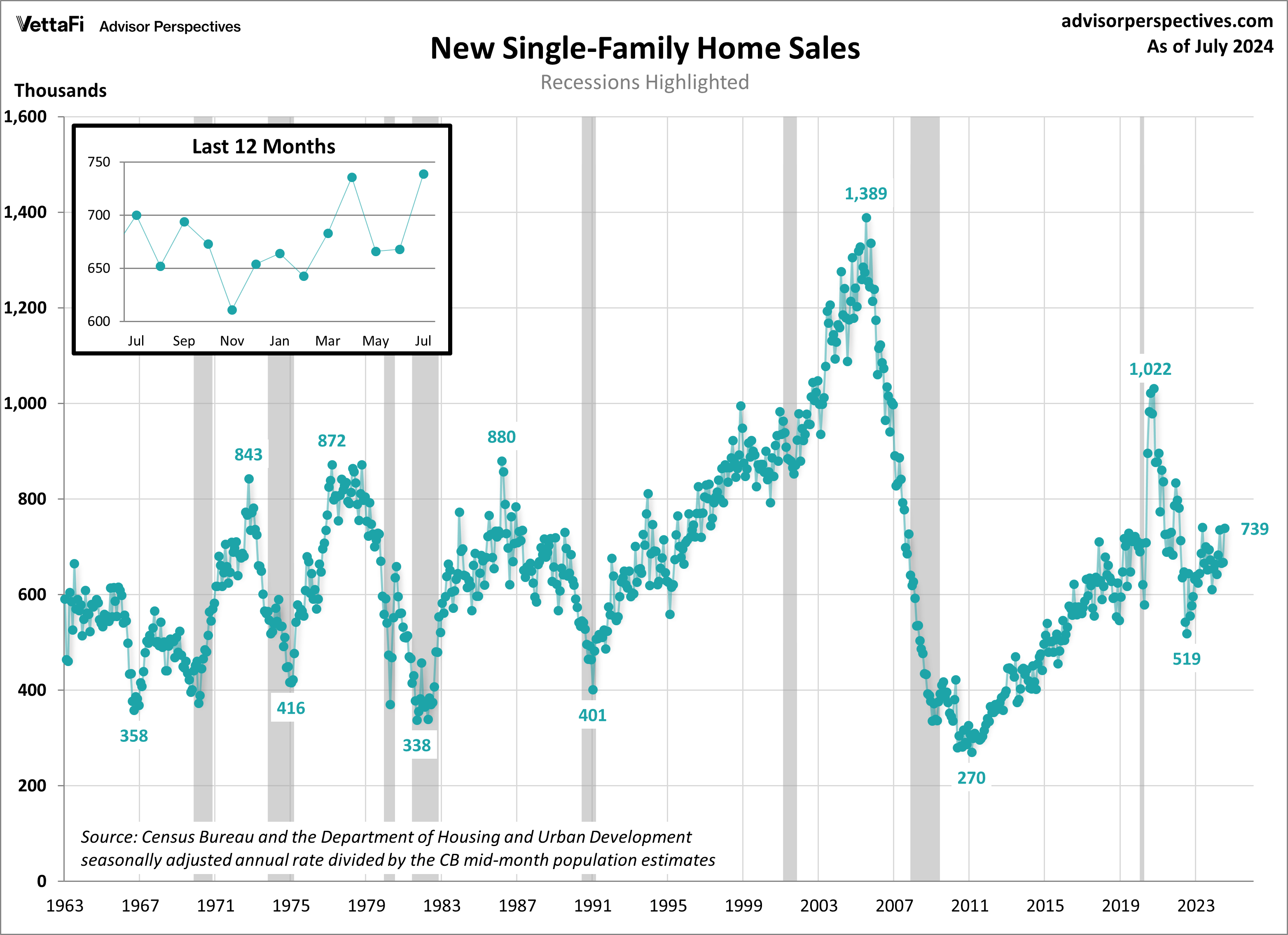

New Home Sales

Another key housing indicator showed renewed strength this week as new home sales surged to a fourteen-month high. In July, sales jumped 10.6% to a seasonally adjusted rate of 739,000 units, well above the expected 624,000 units. This marks a 5.6% increase from one year ago. With inventory for existing homes still low, homebuyers are increasingly turning to new construction. Additionally, moderating mortgage rates have made new homes even more attractive. While new home sales can be volatile month-to-month, the six-month moving average (6-month MA) offers a clearer picture. In July, the 6-month MA climbed to its highest level since September 2023, providing further evidence that the housing market may be on the path to recovery.

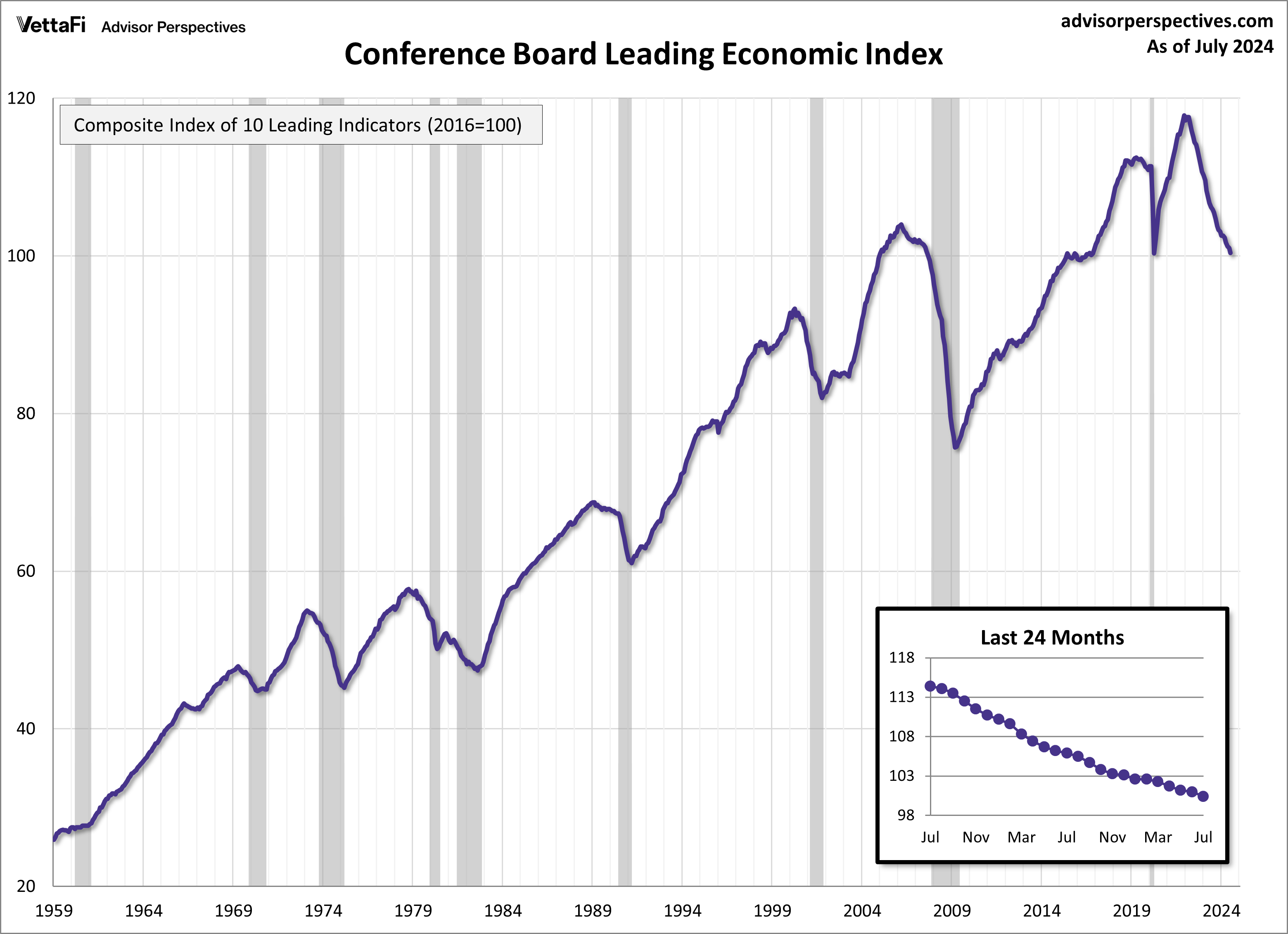

Leading Economic Index

The Conference Board Leading Economic Index (LEI), a composite index designed to predict the economy’s trajectory, fell more than expected last month. In July, the LEI fell 0.6% to 100.4 – now just 0.1 points above its most recent low from April 2020. The index was projected to only fall 0.4% from the previous month. The LEI has now declined or been flat for 29 straight months, but the Conference Board indicated that the six-month annual growth rate is no longer signaling a recession in the future.

A breakdown of the latest report showed that five of the index’s ten components made negative contributions, mostly coming from the non-financial components, including consumer expectations for business conditions, new orders, building permits, and average weekly hours. Additionally, the interest rate spread remained negative. While the LEI signaled a recession for all of last year, over the past four months it has switched off its recession signal, but continues to suggest downward pressure on economic activity in the near future.

Economic Indicators and the Week Ahead

The upcoming week will offer insights into the nation’s economic health and activity with the release of the second estimate for Q2 GDP and July’s PCE price index data, better known as the Fed’s preferred measure of inflation.

The second estimate is currently forecasting that the U.S. economy grew at a rate of 2.8% in the second quarter, twice as fast as the 1.4% rate from the first quarter. Meanwhile, headline and core PCE have slowly trended downward towards the Fed’s 2% target rate over the past few years with the latest readings at 2.5% and 2.6%, respectively.

For more news, information, and strategy, visit the Innovative ETFs Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi