Fed Preview: Be Quick, but Don’t Hurry

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThe American coach John Wooden was famous for his “Pyramid of Success.” International audiences became acquainted with its contents through the television series “Ted Lasso.”

One of Wooden’s bromides, borrowed for this commentary’s title, encourages action rooted in firmness of conviction. It discourages rash movements that might be regretted later on. As the Federal Reserve gathers to contemplate American monetary policy next week, they will do well to keep Wooden in mind.

The September 18 decision is nearly certain to yield the first in a series of rate cuts, but the structure of the easing cycle is up for debate. Should the Fed move gradually, or front-load its actions to offer more rapid relief? Here is our analysis of the points of debate which may arise next Tuesday and Wednesday, and in meetings to follow.

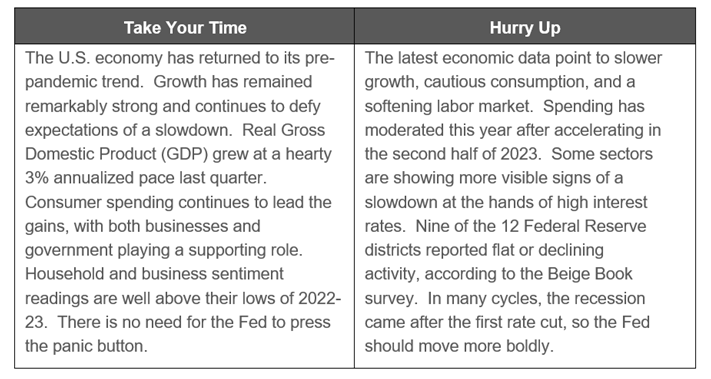

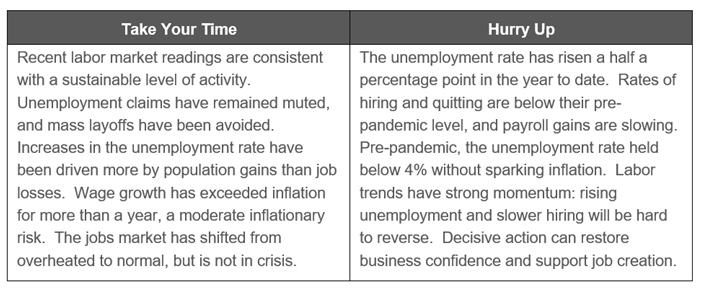

Economic Growth

The U.S. economy might appear to be on the brink of a recession, with an inverted Treasury yield curve and the Sahm Rule triggered by rising unemployment. But as we highlighted here, previously reliable recession indicators have not worked in this cycle.

Income, consumer spending and employment are all growing. None reflect signs of an imminent downturn. While there are pockets of concern, the perception that consumers are completely tapped-out is not accurate. Household balance sheets, in aggregate, are still very healthy.

All of that said, the economy is showing signs that it cannot withstand a sustained period of high rates. The longer monetary policy remains in restrictive territory, the higher the chances of a hard landing. A steady pace of easing should be enough to take a worst-case scenario off the table.

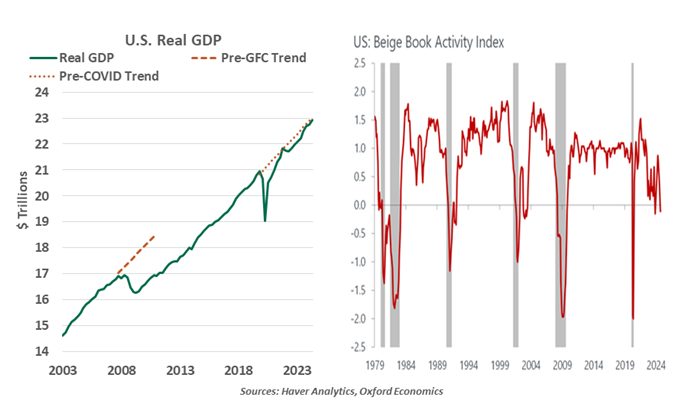

Inflation

Inflation has been well-behaved over the past several months. The slowing labor market is contributing to gradual softening of price pressures across domestically-focused services. Shelter costs continue to escalate briskly, but increases in this category do not have to reach 2% for the overall inflation target to be satisfied. The benign readings have given Federal Reserve Chair Powell more confidence that inflation is on a sustainable path toward the 2% target and allowed him to turn attention to both sides of its dual mandate.

More cautious voices will note that the Fed was reasonably confident of reaching the inflation target coming in to 2024, only to see unwelcome increases in monthly readings. That series set back the start of the easing campaign, and argues for caution in reducing interest rates. We’ve had very good fortune with energy and goods prices, which may not persist. The dollar has lost some ground in currency markets, raising the potential for higher import costs. Cutting aggressively may risk rekindling inflation at a very unwelcome time.

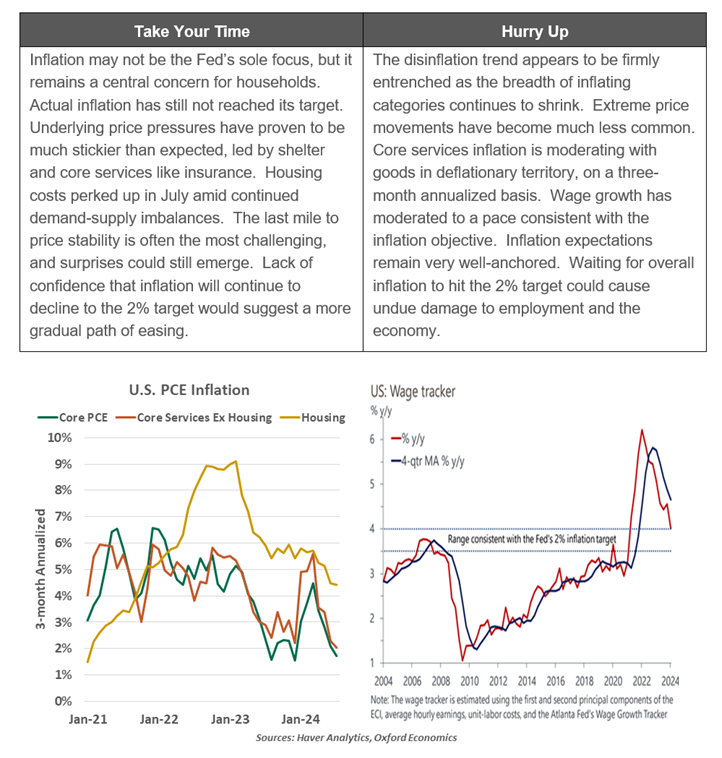

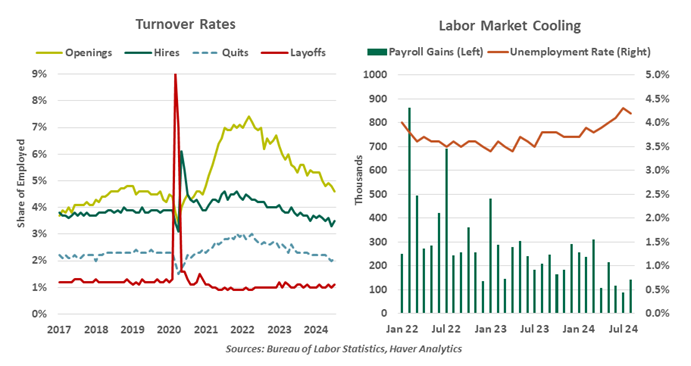

Employment

Assessing the labor market is difficult, given a series of measurement challenges. The unemployment rate requires estimates of both the working population and the total population available to work; recent immigration has complicated the collection of these data. Falling survey response rates and funding constraints prevent a more fulsome assessment. The correction of some statistical problems led the Bureau of Labor Statistics to reduce the average monthly payroll gain for the year through March 2024 from a hot 243,000 to a still-healthy 175,000.

Unlike inflation, the Fed does not have a target unemployment rate, with a less distinct goal of “maximum employment.” Even if the figures and targets are imprecise, the labor market is unmistakably cooler today than it was a year ago. The challenge for the Fed will be to see these trends reach a steady state around the current readings. Chair Powell stated clearly in his Jackson Hole comments: “We do not seek or welcome further cooling in labor market conditions.” Easier policy may help bring back demand and support more investment that creates jobs, but there is no need to rush.

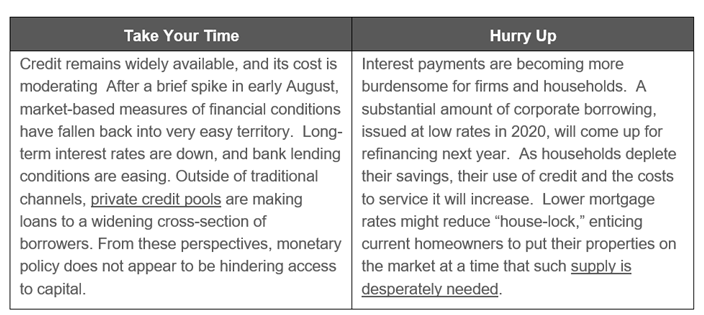

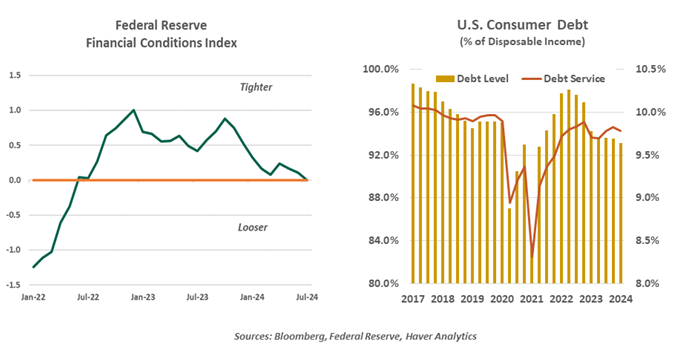

Financial Conditions

We’ve been watching closely for signs of credit distress across the economy, but nothing stands out. Commercial real estate loans bear watching, but may not be as threatening as some fear. Household finances for the lower deciles of the income distribution are not as comfortable as they were two years ago, but aggregate debt ratios remain in comfortable ranges.

The financial system had a wobble at the beginning of August, but righted itself quickly. Happily, there hasn’t been a recurrence of the banking stress of early last year.

The Federal Reserve has reduced its balance sheet by almost $2 trillion without attracting much notice. Levels of liquidity in markets are no longer abundant, but they are still ample. The pace of quantitative tightening has been reduced, to avoid the potential for a policy mistake.

Our View

The Federal Reserve has been accused of being behind the curve on several occasions this year. But results have justified their patient stance. Despite that history, some are pressing for a 50 basis point cut next week.

We don’t think that a move of that magnitude is warranted. Instead, we expect a cut of 25 basis points to be accompanied by guidance that more of the same are on the way. Our latest forecast calls for a steady string of quarter-point reductions until rates get close to their neutral level (which we think is somewhere just north of 3%). The decision will be driven by the data, not the election.

A large opening gambit could be interpreted as a signal that the Fed is panicking or acted too late, which could add to volatility and dent investor confidence. The Federal Open Market Committee (FOMC) will communicate that it remains data dependent, and the policy path could be recalibrated if incoming information warrants.

The next meeting will include a quarterly Summary of Economic Projections (SEP), including the “dot plot” of rate expectations. In the June SEP, FOMC members coalesced around a pace of reducing by a percentage point per year, implying a cut of 25 basis points at every other meeting. We expect the September SEP will show a faster pace of easing, and a greater degree of dispersion.

Longer term, we expect the Fed to steer overnight interest rates towards their “neutral” level, which we think is just over 3%. Getting there will require cuts totaling more than 2%. Sticking to a cadence of a quarter-point per meeting will reach that objective late next summer.

The easing cycle ahead of us has no close precedent. Central banks typically reduce rates when they need to support the economy through some sort of stress event. Cutting rates to secure a soft landing will create unique challenges for both deciding and communicating changes to policy.

Uncertainty surrounding the outlook has increased, and the Fed will need to adapt if needed. As Wooden famously said, “Failing to prepare is preparing to fail.”

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All