The results of last week's elections have rippled through financial markets. With a "Red Sweep" in Washington likely, markets are now pricing in a more aggressive policy agenda in areas such as tax cuts, tariffs, and deregulation, which could drive domestic economic growth but also increase inflation and deficit concerns.

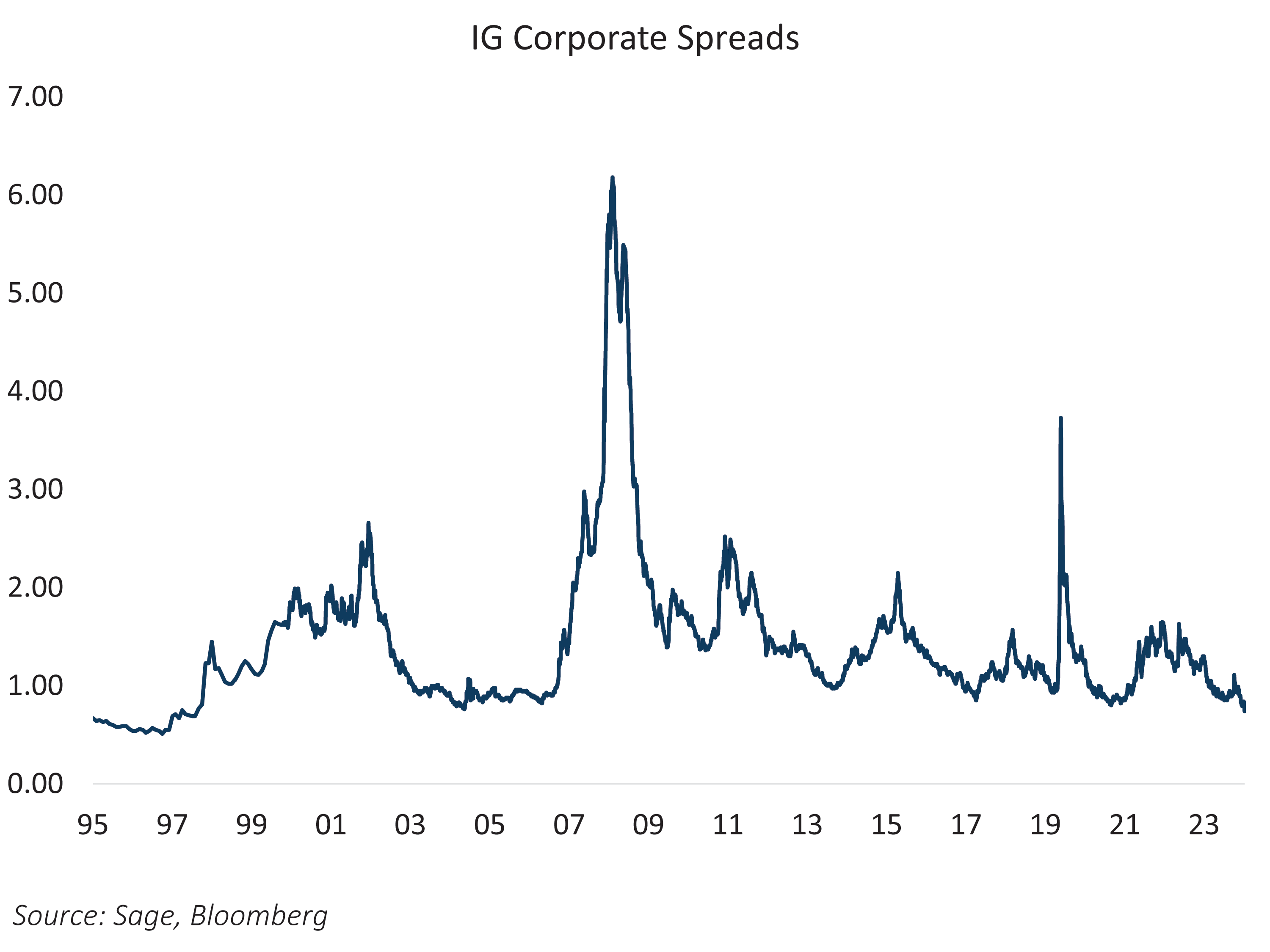

A Republican-controlled government is expected to be friendly to the corporate sector, and with the FOMC cutting rates by 25 bps as expected at its November meeting, credit continues to benefit from a growing economy and stimulative fiscal and monetary policies. The IG corporate credit spread now stands at 74 bps over Treasuries, which is the tightest level since 1997.

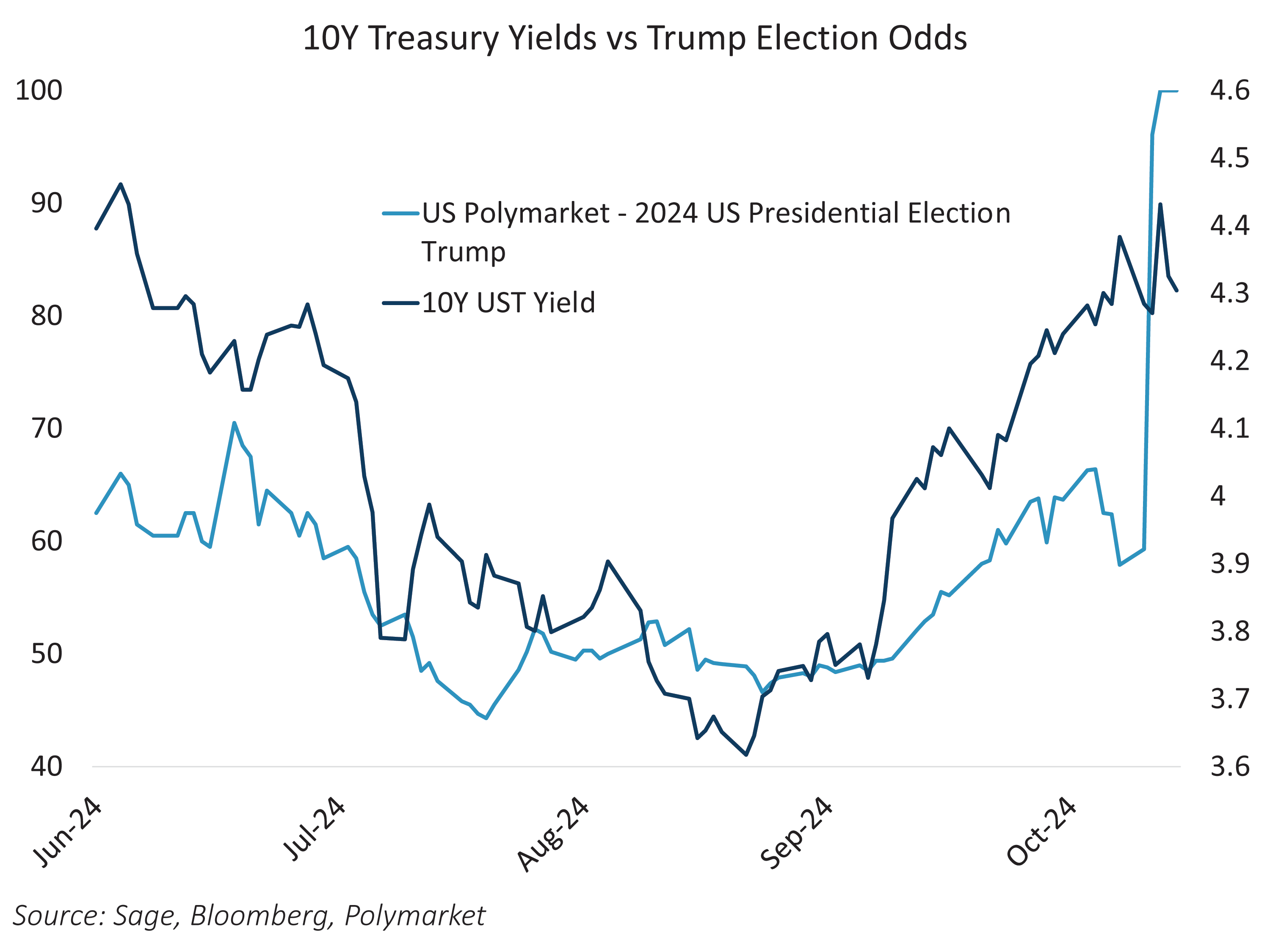

Since hitting a low on September 16, just ahead of the Fed’s 50 bps rate cut, Treasury yields have been on a journey of recalibration. Prior to election day, betting markets placed an increasing probability of Republican control across the executive and legislative branches. This caused yields to climb, reflecting concerns over anticipated policy shifts and the effects on inflation and deficits.

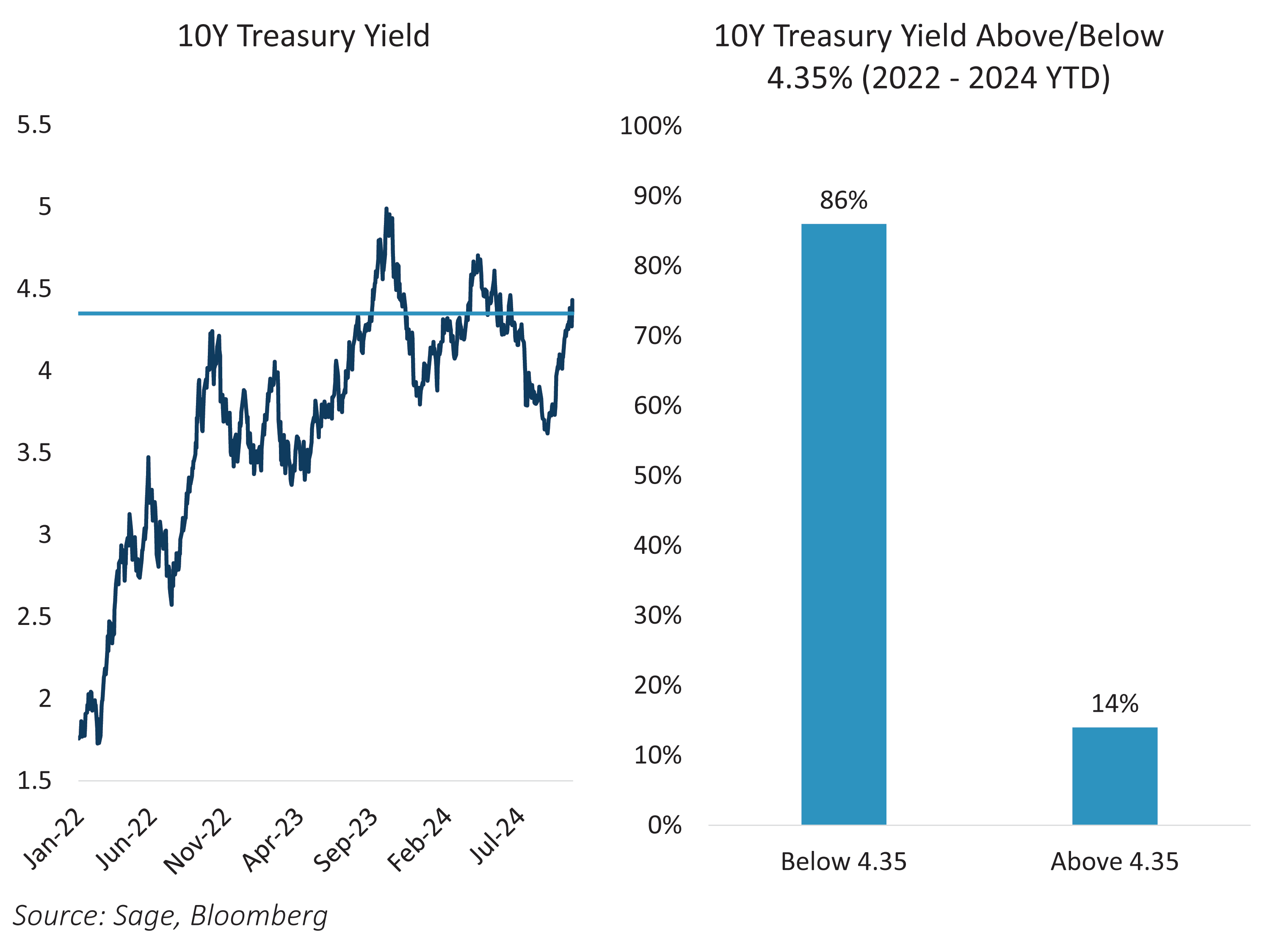

Despite having priced in a notable “Trump term premium” prior to the election, longer-term interest rates were lower last week. The 10Y and 30Y Treasury yields were down 8 bps and 12 bps, respectively, week-over-week. Despite the muted reaction during election week, the current level of interest rates continues to discount significant term premium as a result of the election and could be ahead of itself as it will take some time for tariffs and tax cuts to take effect. Even in the recent period of high inflation, during the worst of the post-Covid inflation and the most aggressive Fed rate hikes since the 1980s, the 10Y Treasury yield traded below 4.35% for all but 14% of the time.

While growing deficits and higher tariffs should theoretically translate into higher inflation, market pricing leaves room for this narrative to change or miss as the FOMC has continued to signal its determination to lower the policy rate to neutral and market expectations for stronger economic growth continue to rachet higher. After the FOMC's rate cut last week, markets are priced for only three more 25 bps cuts by mid-2026. We believe inflation is unlikely to change course from its current downtrend and the number of rate cuts could end up being more, as tax cuts, deregulation, and the effect of tariffs could take some time to flow through to the real economy.

For more news, information, and strategy, visit the ETF Strategist Channel.

This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our podcasts.

Read more commentaries by Sage Advisory