Taking Stock: Q4 2024 Equity Market Outlook

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways

The economy is not the stock market. And that’s good news. Summer market volatility tested investor conviction, but fundamentals prevailed and stocks quickly rebounded. As Q4 begins, we see:

- Fed and election uncertainty fueling volatility

- Generally positive stock reaction to rate cuts

- Greater opportunity in large vs. both mega and small caps

Q3 volatility was at least partly rooted in concerns over a slowing economy and whether the Fed was behind the curve in addressing it. We believe it had little to do with the fundamentals underlying the stock market, and this is an important distinction.

Markets are an anticipatory mechanism and attempt to predict recessions, with historically mixed results. When the economy is in a slowdown, markets can struggle to discern a midcycle slowdown from a recession ― stoking volatility.

While the economy has struggled to recalibrate post-COVID, spiraling into a series of “mini rolling recessions” ― first in technology, then in housing ― we find that the stock market, and the companies that comprise it, have managed to adapt to what we see as a return to more “normal” conditions. This resumption of normalcy also means more volatility, which we believe can be a boon for skilled stock pickers.

The two sides of volatility

Recent bouts of market volatility have served as reminders that sentiment can move markets, yet stock fundamentals prevail in the end. Sometimes that realization comes faster than others. This illustrates the importance of active selection and knowing (deeply) what you own, which can provide conviction when markets are on edge.

Q4 brings some key issues for investors to contemplate, which could further stoke market turbulence. While volatility gets a bad rap, it’s important to remember that it entails ups as well as downs ― and that context and circumstances are critical variables. When it comes to inevitable market angst, consider that:

1. Volatility can be healthy. Market resets can provide opportunities for investors to establish or increase exposure to stocks in which they have high conviction ― and at a discounted price. This is particularly true in cases where volatility is driven by sentiment or technical factors (such as extended/crowded positioning or light trading as is common in summer months) rather than fundamentals (like company earnings growth and financial fortitude).

2. Volatility is normal. The period of moderation following the Global Financial Crisis (GFC) was unusual for many reasons ― muted volatility among them. The VIX historically has experienced more dramatic gyrations than was the case post-GFC, particularly the very subdued 2012-2019. We see a return to a more normal environment where the VIX may experience more pronounced spikes, driven by such factors as the Fed, geopolitical tensions and a general proliferation of information and social media dissemination that can arguably make investors more anxious and markets less efficient.

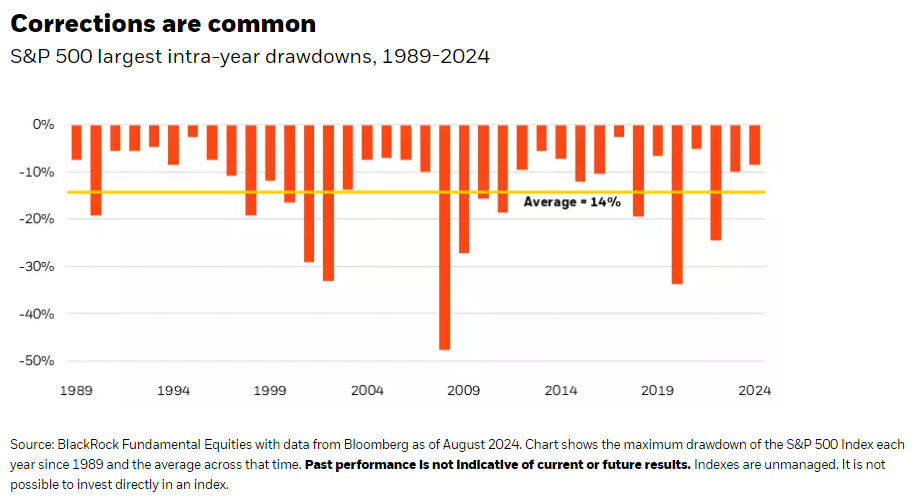

3. Market corrections are not uncommon. Corrections of 10% or more have happened in 20 of the last 35 years, with the average drawdown in that timeframe at 14%. And yet the S&P 500 returned an average 11% per year (more than 4,000% on a cumulative basis) in that time. Investors who stay the course through bouts of volatility can be rewarded ― sometimes quickly as was the case this August.

4. Volatility good for return? Data back to 1990 also suggests that higher volatility has produced higher short-term returns. Our analysis finds that muted VIX levels of 12 and below have resulted in S&P 500 returns of roughly 5% six months later. This compares to six-month returns of 16% when the VIX touches 29 or higher. The summer VIX spike, where levels hit a high of 65, quickly normalized. If historical precedent holds, moments like these could present attractive buying opportunities with potential for outsized short-term returns.

Equities and elections

Among the potential volatility-inducing moments in Q4 is one that has been anticipated all year: the Presidential election.

While history shows that the winning candidate or party has little long-term bearing on market returns, it is also interesting to note that markets do tend to have a visceral reaction (either positive or negative) on election outcomes. We looked at market performance in the first month after prior Presidential elections and then the 11 months following to see if the initial reaction to the result was the one that held in the following year. In five of seven elections since 1996, it was not.

The key takeaway: More evidence that elections may have short-term market impact but that policy regime changes and political machinations have little sway over longer-run stock performance.

Equities and an easing Fed

Also likely to influence market sentiment in Q4 are Federal Reserve rhetoric and rate cuts. Equity markets generally perform well on Fed easing, particularly when rate cuts are not accompanied by a recession.

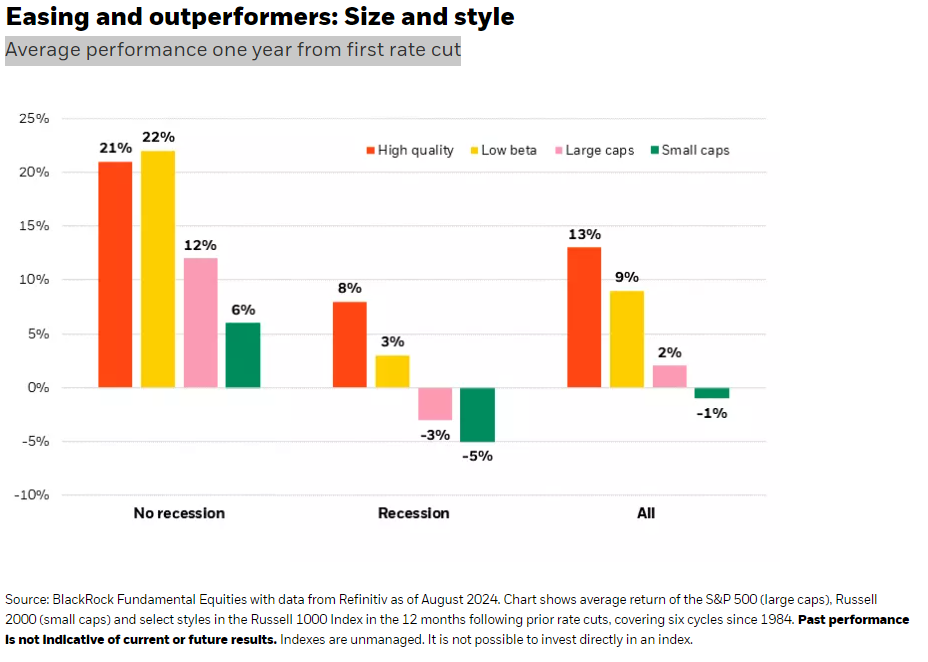

While the outcome for stocks can look different in an environment of recessionary rate cuts, history does reveal some patterns: Large caps generally lead small caps and high quality and low beta tend to outperform in the year after the onset of cutting, with or without a recession, as shown below. The pattern holds two and three years after the first cut, though value stocks also join the “winners” in these time periods.

Dissecting the sector outlook

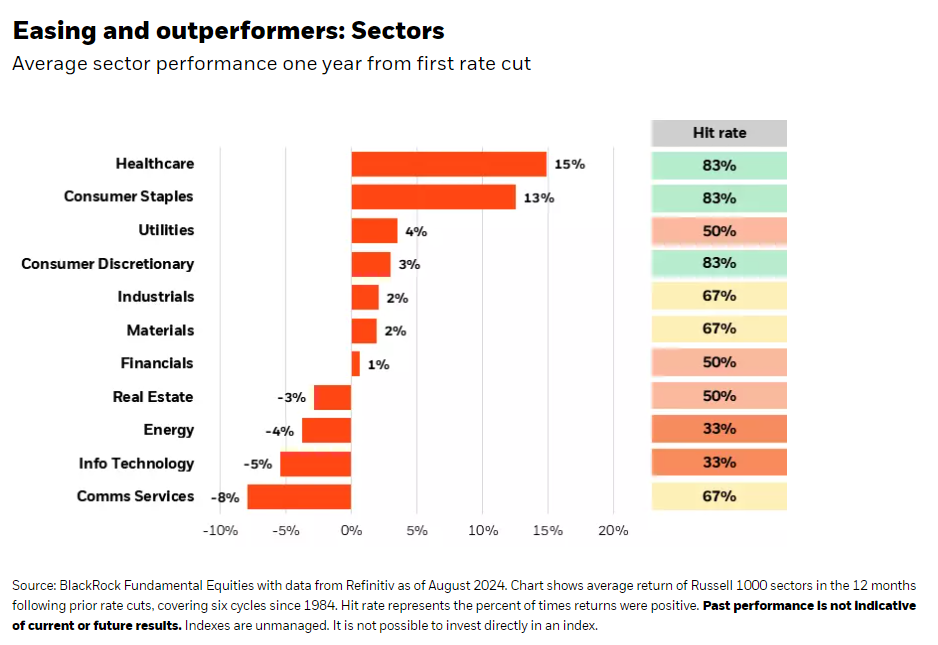

From a sector perspective, healthcare and consumer staples have historically emerged as top performers in the year following the first Fed rate cut of a cycle, as shown in the chart below. Their record of positive return (the “hit rate”) is also well above average. Extending that analysis out to two and three years shows these two sectors still lead but cyclicals, particularly financials, start to improve.

No surprise, cyclicals become more interesting as the cycle evolves and the economy approaches recovery mode. In general, recessions more often follow the start of rate cuts, with economic conditions improving as the easing cycle advances.

This time … similarities and differences

Our review of data back to 1979 shows that healthcare is also a relative outperformer over the long term. While every cycle is different, we maintain our conviction in the healthcare sector given strong secular tailwinds, such as aging populations and rising health needs, alongside growth potential powered by innovation.

Our analysis of stock dispersion within sectors over the past 20 years shows that healthcare was among three sectors (discretionary and tech being the others) that exhibited above-average difference between the best- and worst-performing stocks. This suggests potential for attractive stock picking in a sector that typically performs well in the environment we are entering.

The outlook for staples in this cycle is more nuanced. We find the sector to be well priced after being left behind in the 2023-2024 market upturn and attractive on a one-year horizon. Yet its future may not be as robust as in past cutting regimes.

On balance, the growth rate of staples has been in decline since the 1980s when dual-income families were coming into vogue and embracing the convenience of packaged foods. With that story mostly penetrated, the catalysts for significant staples growth are not what they once were.Another variable at play: the potential impact that GLP-1 diabetes and weight loss drugs may have on the demand for some packaged food items.

Meanwhile, the technology sector, a laggard in past rate-cutting regimes, looks far better positioned in this cycle. We find many areas of tech have become more staples-like, while AI also serves as a powerful secular propellent for growth in the sector.

Final reflection: The power of patience

Since 1974, the stock market has endured a presidential resignation, the collapse of the “Nifty Fifty” blue-chip stocks, raging stagflation, the 1987 stock market crash, the rise and bursting of the dot-com bubble, three wars in the Middle East, the GFC and COVID-19 pandemic. And over those 50 years, $5,000 invested in the S&P 500 Index would have grown to be worth $1.3 million today.*

Volatility is inevitable. Still, for long-term investors, patience is a virtue.

* Analysis is based on total returns with dividends reinvested from Jan. 1, 1974, to Aug. 5, 2024, with data from Bloomberg.

Other analyses cited within are conducted by BlackRock Fundamental Equities with data sourced from Bloomberg and Refinitiv.

This material is provided for educational purposes only and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of September 2024, and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. The material was prepared without regard to specific objectives, financial situation or needs of any investor.

This material may contain “forward-looking” information that is not purely historical in nature. Such information may include, among other things, projections, forecasts, estimates of yields or returns, and proposed or expected portfolio composition. Moreover, where certain historical performance information of other investment vehicles or composite accounts managed by BlackRock, Inc. and/or its subsidiaries (together, “BlackRock”) has been included in this material, such performance information is presented by way of example only. No representation is made that the performance presented will be achieved, or that every assumption made in achieving, calculating or presenting either the forward-looking information or the historical performance information herein has been considered or stated in preparing this material. Any changes to assumptions that may have been made in preparing this material could have a material impact on the investment returns that are presented herein by way of example.

Investing involves risk. Equities may decline in value due to both real and perceived general market, economic, and industry conditions. Diversification does not ensure profits or protect against loss.

You should consider the investment objectives, risks, charges and expenses of any BlackRock mutual fund carefully before investing. The prospectus and, if available, the summary prospectus contain this and other information about the fund and are available, along with information on other BlackRock funds, by calling 800-882-0052 or from your financial professional. The prospectus should be read carefully before investing.

Prepared by BlackRock Investments, LLC, member FINRA.

Not FDIC Insured • May Lose Value • No Bank Guarantee

©2024 BlackRock, Inc or its affiliates. All rights reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0924U/S-3885882

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits