Doug Drabik discusses fixed income market conditions and offers insight for bond investors.

Investors may find themselves prognosticating about future rates relative to current rates in an attempt to optimize their portfolio. The difficulty with this is reigning in the seemingly countless variables that determine forward rates. Economists, analysts, strategists, traders, and investors may have a multitude of rationales for selecting the most favorable blend of investments and risk, which, based on these findings, may allow for desirable results. The disputing points of observation and data analysis lay the groundwork for market volatility. It can get complicated; however, sometimes, we may make it difficult when it doesn’t necessarily need to be.

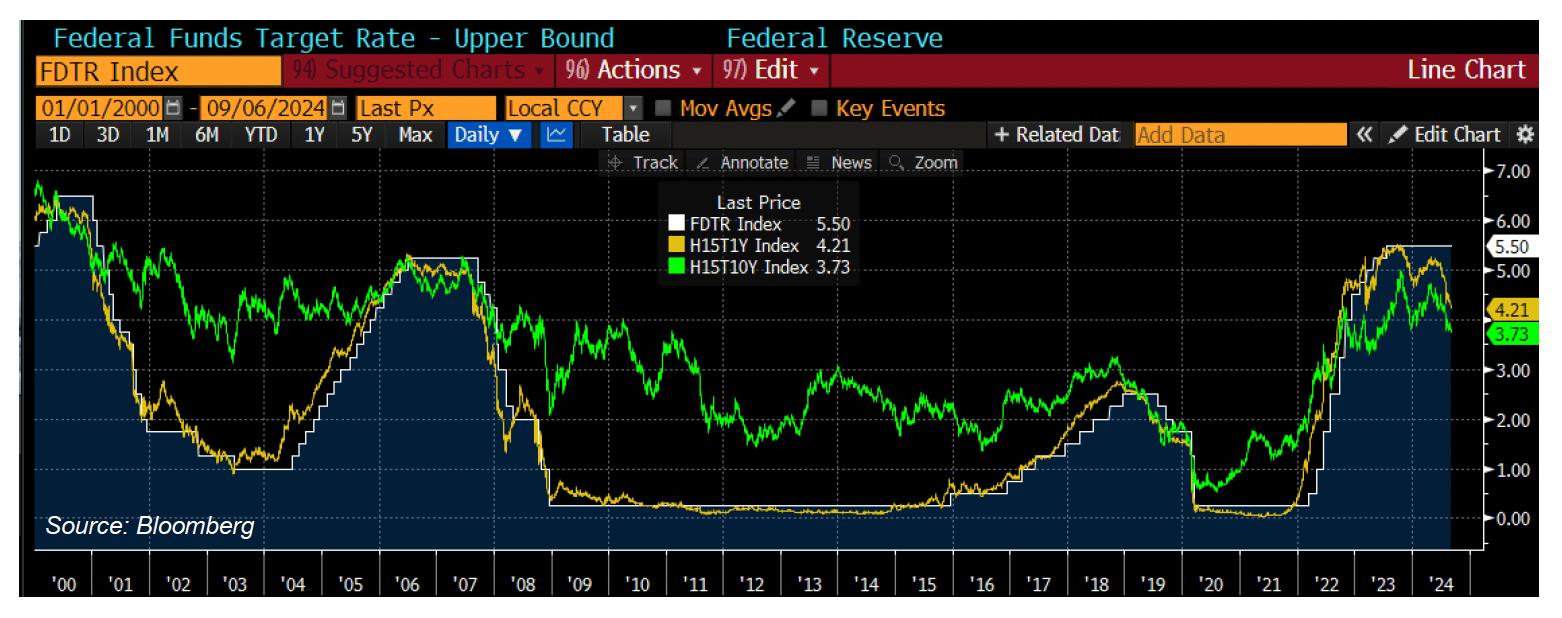

Here's what we know. The 10-year versus 3-month Treasury yields remain inverted. Historically, inverted curves precede recessions. Yield curves that develop after inversions tend to reflect lower all-around rates. When Treasury yield curves finally become “normal” or upward-sloping, it takes another 8 to 12 months until the flat curve manifests in a steep upward slope (long-term maturities provide a significant amount of additional yield versus short-term maturities). This slope steepening typically occurs in the middle of the recession. There is a consensus that the Fed will start cutting interest rates as soon as their next meeting in nine days. This graph demonstrates that all maturity rates will not necessarily move parallelly should the Fed begin to drop the Fed Funds rate.

The white line or blue shaded area depicts Fed Funds. The one-year Treasury (gold line) is correlated with the Fed Funds rate. The green line is the 10-year Treasury. It appears that the 10-year Treasury leads (begins to drop) or anticipates the Fed move down. It is also evident that the 10-year Treasury does not parallel the Fed Funds movement.

What can we conclude?

If history repeats, and it often does, today’s 10-year Treasury has already anticipated the upcoming Fed cuts. It can be argued that it will not continue to trail down in rate (at least at the same pace) even if the Fed continues to cut the Fed Funds rate. This moment may be the time in the economic cycle when the path to the Treasury curve moves from a state of inversion to a normal upward slope – with short-term rates falling much faster than intermediate to long-term rates. To point, in August, the 1-year Treasury rate fell 34 basis points – almost three times as much as the 12 basis points the 10-year Treasury fell.

Should inflation continue to decline, employment numbers persist in weakening, and consumer spending shrinks, the Fed will likely begin its softening policy with a sequence of Fed Fund rate cuts. It is not a given since many pundits predict inflation may inch back up, but that is an argument for another day. Investment money that is short and not earmarked as liquidity can still take advantage of elevated rates in the intermediate and long term while they last, thus locking into higher income levels for longer. An individual bond-laddered approach of spreading maturities over a range of time can mitigate interest rate risk by ensuring that all portfolio investments do not mature simultaneously. This can further insulate investors from unforeseen adverse future rate environments.

The author of this material is a Trader in the Fixed Income Department of Raymond James & Associates (RJA), and is not an Analyst. Any opinions expressed may differ from opinions expressed by other departments of RJA, including our Equity Research Department, and are subject to change without notice. The data and information contained herein was obtained from sources considered to be reliable, but RJA does not guarantee its accuracy and/or completeness. Neither the information nor any opinions expressed constitute a solicitation for the purchase or sale of any security referred to herein. This material may include analysis of sectors, securities and/or derivatives that RJA may have positions, long or short, held proprietarily. RJA or its affiliates may execute transactions which may not be consistent with the report’s conclusions. RJA may also have performed investment banking services for the issuers of such securities. Investors should discuss the risks inherent in bonds with their Raymond James Financial Advisor. Risks include, but are not limited to, changes in interest rates, liquidity, credit quality, volatility, and duration. Past performance is no assurance of future results.

Investment products are: not deposits, not FDIC/NCUA insured, not insured by any government agency, not bank guaranteed, subject to risk and may lose value.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Raymond James

Read more commentaries by Raymond James