In the ever-evolving landscape of financial services, wealth advisors are always seeking new avenues for growth and client engagement. One promising area they may consider is the 401(k) market. With the rapid expansion of 401(k) plan formation, advisors who pivot toward this sector can unlock significant business development potential.

By the numbers: The growth of 401(k) plans

The 401(k) market has seen remarkable growth over the past decade. As of the first quarter of 2024, Americans had $7.8 trillion invested in 401(k) plans.1 This growth is not just in assets but also in the number of plans and participants. For example, the number of 401(k) plans has increased significantly, with 55.8% of plans having less than $1 million in assets, and 48.8% of all 401(k) assets concentrated in plans with more than $1 billion in assets.

Moreover, participation rates are encouraging. In 2019, 43% of all workers participated in a defined contribution plan such as a 401(k). This participation is even higher among workers with automatic enrollment, reaching up to 89% for those earning between $30,000 and $49,999.2

The metaphor: Mining for gold in the 401(k) market

Imagine the 401(k) market as a vast gold mine. The surface has been scratched, but the richest veins of opportunity lie deeper, waiting to be discovered. Wealth advisors are like skilled miners, equipped with the tools and expertise to unearth these additional revenue opportunities. By tapping into the 401(k) market, advisors can not only diversify their service offerings but also build long-term relationships with clients looking for comprehensive retirement planning solutions.

Why pursue the 401(k)market?

The 401(k) market may offer wealth advisors a compelling avenue for growth and client engagement. With increasing demand driven by legislative changes and a heightened focus on retirement planning, advisors have a unique opportunity to expand their services. Specializing in 401(k) plans can diversify revenue streams, enhance client loyalty and help advisors stand out in a competitive market. To effectively tap into this market, advisors should consider several key factors.

-

Growing demand: As more companies offer 401(k) plans, the demand for expert advice on plan design, management and optimization is increasing. State auto-IRA mandates and the SECURE Acts of 2019 and 2022 are helping to fuel this demand.

-

Client retention: Offering 401(k) advisory services can enhance client loyalty by providing a holistic approach to financial planning. Most IRA rollovers go to an advisor the worker knew prior to the rollover triggering event.

-

Revenue streams: Advisors can generate additional revenue through plan management, participant education programs and investment advisory services. One of the most popular participant education opportunities is financial wellness consulting. Financial wellness engagement can help advisors identify and consolidate retirement assets from prior employment. Many individuals accumulate multiple 401(k) accounts due to frequent job changes. According to the Bureau of Labor Statistics, the average American holds 12 jobs over their lifetime, often resulting in stranded retirement assets.3

-

Market Differentiation: Specializing in 401(k) plans can set advisors apart from competitors who may not offer these services. Approximately 35% of wealth advisors’ clients in the United States are small business owners. Concentrating some time on 401(k) plans may give advisers an advantage when mining for small/medium business-owner clients.4

Consider potential growth

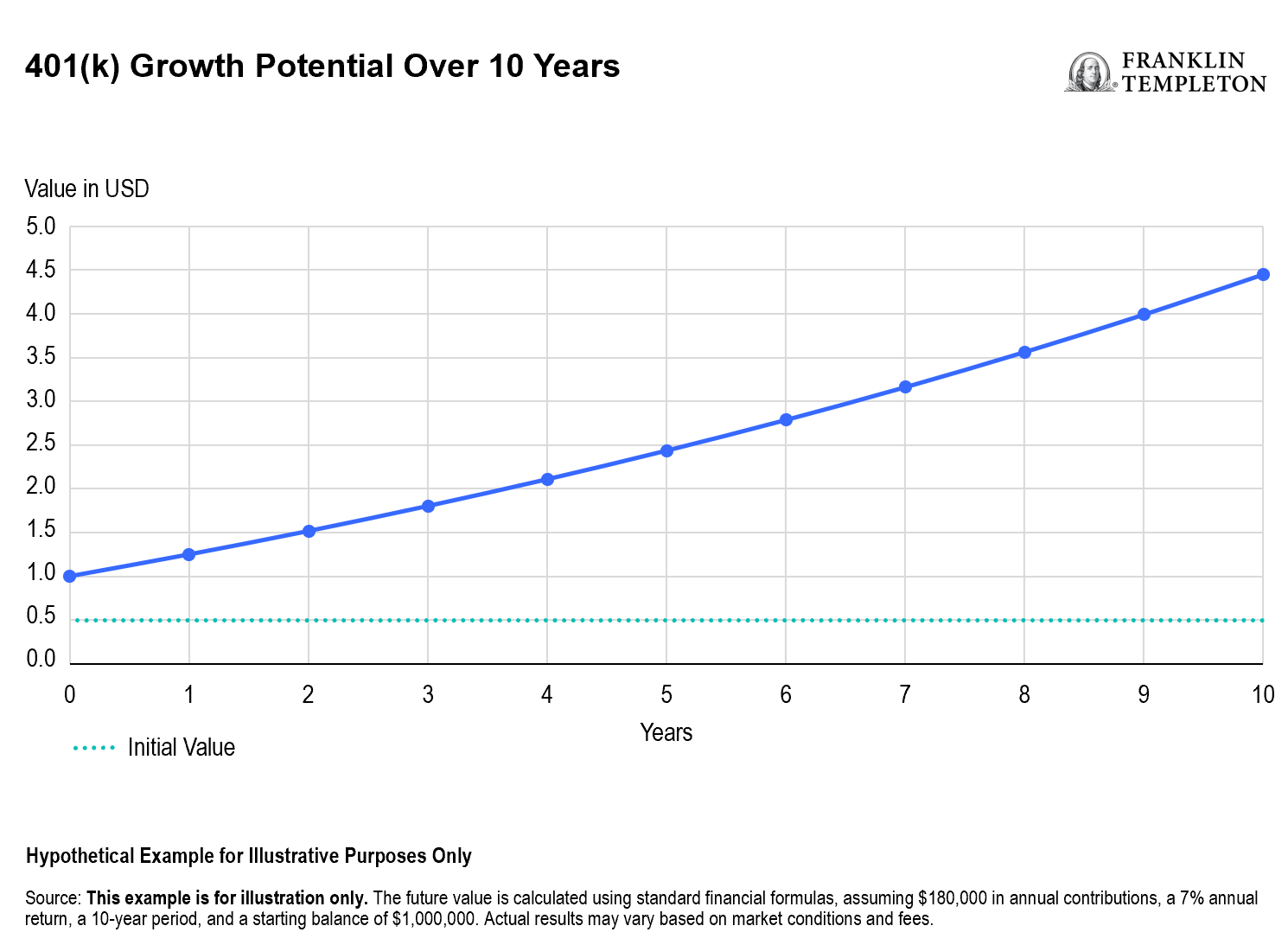

To estimate the asset growth potential of a $1 million 401(k) plan over the next 10 years, there are several factors to consider, including annual contributions, employer match and expected rate of return.

Consistent contributions drive the outcome

Under these assumptions, the 401(k) plan could grow to approximately $4.45 million over 10 years. This demonstrates the significant growth potential of a well-managed 401(k) plan, that features consistent contributions and a reasonable rate of return.

Strategies for advisors

To successfully navigate the 401(k) market, wealth advisors may want to consider the following strategies.

-

Education and certification: Obtain certifications such as the Certified 401(k) Professional (C(k)P) to show expertise. Education can be found with resources like Napa.net and 401kspecialist.com as well as attending retirement industry conferences.

-

Partnerships: Collaborate with record-keepers and third-party administrators to offer comprehensive solutions. The growth in plan formation has ushered in the creation of turnkey structured solutions where third-party partners can take on many aspects of plan creation and plan management.

-

Technology integration: Utilize advanced financial planning software to provide personalized advice and track plan performance. The capabilities created by record keepers and the fintech community continue to grow as demand for personalization increases.

-

Client education: Conduct workshops and seminars to educate clients about the benefits and intricacies of 401(k) plans. Since retirement plans, along with health care, are often considered one of the most popular benefits at most companies, the demand for this education is strong.

The bottom line

The 401(k) market represents a treasure trove of opportunities for wealth advisors. By tapping into this sector, advisors can unlock new revenue streams, enhance client relationships and position themselves as leaders in the industry. As the 401(k) market continues to grow, I believe those who seize this opportunity may be rewarded well.

-

Next steps for advisors to consider: Build better workplace solutions: Guide employers and employees toward financial well-being with Franklin Templeton’s innovative offerings. Learn more by clicking here.

-

Explore flexible retirement plans: Discover our range of flexible solutions for small and mid-sized businesses by visiting Retirement Plans Made Easy.

-

Connect with your partners: Get in touch with your Franklin Templeton Retirement team. Contact information is available here.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realized. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S.: Franklin Resources, Inc. and its subsidiaries offer investment management services through multiple investment advisers registered with the SEC. Franklin Distributors, LLC and Putnam Retail Management LP, members FINRA/SIPC, are Franklin Templeton broker/dealers, which provide registered representative services. Franklin Templeton, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com.

Please visit www.franklinresources.com to be directed to your local Franklin Templeton website.

Copyright © 2024 Franklin Templeton. All rights reserved.

1.Source: Investment Company Institute, Quarterly Retirement Market Data. June 13, 2024.

2. Source: “100 Must-Know Statistics About 401(k) plans.” Morningstar. September 4, 2020.

3. Source: “Number of Jobs, Labor Market Experience, and Earnings Growth: Results from a National Longitudinal Survey.” Bureau of Labor Statistics. August 2021.

4.Source: “Five ways for financial advisors to prospect 401(k) clients.” Ascensus, 2024.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent market outlooks.

© Franklin Templeton

Read more commentaries by Franklin Templeton