All eyes this past week were on the U.S. jobs report, which came out on Friday morning. The numbers were improved from the prior month, comforting those who have been concerned about rising unemployment. As Federal Reserve Chairman Jay Powell said during his address to last month’s Jackson Hole conference, “We do not seek or welcome further cooling in labor market conditions.” The most recent readings should allow the Fed to lower rates gradually, not suddenly.

Viewed over time, however, many large economies are facing the challenge of worker deficits, not surpluses. Conditions during the pandemic were extreme, but secular excesses of labor demand over supply have been building for the past fifteen years.

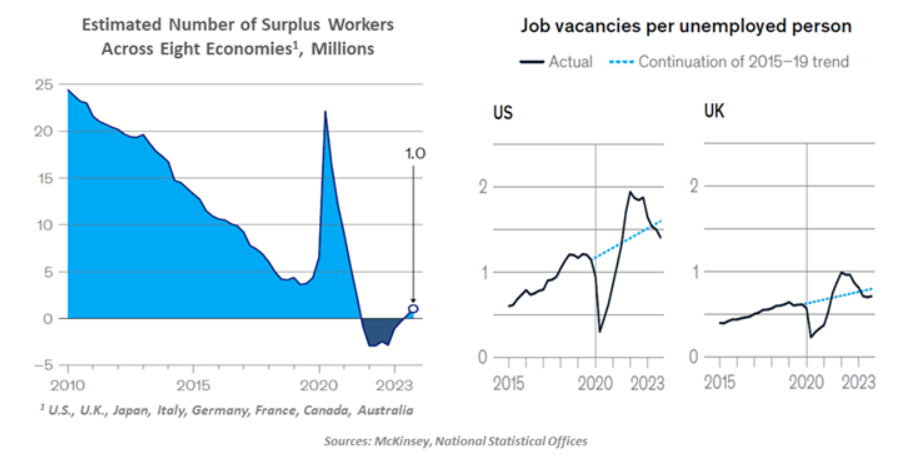

Recent work from the McKinsey Global Institute clearly illustrates this progression. The 2008 Global Financial Crisis left many out of work, and the slow recovery from that episode kept ratios of job openings to job seekers very low. But starting in 2015, labor market capacity began declining. The pandemic years created a rude interruption, but the long-term trend has been re-established.

In several large countries, job openings are still well in excess of available workers. McKinsey finds that skills mismatches do not explain much of the gap; job vacancy rates are highest in occupations that are at the lower end of the wage scale, and should therefore be within the reach of most of those seeking work.

Demographic trends are leading to growing labor shortages in many countries.

Demographic trends are driving these long-term developments. At the end of this decade, more than one quarter of the population across the eight countries studied by McKinsey will be over the age of 65. The United Nations estimates that one in four people globally live in a country whose population has peaked.

Immigration can compensate for domestic talent deficits. Newcomers can accept many open roles without requiring training, instantly boosting labor supply. But sentiment towards immigration has turned negative in many places. Italy, where the native-born population has been shrinking for a long time, has been especially active in restricting entry.

The current cyclical focus on unemployment is important, but the longer-running trend toward larger labor deficits is a far bigger economic issue.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust