Executive summary:

- U.S. Treasury yields have soared in the past month, despite the beginning of the Fed rate-cutting cycle

- Q3 earnings growth projections in the U.S. and Europe have been adjusted downward

- The Bank of Canada delivered its fourth consecutive rate cut

On the latest edition of Market Week in Review, Director of Investment Strategies, Shailesh Kshatriya, unpacked the potential factors driving the sharp increase in U.S. Treasury yields. He also provided an update on third-quarter earnings season and the Bank of Canada’s (BoC) latest decision on rates.

Two potential factors pushing up Treasury yields

Kshatriya began by discussing the rapid increase in U.S. Treasury yields. He noted that the yield on the benchmark 10-year note, which stood at roughly 4.2% at market close on Oct. 24, has risen by roughly 12 basis points (bps) in the past week and approximately 55 bps since mid-September—right after the U.S. Federal Reserve (Fed) lowered borrowing costs by half a percentage point.

“With the Fed commencing rate cuts, it seems counterintuitive for yields to move in the opposite direction—and it’s tricky to pinpoint precisely what's driving them higher. However, I believe two potential contributing factors are the continued strength of U.S. economic data and markets pricing in the possibility of a wave outcome in November’s U.S. elections,” Kshatriya said.

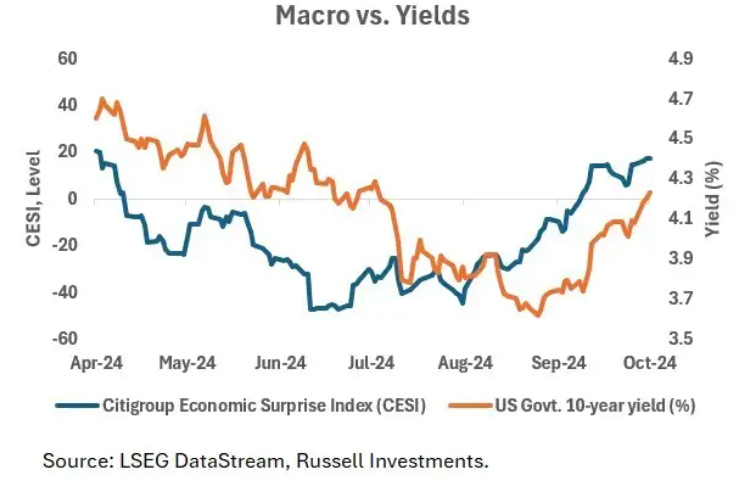

He explained that U.S. macro data over the past month has generally fared better than expected, with indications of more robust growth causing markets to reassess their outlook on Fed rates. In early September, market expectations were for three additional 25-bps cuts over the remaining two Fed meetings this year—expectations that have since been dialed down to just under two rate cuts as of late October, Kshatriya said. As evidence, he pointed to a chart that plots the stronger-than-expected U.S. economic data—as measured by Citigroup Economic Surprise Index (CESI)—against the 10-year U.S. Treasury yield. The chart shows that the rise in the CESI has roughly coincided with the rise in the 10-year yield, Kshatriya noted.

He said that the looming U.S. elections could be another factor in the spike in yields, as markets may be pricing in a higher probability of a wave election scenario, in which one political party controls the White House and both chambers of Congress. Such an outcome could be more expansionary from a fiscal perspective, leading to higher inflation and, therefore, higher yields, Kshatriya explained.

“The bottom line here is that while it’s not a precise science, a combination of solid macroeconomic data and politics likely is contributing to the increase in U.S. yields,” he stated.

Q3 earnings growth estimates lowered in the U.S. and Europe

Switching to U.S. third-quarter earnings season, which kicked off earlier in the month, Kshatriya said that so far, a third of S&P 500 companies have reported earnings for the quarter.

He noted that blended earnings-per-share (EPS) growth—which combines actual and estimated results—is tracking at around 4.3% on a year-over-year basis, which is about one percentage point lower than estimates at the start of October. However, he said that if the energy sector is excluded, earnings growth jumps to a more respectable 6.9% year-over-year rate. What’s more, approximately 79% of reporting companies have beaten their EPS estimates—an impressive statistic that is notably higher than the historical average of 67%, Kshatriya remarked.

Turning to Europe, he said that while it’s still very early days in the reporting season, the initial read is for a blended third-quarter EPS growth rate of 3.0% year-over-year. Similar to the U.S., EPS growth estimates in Europe jump to 7.6% when the energy sector is excluded, Kshatriya noted.

“The key takeaway is that while EPS growth estimates have been coming down in both regions for the third quarter, the energy sector is a factor in that downshift, with earnings growth looking respectable otherwise,” he stated.

Bank of Canada slashes rates by 50 bps

Kshatriya finished with an update on the Bank of Canada’s latest decision on rates. He said that Canada’s central bank delivered a jumbo-sized 50-bps rate cut at the conclusion of its Oct. 23 meeting, lowering its target rate from 4.25% to 3.75%. This matched consensus expectations for a big cut, Kshatriya remarked, noting that markets were pricing in over a 90% chance of a 50-bps reduction in rates.

The cut was the BoC’s fourth in a row, he said, and is largely due to a sharp decline in inflation coupled with a sluggish growth outlook. “It’s important to understand that the inflation and growth backdrop in Canada is very different from the neighboring United States,” Kshatriya said, noting that both headline and core inflation have fallen below the BoC's 2% target rate to 1.6%. Moreover, the bank’s updated projections call for an economic growth rate of roughly 1% in 2024, he said, adding that the nation’s unemployment rate has also been on the rise.

“With this backdrop, I don’t think it's surprising that the BoC feels a greater urgency to bring rates down toward neutral—that is, toward the rate that is neither stimulative nor restrictive for the Canadian economy,” Kshatriya stated, noting that the BoC’s estimation of the current neutral rate is somewhere between 2.25% and 3.25%.

Kshatriya concluded by stressing that while the bank will ultimately make decisions based on incoming data, he believes the policy rate is headed toward the lower end of the neutral range and that another jumbo-sized cut cannot be ruled out.

Disclosures

These views are subject to change at any time based upon market or other conditions and are current as of the date at the top of the page. The information, analysis, and opinions expressed herein are for general information only and are not intended to provide specific advice or recommendations for any individual or entity.

This material is not an offer, solicitation or recommendation to purchase any security.

Forecasting represents predictions of market prices and/or volume patterns utilizing varying analytical data. It is not representative of a projection of the stock market, or of any specific investment.

Nothing contained in this material is intended to constitute legal, tax, securities or investment advice, nor an opinion regarding the appropriateness of any investment. The general information contained in this publication should not be acted upon without obtaining specific legal, tax and investment advice from a licensed professional.

Please remember that all investments carry some level of risk, including the potential loss of principal invested. They do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Frank Russell Company is the owner of the Russell trademarks contained in this material and all trademark rights related to the Russell trademarks, which the members of the Russell Investments group of companies are permitted to use under license from Frank Russell Company. The members of the Russell Investments group of companies are not affiliated in any manner with Frank Russell Company or any entity operating under the "FTSE RUSSELL" brand.

The Russell logo is a trademark and service mark of Russell Investments.

This material is proprietary and may not be reproduced, transferred, or distributed in any form without prior written permission from Russell Investments. It is delivered on an "as is" basis without warranty.

CORP-12611

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Russell Investments

Read more commentaries by Russell Investments