The United States housing market has undergone significant transformations in recent decades with the aftermath of the Global Financial Crisis (GFC) and the COVID-19 pandemic leaving lasting impacts. This piece examines the current state of the housing market, the factors contributing to its challenges, and the potential solutions to address the ongoing affordability issues.

One of the most pressing issues facing the U.S. housing market is the severe shortage of homes. In the years following the GFC, the home construction industry significantly reduced its output, which led to a cumulative shortfall of millions of homes compared to historical building rates and new household formations. This underproduction created a structural imbalance between supply and demand and set the stage for the affordability challenges we see today.

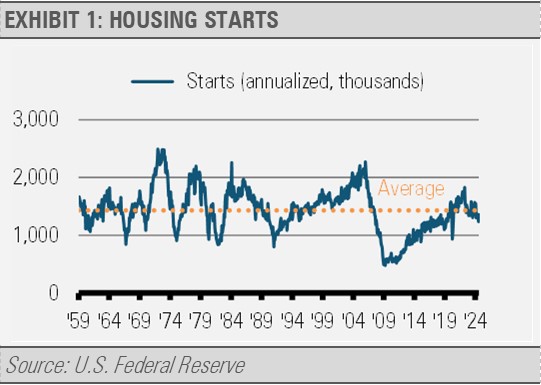

In the U.S., new home construction has averaged 1.433 million units per year since 1959. As you can see in the graph below, there have been plenty of booms and busts in housing construction over the last 65 years. These boom periods can go on for several years as depicted in the above average annual construction.

In contrast, bust periods of below average annual construction tend to be much shorter. However, we have not seen anything like the current length of the post-GFC below average annual housing starts since this dataset started in 1959.

After the overbuilding housing boom of the mid-2000s, new home construction slowed considerably. From 2007 to 2023, new housing starts averaged 1.1 million units per year compared to the long-term trend of 1.433 million units per year. In short, new housing starts were below the long-term average by an average of 333,000 per year for 17 years. Notably, while new household formation has lessened over recent decades as the population growth has slowed, the result is still a shortage of millions of homes.

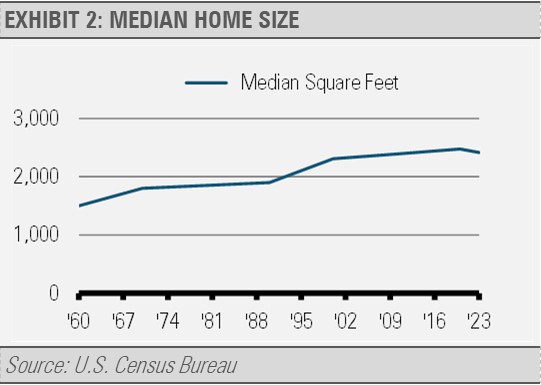

An additional, though likely secondary factor, is that the size of each house and the associated costs of construction have gone up. As we can see below, since the 1960s the median size of a new home has increased persistently. Since 1990, the median size of a new home increased from approximately 1,900 square feet to 2,400 square feet. In addition to the rising cost of materials and labor, the increase in the quantity of materials and labor required to build these larger homes has also driven costs per unit higher.

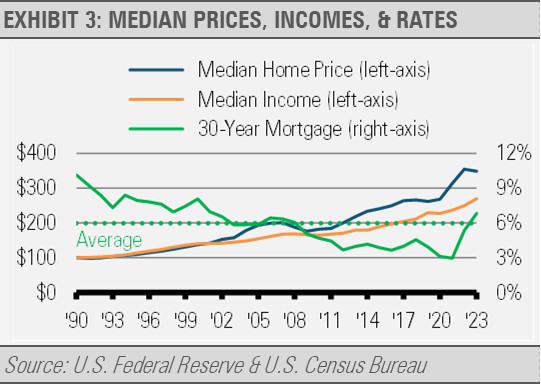

The COVID-19 pandemic acted as a catalyst to the price surge, exacerbating existing housing market tensions. As remote work became widespread and people sought more living space, demand for homes surged. This increased demand, coupled with the pre-existing housing shortage, led to a dramatic spike in home prices. The annual average growth rate of median home prices jumped from 3.46% in the pre-pandemic period (1990-2019) to an astounding 7.68% per year in the post-pandemic years (2020-2023).

While median household incomes have also grown, they have not kept pace with the rapid acceleration of home prices. Pre-pandemic (1990-2019) median household income grew at an average annual rate of 2.93%, which is slightly below the 3.46% growth rate of median home prices. However, the gap widened significantly in the post-pandemic period. From 2020 to 2023, median household income growth accelerated to 4.13% annually, but this was dwarfed by the 7.68% annual growth in median home prices.

This growing disparity between income and home price growth has led to a significant deterioration in housing affordability for many Americans. The dream of homeownership has become increasingly out of reach for a sizable portion of the population, particularly first-time buyers, and those in lower income brackets.

Interest rates also play a crucial role in housing affordability. The past few decades have seen a general trend of declining mortgage rates. Mortgage rates in the teens during the late 1970s and early 1980s declined to 10.13% in 1990 followed by a historic low of 3.11% in 2020. These lower rates helped offset rising home prices to some extent, keeping monthly payments more manageable for homebuyers.

However, as of October 2024, mortgage rates have risen to 6.72%. This return to more "normal" interest rate levels, combined with elevated home prices, has created a double whammy for affordability. Many potential buyers now face both higher purchase prices and higher borrowing costs, which further exacerbate the affordability challenges.

We can see these phenomena trend over time. As the following chart illustrates, median incomes kept pace with median home prices between 1990 and 2000. During the housing boom of the mid-2000s, incomes fell behind. With the housing bust, home prices corrected, and incomes briefly caught up. More recently, median home prices have leapt ahead once again.

In our view, the most effective long-term solution to address housing affordability is to significantly increase the supply of homes. This approach tackles the root cause of the problem: the shortage of available housing units. By encouraging more construction, we can work towards closing the gap between supply and demand, which should help alleviate price pressures over time.

Several strategies could be employed to boost construction:

-

Zoning reforms: Many areas have restrictive zoning laws that limit housing density and types. Relaxing these restrictions could allow for more diverse and abundant housing options.

-

Streamlined permitting processes: Reducing bureaucratic red tape and expediting approval processes for new construction projects could help accelerate building rates.

-

Incentives for developers: Tax breaks or other financial incentives could encourage developers to build more homes, particularly in affordable housing segments.

-

Investment in infrastructure: Improving transportation networks and other infrastructure can make previously less desirable areas more attractive for development.

-

Support for innovative construction methods: Encouraging the adoption of technologies like modular construction could help reduce building costs and time.

It's important to note that addressing the housing shortage will require a sustained, long-term effort. Even if we were to increase annual construction rates by 50% or more, it would still take years to make up for the millions of homes that are currently lacking in the market. This underscores the need for patience and persistent policy focus to achieve meaningful results.

The U.S. housing market faces significant challenges stemming from years of underproduction, exacerbated by the economic shocks of the past few years. The widening gap between home price growth and income growth, combined with the return to more normal interest rate levels, has created an affordability crisis. While there's no quick fix, a concerted effort to boost housing construction offers the most promising path forward. By addressing the fundamental supply-demand imbalance, we can work towards a more stable and accessible housing market for all Americans. However, this will require sustained commitment, innovative policies, and patience as we work to overcome years of underbuilding and adapt to changing economic realities.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

Read more commentaries by Stringer Asset Management