Options-based ETFs are one of the fastest-growing categories in the market today, with product proliferation and adoption rising quickly. As more products and assets enter this category, we are asked: Can the options market support so many of these strategies?

The short answer is yes. To illustrate that, consider the experience of the capital markets team transacting in the suite of defined outcome and 100% Buffer ETFs from Innovator ETFs.

This past week, we witnessed a rare occasion. An entire lineup of options-based strategies—the Innovator Defined Outcome and 100% Buffer Protection series—reset on a single day. On Oct. 1, monthly, quarterly, six-, 12-, and 24-month buffer and outcome strategies—30 in total—reset. This kicked off another outcome period with new caps and buffers.

It was a busy day of options trading for Innovator.

According to the firm, more than 320,000 options contracts were traded on that day on behalf of these ETFs. Some $2.5 billion in assets rolled on that reset day. These funds also picked up more than $320 million in fresh creations on Oct. 1, with massive volume across the funds. It all went down without a hitch.

Innovator ETFs’ big reset day is a great illustrative anecdote of the deep liquidity of options markets, especially in contracts-tied indexes such as the S&P 500. It’s also a testament to the tradability, efficiency, and nimbleness of the ETF structure itself, which can exchange investor hands and keep supply of shares elastic with ease.

Consider that Innovator, while a pioneer in Buffer ETF investing (commanding about a 51% market share in that category), isn’t the only one in the space. The firm was not the only name transacting in options contracts on Oct. 1. Several other providers navigated the same markets in pursuit of downside protection with some upside capture through options-based strategies resetting that day.

The market for options-based ETFs may be growing. However, the underlying market supports it with the liquidity these ETFs need to deliver on their value proposition. Is that news? Not really. But it’s still a good exercise to stop and take notice when things go according to plan. In this case, these ETFs are doing what they set out to do. They are transacting successfully and seamlessly to deliver investors the expected access.

That is good news. The demand for Buffer-type investing should continue to grow, according to Andrew Nelson of Innovator ETFs. He notes that assets have been coming into Buffer and Managed Floor strategies as “advisors look to equitize cash on the sidelines with principal protection and tax alpha.”

Redeployment of cash on the sidelines has been one of the big themes for asset managers this year. Meanwhile, ETFs delivering capital protection and some capital appreciation potential in a single ticker should remain a valuable investor tool.

“There have only been four quarters since 1950 where the S&P has declined more than 20%, so you can see the safe nature in this offering,” Nelson says of Buffer ETFs. “It begins to look like traditional fixed income, but with upside tied to the equity market, with a cap that also resets.”

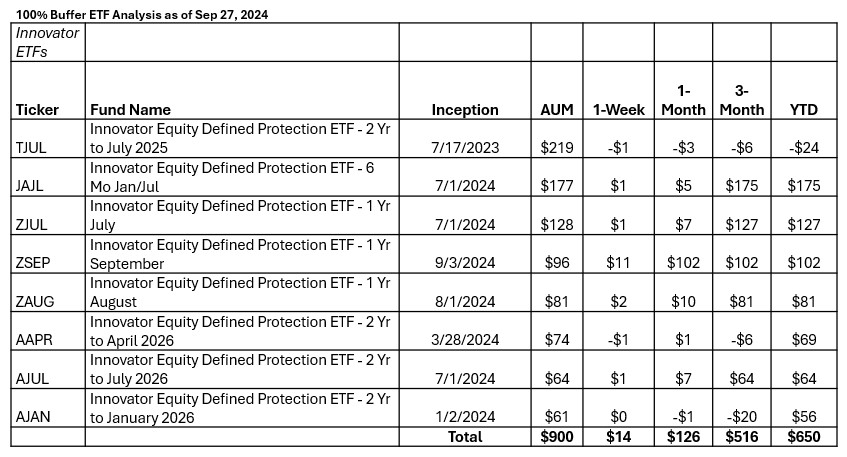

Source: Innovator ETFs

For a broad list of Buffer ETFs, start your research here.

For more news, information, and analysis, visit VettaFi | ETF Trends.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

Read more commentaries by VettaFi