In Shakespeare’s “Hamlet,” a father gives his son the following advice as the younger heads off to college:

Neither a borrower nor a lender be,

Because loan oft loses both itself and friend

And borrowing dulls the edge of husbandry.

Husbandry, in this context, refers to the control and judicious use of resources.

In America, responsibility for financial husbandry was vested by our founders in the U.S. Congress. Unfortunately, successive editions of the institution have indulged in borrowing that is unparalleled. This year’s candidates for high office are promoting policies that could make matters even worse. Unfortunately, it appears that fiscal responsibility will remain an oxymoron in the United States.

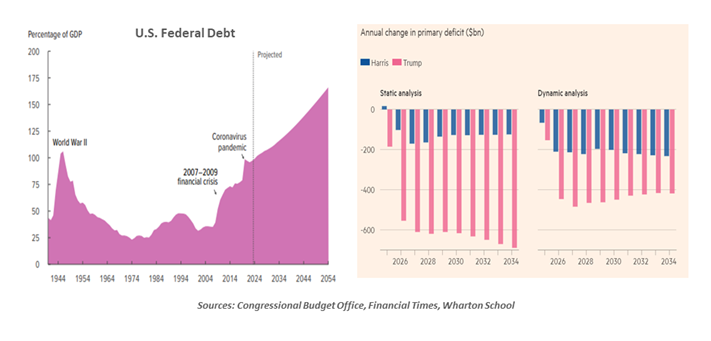

It has been hard for Congress to focus on long-term fiscal policy because the basic task of keeping government open has proven more difficult than it should be. As they battle over continuing resolutions and the debt ceiling, the national debt just keeps on increasing. We now owe more than 100% of our of gross domestic product for the first time in almost 80 years. Projections suggest that level could almost double by the middle of this century. Our essay on how we got into this mess can be found here.

Unsurprisingly, Vice President Harris and former President Trump have been reluctant to consider austerity. Instead, each has offered a menu of proposals that are politically appealing but fiscally worrisome. Third-party projections show that both party platforms will likely add significantly to the national debt.

Another “fiscal cliff” looms in 2025.

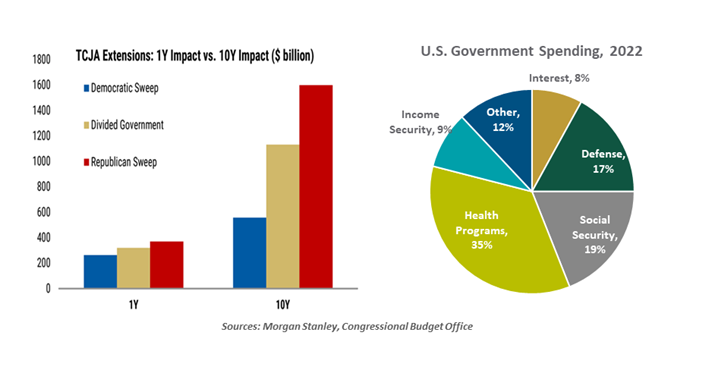

On the revenue side of the ledger, the foremost issue to be addressed next year is the expiration of most individual tax policies within the 2017 Tax Cuts and Jobs Act (TCJA). Among them are:

- Increases in standard deductions for taxpayers and reductions in personal exemptions

- The lowering of the top marginal individual tax rate from 39.6% to 37%

- Caps on the deduction for state and local taxes

- Increased thresholds for the alternative minimum tax (AMT)

- The doubling of the estate tax exemption

These kinds of “cliffs” have become more common in recent decades, as major fiscal bills passed under a reconciliation procedure cannot increase the deficit beyond a ten-year window. (This is known as the “Byrd rule” after the Senator that championed it.) Early sunsets help limit projected costs, but they are often extended to avoid creating a sudden drag on the economy.

While sustaining the TCJA provisions would be very costly from a budgetary perspective, neither side is anxious to let all of them go. Vice President Harris has proposed sustaining relief for taxpayers earning less than $400,000, offsetting the revenue loss with higher taxes on wealthier households. She has also proposed increasing corporate income taxes; such a step might prompt companies to shift profits overseas. Efforts to enact a global minimum corporate tax have stalled.

Former President Trump has promised to make all of the TCJA favors permanent. On top of that, he has proposed additional reductions in individual and corporate taxes and ending the taxation of Social Security benefits, gratuities and overtime pay. No tax revenue offsets have been recommended; the Republican platform is hoping their policies will generate incremental growth that will broaden the tax base and reduce any loss of tax revenue.

With regard to spending, the main initiative for Vice President Harris is a reinforcement of the Child Tax Credit. The benefit was doubled under the TCJA and temporarily increased in 2021 to offer support during the pandemic. Benefits will revert to their pre-2017 levels of $1,000 per child next year unless extended by Congress. The nominal cost of enhancements to the program is estimated to be $1.35 trillion over ten years, although some of this would be offset by tax revenue generated when households spend the money.

Former President Trump seeks to reinforce defense capabilities and border security. He proposes to pay for them by halting some funding for energy transition authorized under the Inflation Reduction Act (IRA), which would save $650 billion over 10 years.

Claims that tax cuts and spending programs will pay for themselves should be viewed skeptically.

Proponents of federal programs offer that spending generates economic activity and tax revenue. They add that addressing needs now can head off higher costs later.

But as we discussed in our article on budget math, the notion that tax cuts and spending programs will pay for themselves should be viewed cautiously. Projections rely on what are known as “fiscal multipliers,” which gauge the effects that taxes and spending programs have on economic activity. Different forecasters can have very different views of how large these multipliers are.

Federal spending cannot be contained without placing a foot on one of the third rails of American politics. About 85% of government outlays go to defense, Social Security, medical programs and interest. In an uncertain world, military spending does not appear to be a candidate for cuts. Social Security provides important retirement support for many Americans, and will need to be sustained. Economizing on health care will be difficult, given the nation’s demographics and the complexity with which care is delivered. We’ll have more on this latter topic in a few weeks.

Setting a course for improved fiscal health will be challenging. Political parochialism had been the enemy of progress; the two-year election cycle for Representatives (which is effectively one year for districts where primary elections decide the outcomes) is mismatched with the long horizons associated with tax and spending policies.

I share the worry expressed by many of our clients about the scale of the national debt. Unfortunately, it does not appear that the election outcome will provide any comfort on this front. I would urge members of the new Congress to remember their responsibility for husbandry, and to their own selves be true.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Northern Trust

Read more commentaries by Northern Trust