Where Can Private Credit Fit in an Institutional Portfolio?

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsExecutive summary:

- Amid concentration risk in equities and fixed income, private credit investments enable institutions to better diversify across unlisted organizations, economic sectors, and regions.

- When compared to tradable fixed income, private credit has the potential to offer higher annualized income.

- Private credit investments typically provide a stable and predictable income stream.

- Increasingly, fund structures have been designed to enable greater degrees of liquidity in private credit.

Where can private credit fit in an institutional portfolio?

With storm clouds forming above equities and fixed income markets, is now the right time for institutions to grab their private credit labeled umbrella?

After having been on a formidable run, the Magnificent Seven stocks, and equities more broadly, appear to be showing signs of stumbling, with greater scrutiny of their sky-high valuations. Moreover, with interest rates expected to fall further by the end of the year, fixed income instruments are also on course to lose some of their attractiveness.

Amid this change, investors and institutions alike should be wary of the concentration risk of being overly exposed to these asset classes and consider if their risk allocations can be better utilized elsewhere—like in private credit.

Diversification

Private credit has a number of traits that can make it a valuable component of a portfolio leaning on equity and fixed income markets. For instance, private credit investments enable institutions to better diversify their portfolio across unlisted organizations, economic sectors, and geographic regions. Private credit involves lending to a variety of borrowers that are often smaller, mid-sized companies. These companies frequently operate in sectors or niches that are underrepresented in public markets—and with debt that may be less correlated to broader risk assets due to stricter underwriting standards, even in good times. Having this lower drawdown profile could prove vital for alpha preservation if markets cool.

Illiquidity premium

When compared to tradable fixed income, private credit has the potential to offer higher annualized income. The illiquidity and complexity of private loans often command a premium, resulting in higher coupons as well as additional sources of income beyond just the coupon. This helps to compensate for the higher origination efforts required in private lending just to gain the exposure, and the illiquidity risk investors assume after making such loans.

For institutions such as sovereign wealth funds, charities, and pension plans, which might have tighter liquidity budgets, the enhanced returns from private credit can significantly improve overall portfolio performance, even with shorter maturities.

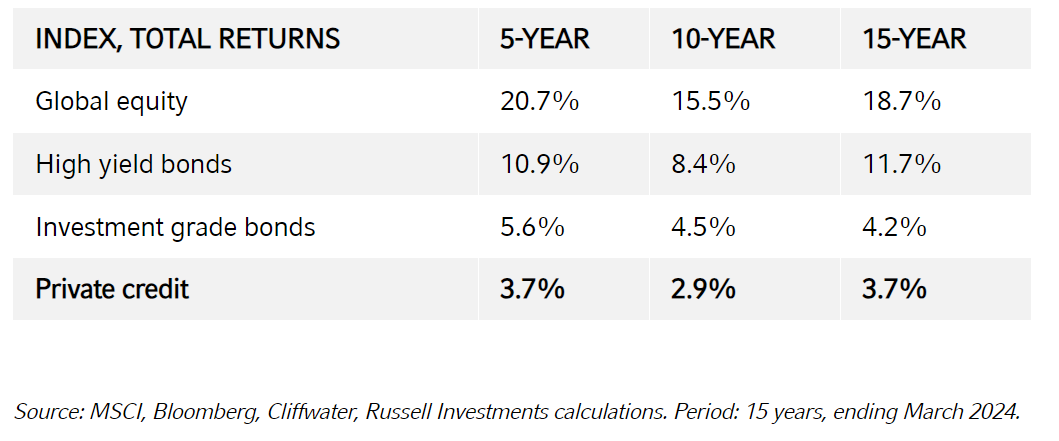

Historical performance shows that private debt performs in line with equities over a medium to long term. This confirms the capabilities of this asset class to replace equities, without expecting to compromise on performance.

Lower volatility

Private credit investments typically provide a stable and predictable income stream through regular interest payments, various fees charged to borrowers, and timely loan repayments. This is especially valuable in a low-interest-rate environment where traditional income-generating assets may underperform. Many private loans also include prepayment penalties, ensuring that investors receive adequate compensation if borrowers repay their loans early.

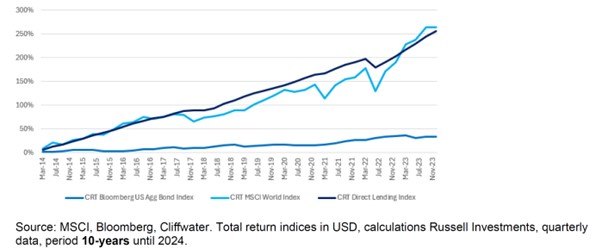

Importantly, the volatility of private credit is relatively low compared to public equities. This is due to structural protections in private loans that manage downside risks and the fact that these investments are not subject to daily mark-to-market pricing. Historically, unlevered private credit has exhibited annualized volatility around 3.7%, making it an attractive option for institutions seeking to reduce portfolio volatility while maintaining returns.

Volatility - Quarterly Total Returns

Improved liquidity

Traditionally, institutions have been wary of increasing their allocations to private credit due its perceived illiquidity. These concerns have not been entirely ill-founded; over the past decade private credit funds have typically been closed-ended, leaving little wriggle room for investors to alter their exposures. However, increasingly fund structures have been designed to enable greater degrees of liquidity. For instance, Russell Investments now offers private credit in an evergreen format with quarterly cash pay liquidity, subject to certain limitations, that significantly reduces the operational burden of investing in private credit while also giving investors more optionality on how and when they might want to reduce exposure in the future.

The bottom line

Private credit represents a potential strategic benefit to many institutional portfolios. It offers diversification, reduced drawdown risk, steady income streams, and robust risk management. For financial institutions and pension plans looking to navigate the concentration risk in Magnificent Seven equities and declining yields in fixed income, we believe private credit provides an attractive option that helps to create a more balanced and resilient investment portfolio—with more investor friendly ways to access the market today than ever before.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All