Macro Thoughts: Goldilocks Pixie Dust

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsThought to ponder ...

“The only true currency in this bankrupt world is what you share with someone else when you are uncool.”

Almost Famous (the movie)

Lester Bangs played by Philip Seymour Hoffman

The View from 30,000 feet

Putting it all together

- The market continues to trend higher on Goldilocks [pixie] dust. The latest installments last week included:

- Revisions to past GDP indicating even better growth than was had been reported

- Forecasts via GDPNow models of even better growth for the current quarter than was already expected

- The Fed’s preferred measure for inflation coming even softer than expected

- China firing a bazooka at their growth problems caused by the Balance Sheet crisis in the country circa 2008/2009 GFC style setting off an Emerging Markets rally

- Potential signs of a bottoming in the commercial real estate market in the U.S. via Amazon’s get your butt back to work order combined with lower rates making refinancing a feasible possibility as some point the foreseeable future

- Lower rates potentially setting off a refi boom in the S. over the next year for nearly 25% of homeowners that may support consumption and answer the question of what comes next to prop up the consumer after government transfer payments are gone

- That’s a lot of good new to digest, but before you get too comfortable / excited / complacent (take your pick), keep in mind there is an election around the corner, and depending on who gets elected and what policies are put in place after the election, the ground could shift. The election is an even race right Economist projections are that Trump policies would result in higher inflation and lower growth, which could change the trajectory of the Fed and throw a monkey wrench in the neatly crafted Goldilocks story. We need to be careful not to put too much faith in modeled projections of economist, which are rarely precise, but we also have to keep in mind that our business is to identify risks.

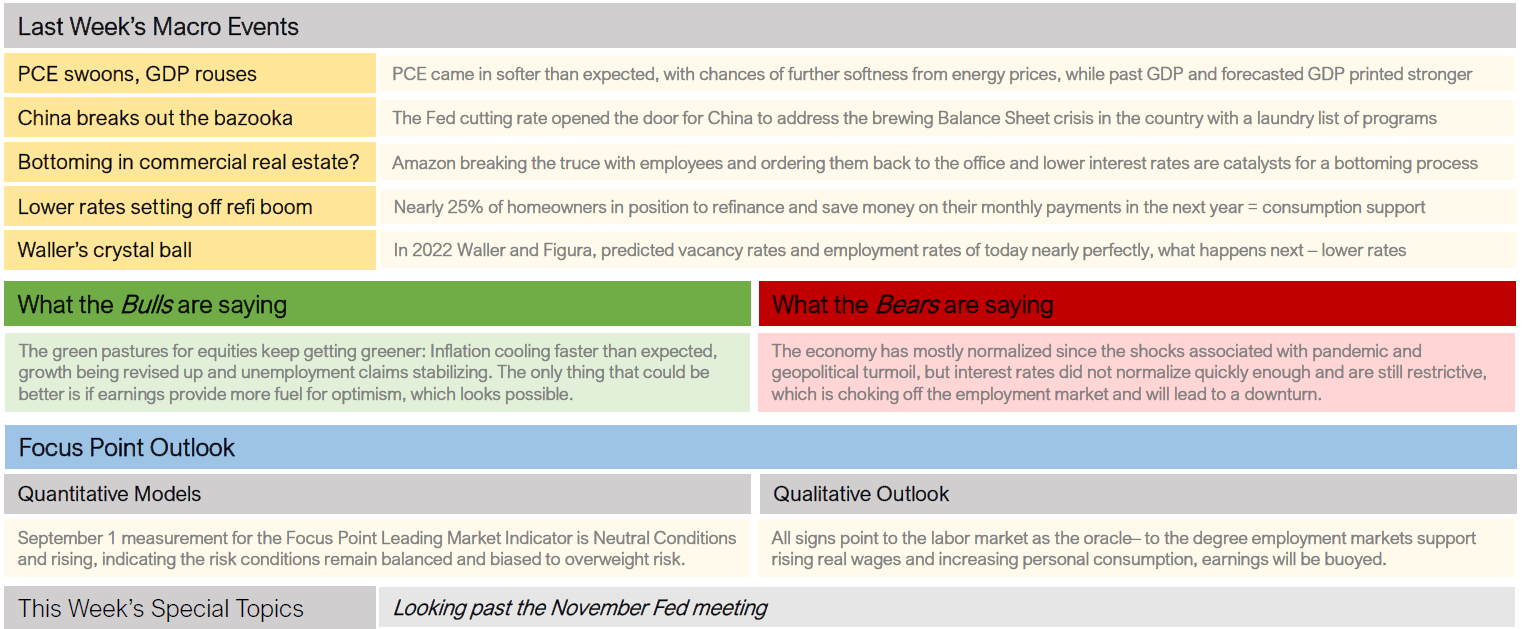

PCE Swoons, GDP Rouses

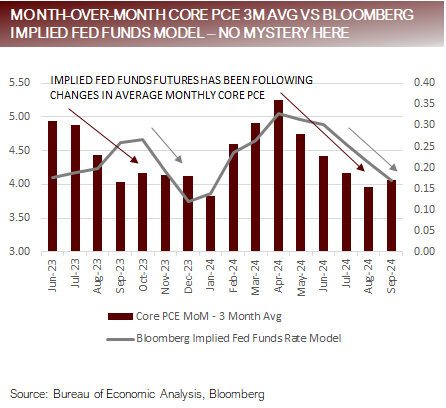

- PCE, the Fed’s preferred measurement of inflation, came in slightly below expectations on Friday, taking the headline PCE YoY measurement to 2%, and the Core PCE YoY to 2.7%.

- Core month-over-month PCE was 13%, brining the three and six month annualized rates to 1.9% and 2.6%. Importantly, the trend for monthly changes in Core PCE has provided extremely good guidance of market expectations of Fed Funds and is pointed lower.

- With WTI Oil down -7.5% in September and housing data indicating a deceleration of the rate of shelter inflation, next month’s PCE, which is the final PCE before the Fed’s next meeting, tips momentum towards another 50 bps cut at the November meeting.

- GDP received to positive shots in the arm last week:

- The latest revision of Q2 GDP growth surprised with an unexpected increase from 9% to 3.0%, with additional revisions to previous GDP revising away the two negative quarters of GDP in 2022 down to one quarter.

- The Atlanta Fed GDPNow Forecast for Q3 GDP, inched to 1%, the highest estimate of the quarter.

- Bottom Line: Lower inflation expectations and higher growth expectations are the Goldilocks cocktail the market is craving.

China breaks out the bazooka

- List of the monetary and fiscal programs enacted by the Chinese government over the last five days (it felt a little bit like the alphabet soup days of the 2008/2009 GFC days in the US):

Monetary

-

- Cut the interest rate on the 1yr medium term lending facility from 2.0% from 2.3%

- Increased lending facilities to financial institutions of $43b

- Reduced the 7-day reverse repo rate by 20 bps to 5%

- Cut the required reserve ratio (RRR) by 50 bps

- Provided guidance that they would be cutting the loan prime rate by 20 to 25 bps

- Reduced the minimum down payment for a second home from 25% to 15%

Fiscal

-

- Introduced a policy to cover 100% of the principal of local government loans from 60%

- Introduced a $114b lending facility to fund stock buybacks and institutional stock purchases

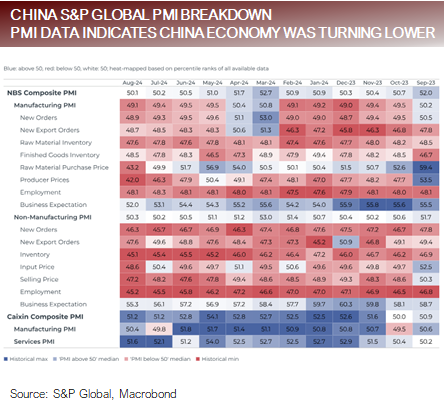

- Why now? Two As highlighted by Chinese PMIs, the economy is deteriorating in an already poor environment, and the Fed’s reduction of interest rates allows the PBOC to move with less risk to devaluing the Yuan.

Bottoming in commercial real estate?

- How will we know when commercial real estate is bottoming?

- Two things combined in a powerful one-two punch to commercial real estate over the last four years.

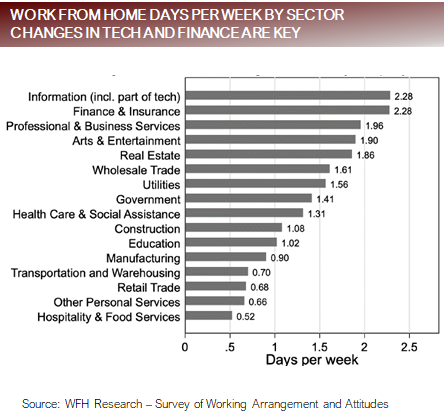

- The pandemic created a Work From Home cultural shift that lowered demand for office space.

- Lending rates, which are ultimately tied to Fund Funds, saw the largest increase since the 1980s

- In the last week and half two events have provided evidence these trends are changing.

- On September 16th, Amazon’s CEO Andy Jassy issued an order that employees need to return to the office five days a week.

- The Federal Reserve cut the Fed Funds rate by 50 bps.

- Two things combined in a powerful one-two punch to commercial real estate over the last four years.

- Bottoming is a process. Neither of these events represent an abrupt shift, but they indicate that that the tides are turning.

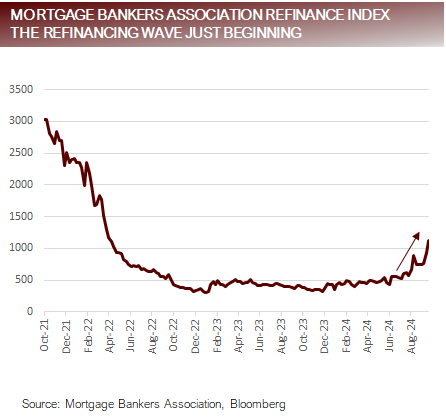

Lower rates setting off refi boom

- Mortgage rates averaged 13% last week from a high of over 8.0% eleven months ago. According to Redfin 85.7% of U.S. homeowners have a mortgage rate below 6%. Which means 14.3% have a mortgage rate above 6%. The people with rates above 6% are beginning to line up to refinance.

- To provide some perspective of how much demand for refinance there is, demand for refinances increased 175% over a demand a year ago.

- According to the Mortgage Bankers Association mortgage applications increased to their highest level since 2022 with refinance applications surging 20% last week after spiking 24% the previous week and making up 55.7% of total mortgage

- If interest rates were to fall below 5%, an estimated additional 10% of homeowners would benefit from refinancing, bringing to total pool of potential homeowners refinance to near 25% of all homeowners. This is a wave that could very realistically be crashing in 2025, and may act as a leg to prop up consumer spending in the coming year.

Waller's crystal ball

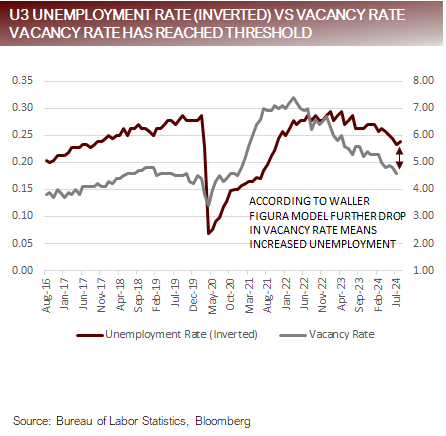

- One of the biggest questions on investors’ minds is if the Fed will continue to ease into what looks like a robust economy? Two-part answer:

- In 2022 Fed President Christopher Waller joined with Andrew Figura to write a paper attempting to quantify their expectations for the Beveridge Curve, which is a theoretical representation of the relationship between Job Openings and They argued that job openings could fall [without] a dramatic impact to unemployment, because the Vacancy Rate was extremely elevated at the time. They postulated that the Vacancy Rate could fall from 7.5% to 4.5% and Unemployment would only increase to 4.2%, which was contra to standard Beveridge Curve modeling. They turned out to be correct. The latest Vacancy Rate was 4.6%, and Unemployment is 4.2%. This has important implications because the implication is that a further decline in the Vacancy Rate may begin to have a more pronounced [affect] on the Unemployment Rate, which helps explain the Fed’s urgency.

- The second reason that the Fed will likely continue to aggressively cut rates is because simply looking at the differential between Fed Funds less Inflation as a simplified measurement of restrictiveness, the Fed has actually become more restrictive since the spring, even after figuring in the interest rate cut in September.

Looking past the November Fed meeting

- There are two inflation reports and two labor market reports between the meetings the September and November Fed meetings. The first of the inflation reports was last week, coming in softer than expected. With oil prices falling and shelter inflation cooling, we expect inflation will continue to be soft. Employment is less certain, but the hurricane will likely make the data look weak.

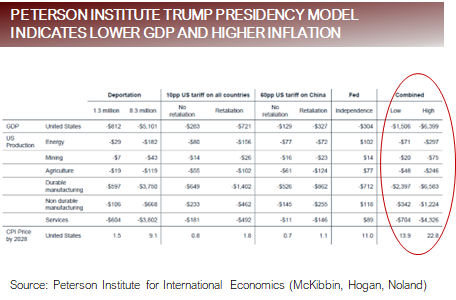

- Beyond the [U.S.] election, the picture gets murky. The Peterson Institute published a report last week forecasting the impacts of Trump’s proposed policies. Polls show the candidates for the U.S. Presidency roughly even, which would imply 50/50 odds to the Peterson Institute Model.

- Peterson Institute Model of Trump Presidency by 2028

- GDP Low -1.5t High -6.4t

- Inflation Low +13.9 High +22.8

- We should be careful assuming this model is correct or that a Trump Presidency would yield the policies he has discussed on the campaign trail, but we should be aware of the risks.

For more news, information, and strategy, visit the Innovative ETFs Channel.

DISCLOSURES AND IMPORTANT RISK INFORMATION

Performance data quoted represents past performance, which is not a guarantee of future results. No representation is made that a client will, or is likely to, achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Focus Point LMI LLC

For more information, please visit www.focuspointlmi.com or contact us at [email protected]

Copyright 2024, Focus Point LMI LLC. All rights reserved.

The text, images and other materials contained or displayed on any Focus Point LMI LLC Inc. product, service, report, e-mail or web site are proprietary to Focus Point LMI LLC Inc. and constitute valuable intellectual property and copyright. No material from any part of any Focus Point LMI LLC Inc. website may be downloaded, transmitted, broadcast, transferred, assigned, reproduced or in any other way used or otherwise disseminated in any form to any person or entity, without the explicit written consent of Focus Point LMI LLC Inc. All unauthorized reproduction or other use of material from Focus Point LMI LLC Inc. shall be deemed willful infringement(s) of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights, including but not limited to, rights of privacy. Focus Point LMI LLC Inc. expressly reserves all rights in connection with its intellectual property, including without limitation the right to block the transfer of its products and services and/or to track usage thereof, through electronic tracking technology, and all other lawful means, now known or hereafter devised. Focus Point LMI LLC Inc. reserves the right, without further notice, to pursue to the fullest extent allowed by the law any and all criminal and civil remedies for the violation of its rights.

All unauthorized use of material shall be deemed willful infringement of Focus Point LMI LLC Inc. copyright and other proprietary and intellectual property rights. While Focus Point LMI LLC will use its reasonable best efforts to provide accurate and informative Information Services to Subscriber, Focus Point LMI LLC but cannot guarantee the accuracy, relevance and/or completeness of the Information Services, or other information used in connection therewith. Focus Point LMI LLC, its affiliates, shareholders, directors, officers, and employees shall have no liability, contingent or otherwise, for any claims or damages arising in connection with (i) the use by Subscriber of the Information Services and/or (ii) any errors, omissions or inaccuracies in the Information Services. The Information Services are provided for the benefit of the Subscriber. It is not to be used or otherwise relied on by any other person. Some of the data contained in this publication may have been obtained from The Federal Reserve, Bloomberg Barclays Indices; Bloomberg Finance L.P.; CBRE Inc.; IHS Markit; MSCI Inc. Neither MSCI Inc. nor any other party involved in or related to compiling, computing or creating the MSCI Inc. data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice.

This communication reflects our analysts’ current opinions and may be updated as views or information change. Past results do not guarantee future performance. Business and market conditions, laws, regulations, and other factors affecting performance all change over time, which could change the status of the information in this publication. Using any graph, chart, formula, model, or other device to assist in making investment decisions presents many difficulties and their effectiveness has significant limitations, including that prior patterns may not repeat themselves and market participants using such devices can impact the market in a way that changes their effectiveness. Focus Point LMI LLC believes no individual graph, chart, formula, model, or other device should be used as the sole basis for any investment decision. Focus Point LMI LLC or its affiliated companies or their respective shareholders, directors, officers and/or employees, may have long or short positions in the securities discussed herein and may purchase or sell such securities without notice. Neither Focus Point LMI LLC nor the author is rendering investment, tax, or legal advice, nor offering individualized advice tailored to any specific portfolio or to any individual’s particular suitability or needs. Investors should seek professional investment, tax, legal, and accounting advice prior to making investment decisions. Focus Point LMI LLC’s publications do not constitute an offer to sell any security, nor a solicitation of an offer to buy any security. They are designed to provide information, data and analysis believed to be accurate, but they are not guaranteed and are provided “as is” without warranty of any kind, either express or implied. FOCUS POINT LMI LLC DISCLAIMS ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY, SUITABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE. Focus Point LMI LLC, its affiliates, officers, or employees, and any third-party data provider shall not have any liability for any loss sustained by anyone who has relied on the information contained in any Focus Point LMI LLC publication, and they shall not be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs) in connection with any use of the information or opinions contained Focus Point LMI LLC publications even if advised of the possibility of such damages.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All