Whether from my favorite chair in our den or from my spot at the kitchen table, I have a good view of our deck. When we have bread products past their “use by” date we break apart the bread and place it in on the railing for the birds. I have noticed there is a pecking order when the birds come to eat. The littlest birds come first, the cardinals and blue jays come next, and then the big crows come in for “cleanup” detail. Occasionally, the birds come “out of order” and a ruckus ensues until proper order is restored.

Watching the birds jostle for position reminds me there is a proper order to design a successful 401(k) plan. While it is tempting to start with a plan’s investments, these are not as important to the success of the plan as the structure of the plan itself.

The right plan design is crucial for making a 401(k) effective for both owners and employees, addressing both near-term and long-term objectives. This is particularly important for small businesses, where profits often pass through to the owner’s individual tax return. Profitable businesses present plan design optimization opportunities.

Focus on features before funds

Plan design determines key components of the plan, such as employee eligibility, automatic features (auto-enrollment and auto-escalation), whether the employer wants to match any contributions, and by how much, vesting schedules, profit-sharing, and the contribution limits for business owners and key employees. Notably, eligible plan expenses are business expenses that may be tax deductible for the business, thereby lowering pass-through taxable income to the business owner.

The good news is that plan design experts are available to help you and your client find features that make the most sense. Third-party administrators (TPAs) can gather data and goals from your client to identify plan features that are customized for their situation. Often, basic information on the ages of employees and incomes, when combined with the owner’s goals, goes a long way in optimizing features.

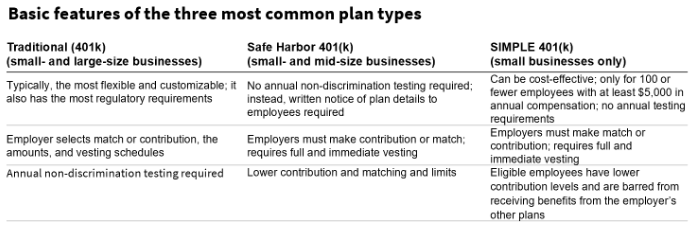

What is key about the chart above, is the “traditional 401(k)” category contains variations. For example, there are other creative options to meet a client’s unique needs, including profit sharing plans, cash balance plans, age-weighted plans, and Social Security integrated plans. It’s important to know that options exist. Your TPA partner will sort out which option is best-suited for optimization.

The pecking order: Prioritizing plan features

Just as birds establish a pecking order, financial professionals must prioritize certain plan features based on the needs of their participants and business-owner clients. This could mean emphasizing employer match programs to encourage participation, offering Roth 401(k) options for tax diversification, including automatic escalation to help participants increase their savings rate over time, all while maximizing the tax benefits of offering a plan.

In conclusion, optimizing a 401k plan design is a delicate balancing act, much like maintaining the pecking order within a flock of birds. By keeping the needs of all participants in mind and prioritizing the right plan features, financial professionals can create a 401k plan that prioritizes employee outcomes while meeting business owner objectives.

Next steps for financial professionals:

- Ask every business-owner client, “How happy are you with the tax efficiency of your company’s retirement plan?”

- Listen intently for business owners who do not have plans or have not recently analyzed their current plan from this perspective.

- Remember, your goal is to start this conversation to reach agreement to set up a plan design consultation call with a TPA with your recordkeeper partner. You do not need to be a plan design specialist.

- Ask anyone you know with an existing plan, “How happy are you with the amount you and your key employees have been able to contribute to your retirement plan in recent years?”

- Often a three- to four-year-old plan has not been reviewed for design optimization. One sign of an out-of-date plan design is when owners and key employees are unable to maximize the use of the plan.

- Ask anyone you know who doesn’t have a plan, “If you could potentially lower your personal tax liability and receive tax credits to offset the costs of running a retirement plan, how interested would you be in learning about these plan design features?”

I am not a plan design specialist. However, I know where to turn for plan design help. The momentum that exists in new plan formation and plan optimization means we all need reliable partners to efficiently win as often as possible. Your Franklin Templeton Workplace Retirement Solutions team is ready to partner to ensure your retirement plan success.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our videos.

© Franklin Templeton

Read more commentaries by Franklin Templeton