Executive summary:

- Bond ladders were a staple of many investor portfolios until rates fell to historic lows after the 2008 Great Recession

- As rates rose in the past two years, the appeal of these laddered strategies grew

- There are a variety of ways to build a fixed-income ladder to meet a variety of investor needs

For decades, a key component of many investors’ portfolios was a fixed income ladder. It was intended to provide ballast to the more volatile equity allocation and help reduce interest-rate risk.

But things began to change in 2008 when the Great Recession forced the U.S. Federal Reserve to cut interest rates to historically low levels to stimulate the economy. Fixed income instruments that offered yield, like bonds, became less attractive. And bond ladders, which include bonds of various maturities, fell out of favor.

Things have begun to change again. Now that interest rates have returned to levels where investors can earn a reasonable yield on bonds, fixed income ladders are starting to make sense as part of a diversified portfolio.

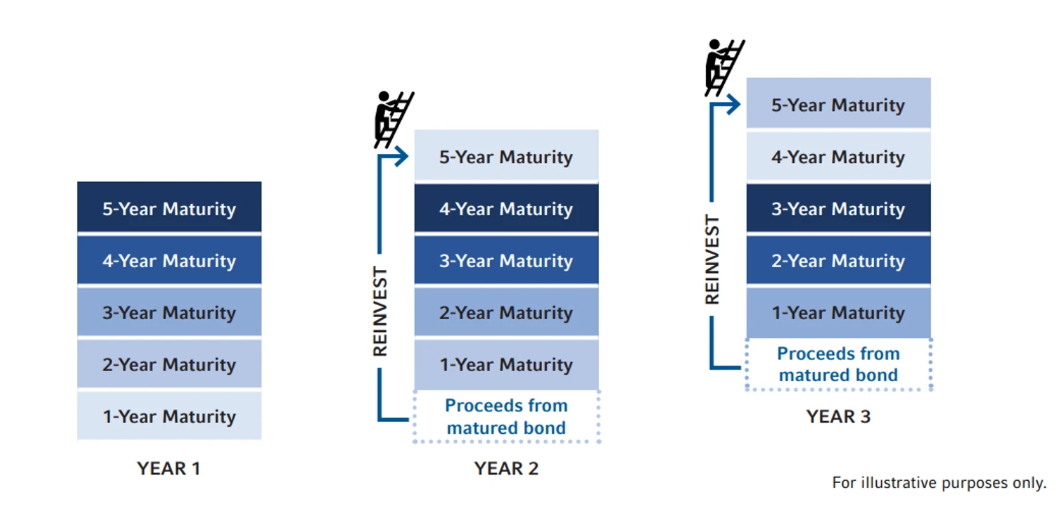

What is a fixed income ladder?

A fixed income ladder is an investment strategy with a series of fixed income securities of staggered maturities. The idea is that when the lowest rung of the ladder - the fixed-income security with the shortest term – matures, it is liquidated and replaced by a longer-term maturity. In this way the investor receives a regular income stream while hedging against any changes in interest rates as they climb the ladder.

How are bond ladders different than mutual funds and ETFs?

There are a few key differences between a bond ladder and a packaged investment like a mutual fund or Exchange Traded Fund (ETF). A bond ladder allows an investor to own the individual bonds themselves, and if they hold them to maturity, they will receive back their initial investment plus earn a predictable interest rate along the way.

Fixed income mutual funds and ETFs do not have set interest rates. Therefore, the yield and the value of the investment will fluctuate with the market. For example, if rates rise, the yield on the bond fund or ETF may increase, but the overall value of the investment may fall. Of course, the opposite thing happens if rates fall. This is a result of bond prices moving in an inverse direction to the yield.

With a bond ladder, if held to maturity, the value of the portfolio will remain the same, and the interest rate is locked in for each bond held.

What kind of bond ladders are there?

Just like you can have a wood ladder or a steel ladder, investors can build their ladders with different materials. A bond ladder can be built with Certificates of Deposit, with government bonds, corporate bonds or municipal bonds. Each has its advantages and disadvantages. For example, municipal bonds can offer tax advantages, investment-grade corporate bonds can offer potentially higher yields, while government bonds, or U.S. Treasury bonds, are backed by the guarantee of the U.S. government.

Are bond ladders suitable for everyone?

Bond ladders, mutual funds and ETFs all offer investors access to the fixed income market. Mutual funds and ETFs offer investors an opportunity to increase the value of their investment over time (if rates fall) or earn a higher yield if rates rise. Conversely, the yield on a mutual fund or ETF will fall if rates fall, and the portfolio’s value may go down if rates rise. Bond ladders hold the same value over time (If held to maturity) and the interest rate (or yield) is fixed.

A bond ladder is suitable for a portfolio if the primary focus is preservation of principal and a consistent yield. Mutual funds and ETFs also have lower investment minimums than bond ladders.

How do bond ladders fit into a portfolio?

As noted, bonds provide stability in a diversified portfolio. Bond prices rarely fluctuate in value to the same extent as equities so holding them can help smooth out returns.

Bond ladders not only provide that stability, but due to the staggered maturities, they can be a source of yield, making them a good choice for investors who need a steady stream of income.

Why incorporate a SMA for your bond ladder strategy?

Because the investor holds the bonds directly, rather than in a bond fund or ETF, they are potentially best suited in a Separately Managed Account (SMA).

SMAs allow investors to customize their portfolios to align with their individual risk profiles and goals. An investor can choose a specific type of bond ladder to fit their needs – perhaps one built with municipal bonds if they are looking for tax minimization, or one using Treasuries if they require stability. They can also choose the maturities of the bonds so that the ladder provides income for the length of time required. And because the bonds have a set interest rate, the ladder can protect the investor against the risk of rates falling from existing levels.

In conclusion, the more attractive yields offered over the past few years have prompted many investors to consider incorporating fixed income ladders into their overall investment portfolios. Maybe now is the time to have a fresh conversation with your clients about incorporating a bond ladder SMA into their fixed income strategy.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

The information, analysis and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual entity.

Personalized Managed Accounts (“PMA”) is a program of Russell Investment Management, LLC (“RIM”) and offers customized portfolio management services.

Each Personalized Separately Managed Account is a product of Russell Investment Management, LLC (”RIM”) and offered through RIM’s Personalized Managed Accounts (“PMA”) program. It represents a model portfolio provided by RIM. For active SMAs, it reflects a composite of third-party investment advisors selected by RIM. When the model is implemented, PMA is a separately managed account program of individually owned securities that can be tailored to meet investor’s investment objectives. RIM offers diversified, single or multi-asset managed accounts that can be customized to the investor’s investment objectives, circumstances and preferences, such as (but not limited to), market exposure, risk management, tax management, category and theme-based restrictions and return objectives. Excluding any allocations to pooled investment vehicles, if any, each investor’s account is managed separately from other investor accounts, allowing for a personalized experience to deliver unique investment outcomes.

The decision to use PMA in investors’ portfolios and related investment advice are provided through financial advisors and other financial intermediaries that are independent of RIM and its affiliates. Investors should consult with their financial advisor to determine which services and programs are appropriate to meet their investment objectives.

Russell Investments' ownership is composed of a majority stake held by funds managed by TA Associates Management L.P., with a significant minority stake held by funds managed by Reverence Capital Partners L.P.. Certain of Russell Investments' employees and Hamilton Lane Advisors, LLC also hold minority, non-controlling, ownership stakes.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the “FTSE RUSSELL” brand.

The Russell logo is a trademark and service mark of Russell Investments.

Copyright © 2024 Russell Investments Group, LLC. All rights reserved. This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an “as is” basis without warranty.

RIM-03508

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

© Russell Investments

Read more commentaries by Russell Investments