Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

As the proverb goes, patience may be a virtue, but we simply are not built for… dare I say patience? It can be argued that we have morphed into a society of instant gratification. We don’t just want food – we want fast food. No one wants to stand in line at the bank. We prefer to conduct our business through phone apps. A prolonged diet of less calories is now being replaced by a pill or injection that can quickly get us to target weight.

But there can be consequences to these hasty acts. Food on demand may come with less healthy attributes. Rapid bank withdrawals were a contributing factor to the latest bank failure, and the long-term effects associated with diet replacements may yet be seen.

So, when we are viewing the markets, it is not surprising that sentiment shifts quickly if we don’t instantly see the anticipated results. Market pundits quickly point fingers and determine that the Fed, economists, and participants are wrong. Reactions can be powerful in number and sway momentum for stocks and/or bonds.

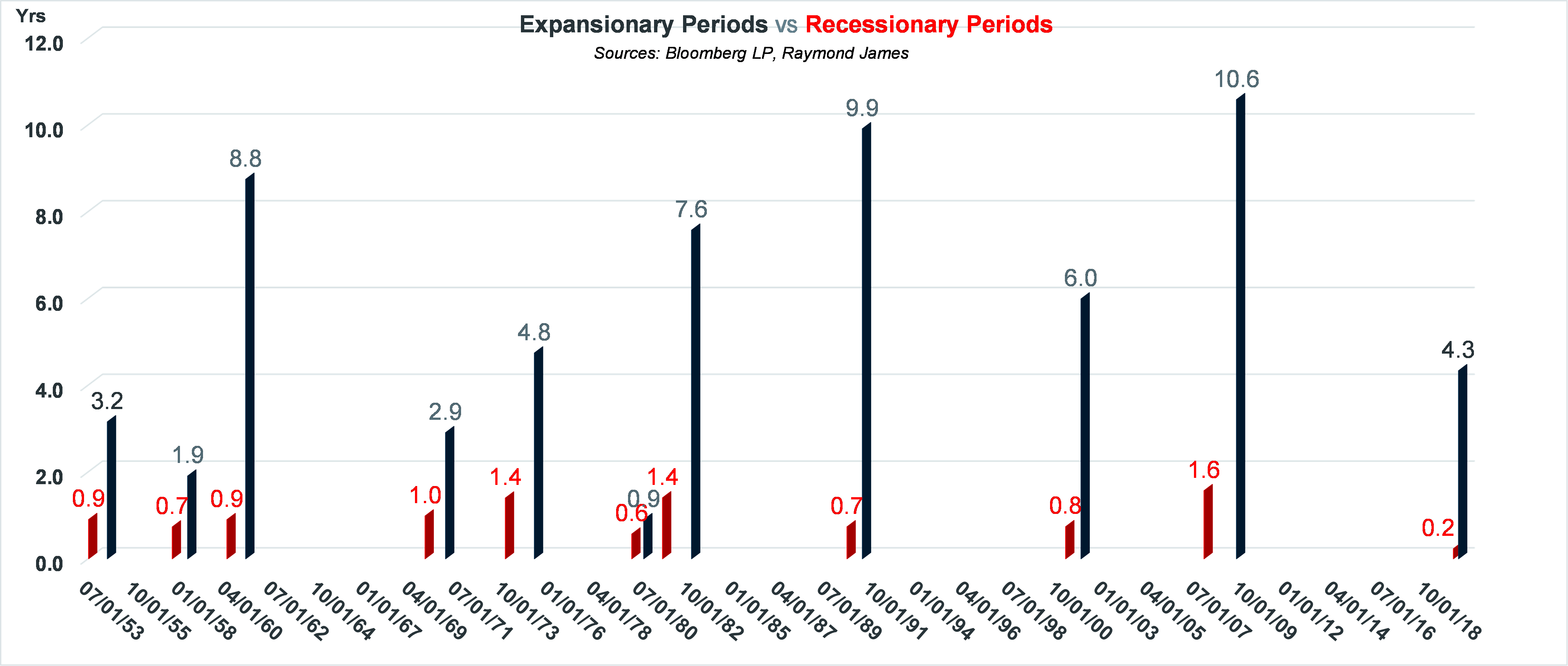

The reality is that economic cycles can be quite long. The following chart shows the length of expansionary and recessionary periods over the last 70 years. The position of each bar represents the start of each respective period.

Economic cycles last about 6.5 years with the recessionary period averaging 0.9 years and the expansionary period running around 5.5 years. The latest five recessionary periods have averaged 0.9 years; however, the last five expansionary periods have averaged 7.0 years. It is fair to say that artificial means have been used to push expansionary periods to last longer. The Fed has intervened with rate policy, quantitative easing, and open market operations in capacities never used before. These operations have extended the economy’s expansionary periods.

The consequence of this cycle’s intervention has been inflation - more money chasing goods and services. The last two cycles came to abrupt closure due to the catastrophic events of COVID and the subprime mortgage crisis. Although this cycle has not yet unveiled such a calamity, the consequences of intervention, albeit very slowly, are creeping into play. Government and consumer debt are on the rise. Consumers were flush with cash during COVID with nowhere to spend money. Now, not only have consumers depleted those savings to below long-term averages, but they have also continued to spend and prop up the markets. However, spending appears to be on borrowed funds as, according to Federal Reserve data, revolving credit is pushing to new highs month after month.

The cycle is extended, but it will be completed. At the end of the cycle, historically rates decline. In the interim, investors are fortunate to have the option to extend out on the curve and lock into higher rates for longer. The current inverted curve has reached a historic length, and although it has flattened out dramatically over the last couple of months, the 3-month T-Bill continues at a rate of 126 basis points over the 10-year Treasury. Investors have benefitted from short-term rates, but as the cycle plays out, locking into longer-term rates will provide for more long-term stability in your portfolio.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

To learn more about the risks and rewards of investing in fixed income, access the Financial Industry Regulatory Authority’s website at finra.org/investors/learn-to-invest/types-investments/bonds and the Municipal Securities Rulemaking Board’s (MSRB) Electronic Municipal Market Access System (EMMA) at emma.msrb.org.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Raymond James

Read more commentaries by Raymond James