Alternative Diversifiers: Rethinking Diversification in Investment Portfolios

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive summary:

- The stock-bond correlation was neutral-to-negative for most periods between 2000 and 2021, meaning that bonds typically retained their value or appreciated when stocks sold off and vice versa. This relationship flipped to positive in 2022 and has stayed that way since, with stock and bond prices rising and falling in tandem. For investors, this means that since 2022, an allocation to bonds has not provided a diversification benefit to equities.

- A combination of select alternative diversifier strategies, including cross-asset trend and long-volatility, has demonstrated stable diversification characteristics for equity risk. As such, they can be complementary to the fixed income allocation in a traditional portfolio and can improve risk management at the total portfolio level. Specifically, a mix of cross-asset trend and long-volatility strategies may generate positive returns during equity declines—even in periods when bonds lose value in tandem with equities.

In 2021 the stock-bond correlation flipped to positive after remaining negative for a majority of the preceding 20 years. This came as a surprise to some investors who had been lulled into complacency, believing that their bond allocation could reliably provide downside management in any risk off event and serve as the primary risk stabilizer in their portfolios. For the last three years, equity and bonds have been losing and gaining value in tandem; bonds have not been helping with drawdown reduction. This has made investors question the robustness of their portfolios in a scenario where the stock-bond correlation remains positive and elevated for an extended period. A portfolio of alternative diversifier strategies, including long volatility and cross-asset trend, can complement duration as a stabilizer during periods of equity drawdowns. Such a portfolio can be especially useful in scenarios where the stock-bond correlation is positive.

In this article, we explore how the stock-bond correlation has behaved through history and if the recent positive correlation in stocks and bonds was an aberration. We then illustrate the impact that the stock-bond correlation can have on an investment portfolio, and discuss a solution using a combination of alternative diversifier strategies that can improve portfolio performance during periods of heighted equity volatility. In this article we discuss:

- Equity-bond correlations through history and the impact of changing correlations on portfolio expectations

- Alternative diversifier strategies as a source of downside management

- How alternative diversifier strategies can act as a complement to duration and have historically improved portfolio outcomes

Changing equity-bond correlation and its impact on portfolio expectations

The macroeconomic environment significantly impacts stock-bond correlations. Researchers1 have found trend inflation2 and correlation between economic growth and inflation as being the key drivers3 of stock-bond correlations. Higher levels of long-term trend inflation can lead to higher inflation uncertainty and an increase in the stock-bond correlations.

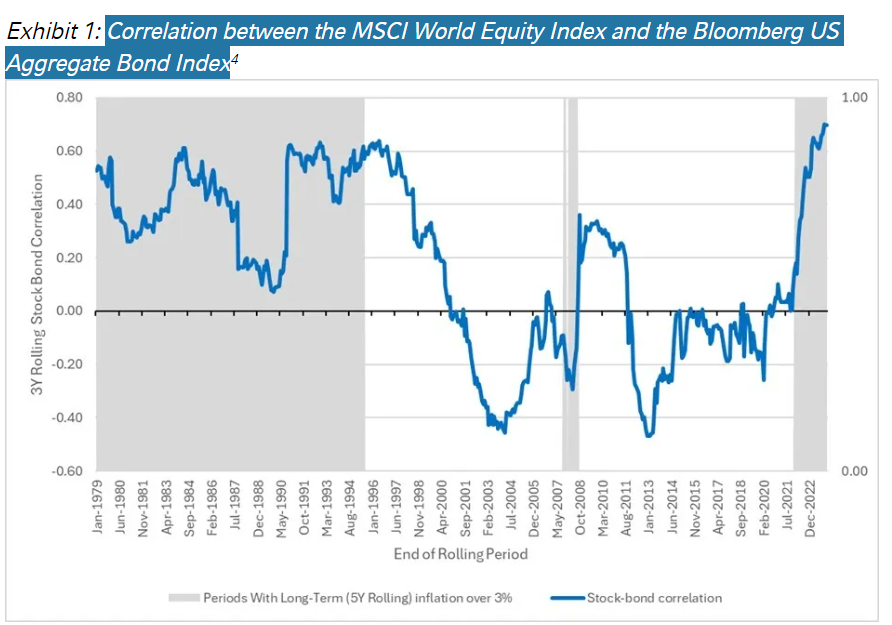

In Exhibit 1 below, we show the equity-bond correlation over the last 45 years. For 20 years through the 1980s and 1990s, when the 5-year rolling inflation rate was higher than 3%, the equity-bond correlation was consistently positive. By the end of the 1990s, the Fed’s success in controlling inflation, combined with the impacts of increased globalization, demographic changes and technological advancements helped reduce inflation to around a 2% level. Starting around 2001, the correlation dipped into negative territory, meaning that bond investments typically retained their value or produced gains when stocks sold off. This condition remained in effect until after 2020, when a COVID-led inflation shock turned the stock-bond correlation positive. This history suggests that the correlation between stocks and bonds is highly variable, and that a condition of positive or negative correlation can persist for decades.

Given the uncertainty inherent in predicting future macroeconomic environments, forecasting stock-bond correlations over a strategic horizon can be highly uncertain. An investor who believes that the U.S. Federal Reserve (Fed) will be able to get inflation close to its target 2% level, and consequently reduce macroeconomic uncertainty, would likely forecast the stock-bond correlation to turn negative or move closer to zero. Another investor who believes that a combination of deglobalization, climate risk, greenflation and other factors would lead to inflation remaining elevated and uncertain could reasonably expect the stock-bond correlations to remain positive and elevated.

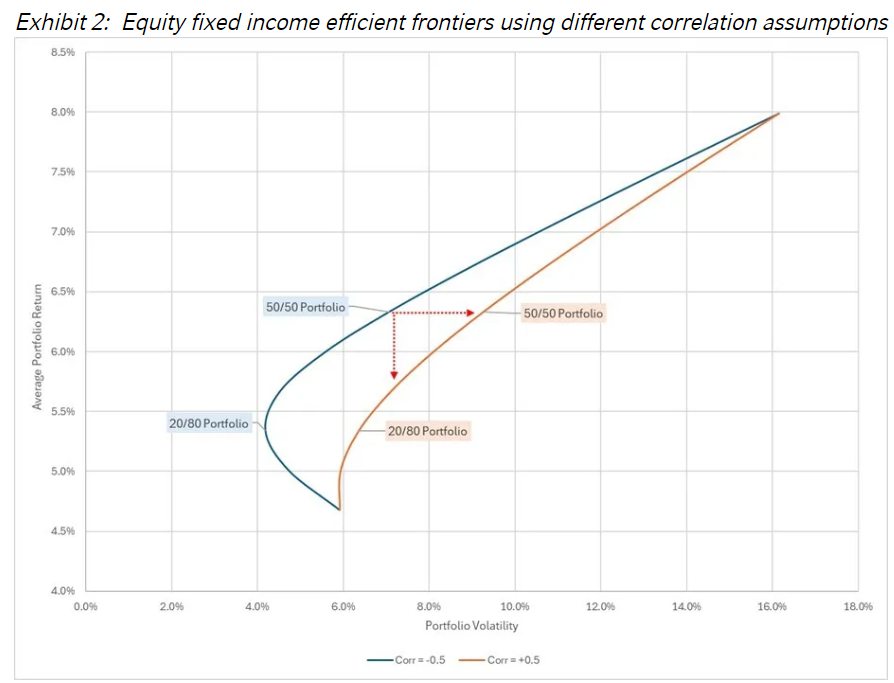

Whether the stock-bond correlation turns negative or remains positive can have a significant impact on portfolio expectations and force an investor to make difficult decisions. To demonstrate this impact, we constructed portfolios containing two asset classes—global equity and core bonds. We plotted two efficient frontiers for different mixes by varying only the stock-bond correlation (Exhibit 2)5.

Investors who forecast the stock-bond correlation to be -0.5 expect their forward-looking return and risk levels to be in-line with the dark blue frontier. A hypothetical investor who allocates to a 50/50 portfolio, based on an expectation of -0.5 equity-bond correlations, expects a portfolio return of ~6.3% and annualized volatility of ~7%. However, if the expected stock-bond correlation was +0.5 instead, the expectations would move to the orange frontier, resulting in a portfolio volatility of ~9.5%.

To account for the fact that the equity-bond correlation may remain positive, the investor is faced with a difficult choice. If the portfolio allocation was unchanged to maintain return expectations, a potential increase in portfolio volatility to ~9.5% would need to be accepted. If the investor decided that they did not want to potentially increase its volatility beyond initial expectations, they would need to de-risk their portfolio to 20% equity and accept a lower expected return of ~5.7%.

Alternative diversifiers can help with downside risk management

Investors who want to limit the impact of stock-bond correlation uncertainty on portfolio outcomes need to look at other options that can complement fixed income and help with robust downside management. One option for investors is to include an allocation to alternative diversifier strategies such as active long volatility and cross-asset trend. These strategies are expected to exhibit a negative equity beta when equities decline and are not expected to be impacted by changes in the stock-bond correlation. We find that allocating to these strategies can help reduce total portfolio drawdown risk and the reliance on bonds for drawdown protection without introducing illiquidity6 into investment portfolios.

-

Active long-volatility strategies: Long volatility strategies serve as a reliable hedge for mitigating portfolio drawdowns during downturns in equity markets. For example, an investor seeking drawdown protection can systematically buy a defensive option that becomes valuable when the underlying equity index falls below a specified price. The option pay-off is agnostic of what causes the equity index to fall. Therefore, unlike duration, the payoff is not dependent on inflation regimes or business cycles. However, the higher certainty of protection comes at a cost that can at times be exorbitantly high. Active long-volatility strategies can help significantly reduce the cost of protection by using active processes to modulate exposures to derivative instruments, including equity index options and VIX futures, in a way that maximizes portfolio protection while minimizing costs (including time decay or negative carry). Using pattern-recognition and other conditional processes, these active long-volatility strategies lie somewhat dormant when volatility is low, and will increase exposure when the probability of a market crisis increases. In this way, portfolio protection increases for active long-vol strategies as market risk increases.

- Cross-asset trend strategies: Cross-asset trend strategies can play a crucial role in creating defensiveness in a portfolio by systematically capturing both upward and downward price movements across various asset classes. These strategies use a variety of medium-to-long-term trend algorithms to initiate long or short positions across equity markets, fixed income, commodities and currencies. By adjusting positions in response to market trends—buying assets that show positive price changes and shorting those with negative price changes—these strategies can generate a positive return in both up and down markets.7 During unexpected inflation shocks, when stocks and bonds struggle, trend-following strategies can enhance portfolio defense by going long on commodities, which typically benefit from inflation. This diversification helps mitigate portfolio losses when stocks and bonds are positively correlated and are both generating negative returns. Historically, trend strategies have performed well in market dislocations, such as during the Global Financial Crisis when they profited by shorting crude oil and gold and by being long U.S. dollar and the Japanese yen.

While both active long volatility and cross-asset trend can provide defensive properties in equity down-markets, they are not exposed to the same risk factors7 and have properties that make them complementary allocations.

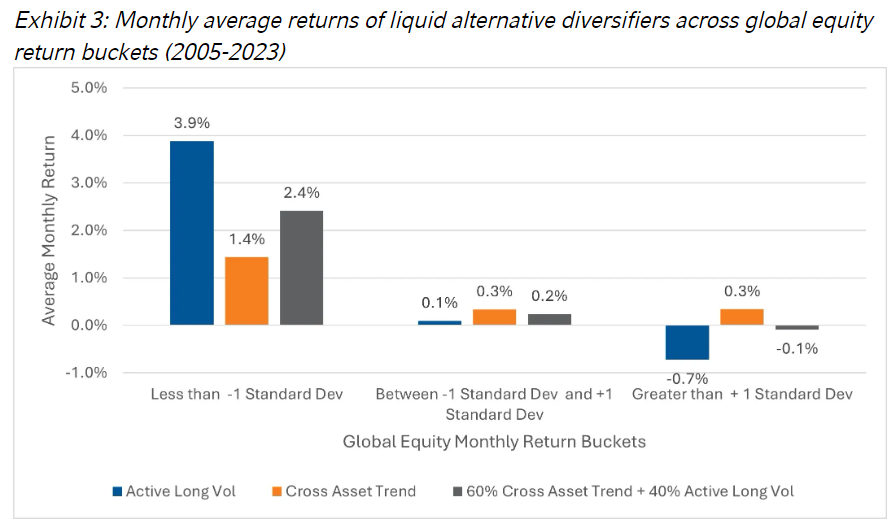

The protection from active long volatility comes at a cost of a return drag in equity up-markets that cross-asset trend can help offset. Active long volatility has historically generated negative returns8when equity markets posted large positive returns, while cross-asset trend has generated positive returns in the same environments. In Exhibit 3 below, we analyze the monthly performance of active long volatility and cross-asset trend9 from 2005-2023, and we divide the data into three groups based on global equity returns being above, below or within a +/-1 standard deviation of its history. We observe strong returns, on average, for both the active long volatility and cross-asset trend strategies in weak equity markets. However, their performances in equity-up markets was different. In strong equity markets, active long-volatility managers generated negative returns whereas cross-asset trend generated modestly positive returns. When combined at 60% cross-asset trend and 40% active long-volatility, the solution provided strong positive returns in poor equity markets and at the same time avoided significant losses in strong equity markets.

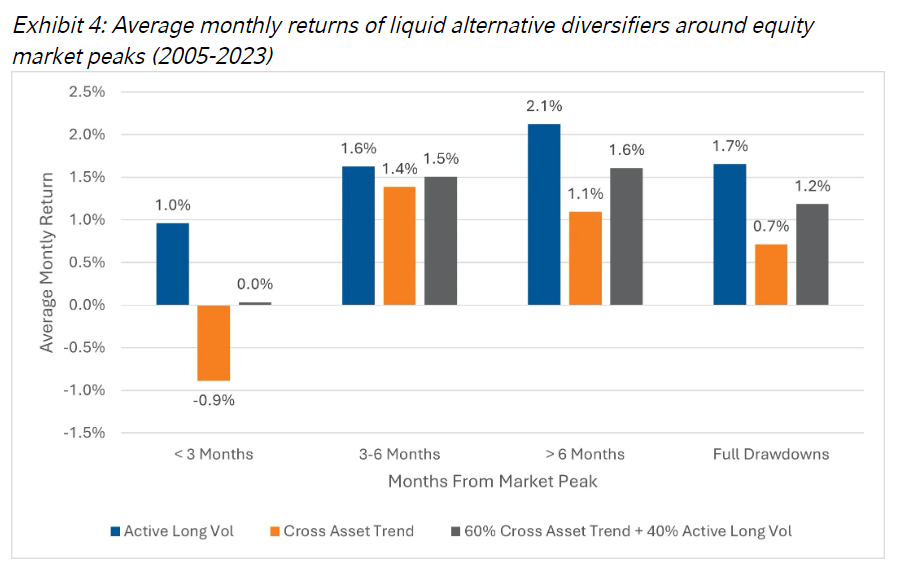

Similarly, active long volatility also helps offset some inherent weaknesses in cross-asset trend strategies. Cross-asset trend is susceptible to drawdowns around market peaks. A long run-up in equity markets can lead to cross-asset trend being long pro-cyclical assets. As such, when there is a sharp drawdown in equity around market peaks, cross-asset trend fails to protect the portfolio in the months that immediately follow. As the length of the drawdown increases, cross-asset trend adjusts its positioning and starts generating gains. The contractual nature of the long volatility positions makes it an ideal defensive allocation for sharp and sudden drawdowns around market peaks, and this helps balance out any potential loss of defensiveness from trend strategies. Exhibit 4 shows the average performance of active long volatility and cross-asset trend in peak-to-trough drawdowns as a function of months from market peak. A mix of 40% active long-vol and 60% cross-asset trend strategies was able to overcome the negative return drag from cross-asset trend around market peaks while providing protection in peak-to- trough drawdowns.

Alternative diversifiers in a balanced portfolio

By including an allocation to active long-volatility and cross-asset trend, we can reduce the reliance on fixed income for drawdown reduction. Importantly, these alternative diversifiers can provide defense in periods when bonds become positively correlated with equity and both equities and bonds experience losses at the same time.

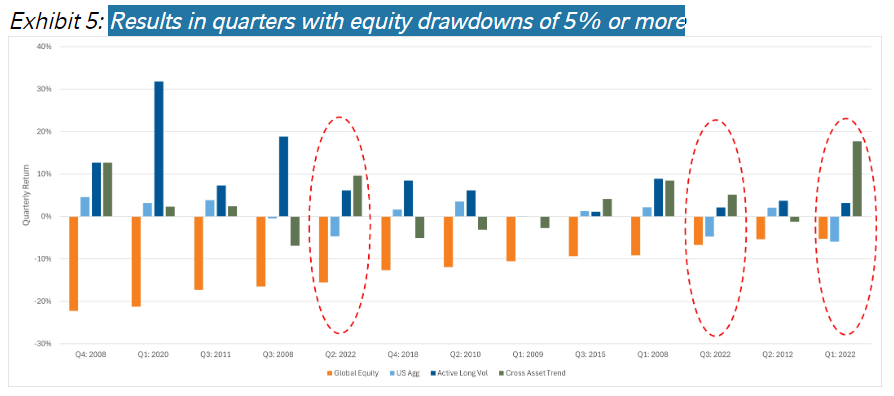

Exhibit 5 shows quarterly periods between 2005-2023 when global equities fell by more than 5%. We show the quarterly performance results for global equities, core fixed income, active long volatility and cross-asset trend.10 In most quarters when equity markets were down, core fixed income and active long volatility and cross asset trend strategies produced positive returns. However, active long volatility and cross-asset trend also produced positive returns in three quarters in 2022 when both equities and core fixed income experienced losses (represented by the three highlighted periods below).

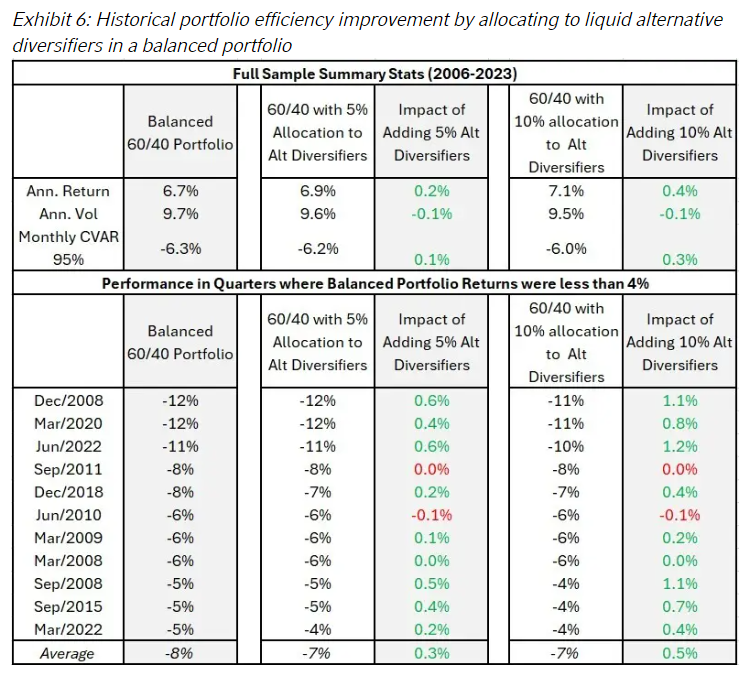

Historically, adding alternative diversifiers like active long volatility and cross-asset trend would have helped reduce portfolio drawdowns while also improving portfolio returns. We show this in Exhibit 6 by comparing the historical performance of three portfolios from 2005-2023. The first portfolio is a balanced 60/40 portfolio that allocates 60% of its capital to U.S. large cap equity and the remaining balance of 40% to U.S. aggregate fixed income. The second portfolio incrementally allocates 5% capital to a mix of 40% active long volatility and 60% cross-asset trend. We assume leverage11 12 is available in the second portfolio, i.e., despite allocating 5% to alternative diversifiers, the equity beta, duration and credit exposure of the second portfolio is the same as the first. The third portfolio is the same as the second but allocates 10% capital to alternative diversifiers instead of 5%. The two portfolios with the 5% and 10% allocation to alternative diversifiers provide us a comparison of impact at different allocation sizes. The actual size of the allocation to alt diversifiers in an investor’s portfolio would vary based on the unique investment objectives and constraints that an investor is exposed to.

We note that portfolio 2 and 3, which include allocations to alternative diversifiers, generated 20-40 bps of annualized excess return when compared to the balanced 60/40 portfolio. Adding liquid alternative diversifiers to the balanced portfolio also helped reduce portfolio volatility and conditional Value at Risk (CVAR). It is in the worst performing quarters of the balanced portfolio where the additional allocation to liquid alternative diversifiers shines, helping to reduce drawdowns by 30bps and 50bps on average when a 5% and 10% allocation to alternative diversifiers was made, which is disproportionately larger than what the volatility and monthly CVAR reduction would suggest.

Concluding thoughts

For most of the past 25 years, bonds have provided strong diversification to equities, yet 2022 reminded us that that is not always the case. In periods of heightened inflation and macroeconomic uncertainty, including the 1970s and the current period since 2022, equities and bonds have had a positive correlation. A positive stock-bond correlation can expose investors to heightened portfolio drawdown risks. Investors can build portfolios that are more prepared for changing stock-bond correlations by not solely relying on bonds for drawdown management. Alternative diversifiers such as long volatility and cross-asset trend can act as complementary allocations to fixed income in an investment portfolio, help with risk management, and act as portfolio ballasts when bonds fail to deliver the expected diversification.

1 Molenaar et al. (2024), Wu et al. (2023), Brixton et al (2023), Czasonis et al (2021)

2 Or the uncertainty in inflation. The Friedman-Ball hypothesis states that increases in inflation should occur in conjunction with higher inflation uncertainty (Ball 1992).

3 Other drivers include long run real rates, macroeconomic and growth uncertainty etc.

4 Rolling three-year correlation of monthly returns. Inflation analyzed on a rolling five-year horizon

5 Assumes the return and volatility of the two asset classes are unchanged and equal to Russell Investments’ capital market assumptions.

6 An investor should expect monthly or quarterly liquidity with no gates. The absence of any potential liquidity restrictions is a significant differentiator from other strategies that may offer monthly or quarterly liquidity but allow for the ability to restrict access to that liquidity.

7 Trend strategies have historically delivered the highest average returns in both the worst and best market conditions (van Dooijeweert, 2022), i.e. their return pattern also resembles a "convexity smile".

8 Albeit the negative returns were only a fraction of systematic passive long volatility strategies.

9 Throughout this paper, all analysis of active long volatility is based on the Eurekahedge Long Volatility Hedging Index, a sample of actively managed volatility strategies and any analysis of cross-asset trend is based on the SocGen Trend Index.

10 Global equities is MSCI ACWI Index, Core fixed income is Bloomberg Barclays US Aggregate, Long Volatility is the Eureka Hedge Long Volatility Hedge Fund Index and Trend is SocGen Trend Index.

11 An investor can judiciously allocate to equity futures to free up capital to fund an allocation to alternative diversifiers.

12 The general conclusions drawdown by comparing these three portfolios is invariant to the availability of leverage. Our analysis shows that smaller allocations to alternative diversifiers show benefits at the total portfolio level even if leverage wasn’t available.

References

Molenaar, Roderick, Edouard Sénéchal, Laurens Swinkels, and Zhenping Wang. "Empirical Evidence on the Stock–Bond Correlation." Financial Analysts Journal (2024): 1-20.

Ball, L. (1992) “Why does high inflation raise inflation uncertainty?” Journal of Monetary Economics 29(3), 371–388.

Wu, Boyu, Kevin J. DiCiurcio, Beatrice Yeo, and Qian Wang. "Forecasting US Equity and Bond Correlation—A Machine Learning Approach." Journal of Financial Data Science 4, no. 1 (2022).

Czasonis, Megan, Mark Kritzman, and David Turkington. "The Stock-Bond Correlation." Journal of Portfolio Management 47, no. 3 (2021): 67-76.

Brixton, Alfie, Jordan Brooks, Pete Hecht, Antti Ilmanen, Thomas Maloney, and Nicholas McQuinn. "A Changing Stock-Bond Correlation: Drivers and Implications." Journal of Portfolio Management 49, no. 4 (2023).

Capital Fund Management (2018) The Convexity of Trend Following, Hedge Fund Journal, April 2018

Kolanovic, Marko and Wei, Zhen (2015): Momentum Strategies Across Asset Classes. JP Morgan Systematic Cross-Asset Strategy, 15 April 2015

van Dooijeweert, Peter (2022) Creating Portfolio Convexity: Trend Versus Options, Man Institute research note, November 2022

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits