Takeaways

-

Q3 S&P 500® EPS growth expected to come in at 5.3%, the fifth consecutive quarter of growth

-

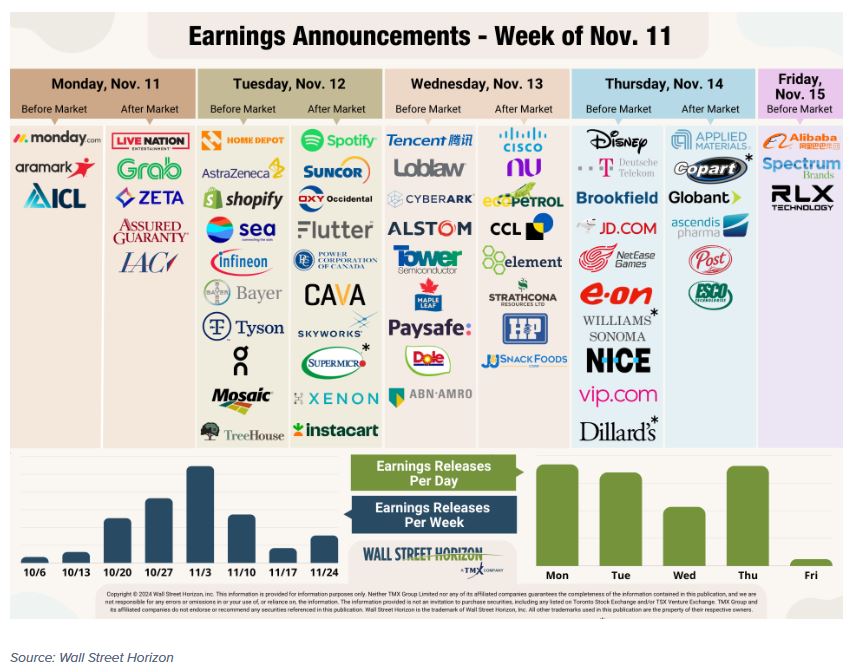

Large cap outlier earnings this week: LiveNation Entertainment, Occidental Petroleum Corp, The Mosaic Company, and The Walt Disney Company

-

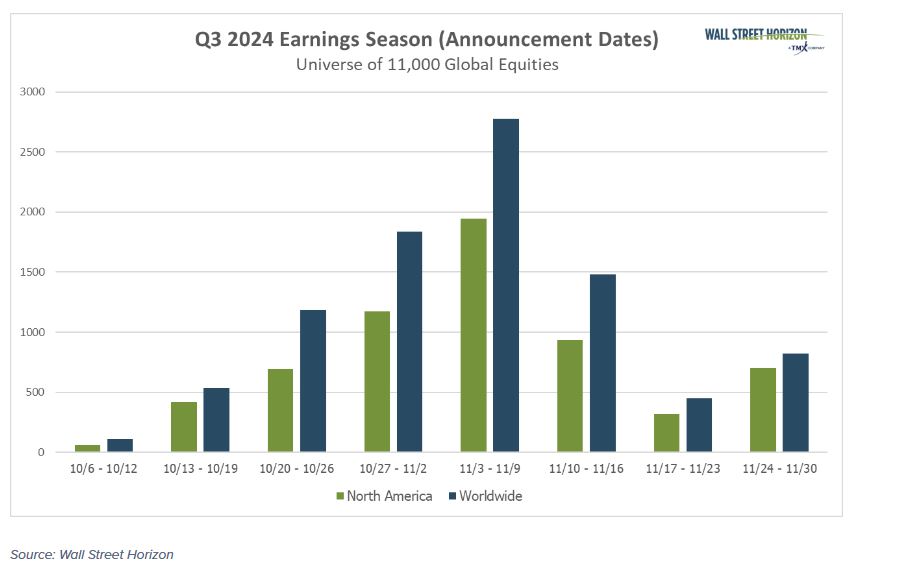

Last peak week of the Q3 earnings season with 2,640 global companies reporting

Investor uncertainty tends to be a detriment to the stock market, but last week the US got answers to two looming questions: who will be the 47th president of the United States and will the Federal Reserve cut rates for the second consecutive time since 2020? In many ways it didn’t matter what those answers were, just that they were out of the way and investors and US companies could begin to plan accordingly for Q4, 2025 and beyond.

On Wednesday, November 6, Donald Trump was announced as the 47th president of the United States, securing a second although not consecutive term. Equity markets have risen in the last week, with all three major indices (DJIA, S&P 500, NASDAQ) trading at record highs.1 Cryptocurrencies such as Bitcoin also received a boost, currently priced around $87k, as a reaction to the potential of lighter crypto regulation.2

The following day, Thursday November 7, the US Federal Reserve lowered interest rates an additional 25bps, on top of the jumbo 50bps cut back in September.3 The move was anticipated, although in the weeks leading up to the meeting the probability of the Fed not cutting rates had grown as a result of stronger-than-expected economic data.4

In the midst of all of this market moving news was also the continuation of the Q3 earnings season, with last week being the busiest week of the season with 3,181 companies reporting. Earnings continue to come in better than expected. With over 90% of the S&P 500 reported thus far, the YoY growth rate stands at 5.3%, the fifth consecutive quarter of growth, and an increase from 5.1% last week.5

Uncertainty Still Remains for US Corporations

Even with a new US president elect, uncertainty remains for US corporations that will wait and see what policies promoted on the campaign trail will actually be enacted, and how those will impact their bottom-line.

After falling to its lowest level in its nine years in the first quarter of 2024, the Late Earnings Report Index, our proprietary measure of CEO uncertainty, has been higher for the last two quarters. This quarter was likely due to the US presidential election being held during a peak week for Q3 earnings season, with many companies perhaps wanting to avoid getting lost in the news cycle and therefore pushing their earnings date.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, and anything above that indicates that companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests that companies feel they have a pretty good crystal ball for the near-term.

The official pre-peak season LERI reading for Q3 (data collected in Q4) stood at 278, well above the baseline reading. Our official post-peak season LERI, now that a majority of companies have reported for the quarter, also closed atypically high at 287. However, as stated above, this is likely a result of the US presidential election. We have noticed that the last two election cycles, 2016 and 2020, also resulted in outsized earnings date delays. As of November 12 there were 257 late outliers and 72 early outliers.

Outlier Earnings Dates This Week

Academic research shows that when a company confirms a quarterly earnings date that is later than when they have historically reported, it’s typically a sign that the company will share bad news on their upcoming call, while moving a release date earlier suggests the opposite.6

This week we get results from a number of large companies on major indexes that have pushed their Q3 2024 earnings dates outside of their historical norms. Four companies within the S&P 500 confirmed outlier earnings dates for this week, all of which are later than usual and therefore have negative DateBreaks Factors*. Those names are LiveNation Entertainment (LYV), Occidental Petroleum Corp (OXY), The Mosaic Company (MOS), and The Walt Disney Company (DIS).

* Wall Street Horizon DateBreaks Factor: statistical measurement of how an earnings date (confirmed or revised) compares to the reporting company's 5-year trend for the same quarter. Negative means the earnings date is confirmed to be later than historical average while Positive is earlier.

The Walt Disney Company

Company Confirmed Report Date: November 14, AMC

Projected Report Date (based on historical data): Wednesday, November 6, AMC

DateBreaks Factor: -3*

Disney is set to report FQ4 2024 results on Thursday, November 14, more than a week later than expected. This move pushes the report into the 46th week of the year after reporting in the 45th week last year. This also denotes the latest FQ4 earnings date for DIS in at least the last ten years.

For its fiscal third quarter Disney was able to beat both top and bottom-line Wall Street estimates.7 Strength from the company’s streaming business was somewhat offset by Disney’s parks and experiences segments which came in softer as a result of lower consumer demand.8 As the company was previously expected to report the day after the US presidential election it is possible they bumped forward one week to avoid the news cycle. However, it will be important to watch how certain Disney-specific metrics come in for FQ4. Within the entertainment segment those metrics are: number of paid subscribers and average monthly revenue per paid subscriber for ESPN+, Disney+ and Hulu, and within theme parks and consumer products those metrics are: international and domestic theme park attendance, revenue and operating income. During the August call Disney executives told analysts to expect parks metrics to be impacted for at least the next few quarters, but to be offset by strength in the entertainment division.9

On Deck This Week

This week marks the final peak week of earnings season, with over 2,640 global companies expected to report results. We start to get a read on the state of the US consumer when retailers begin to report results.

Home Depot kicked things off earlier this morning, and while the home improvement retailer was able to beat expectations on the top and the bottom-line, EPS was still lower YoY, and same store sales declined 1.3%.10 Chief Financial Officer, Richard McPhail, said that the consumer is still cautious which is leading to the deferral of big projects. In an interview with CNBC, McPhail noted “Our consumers continue to tell us that economic uncertainty and higher borrowing costs are on their minds.”11

The retail earnings parade continues on Thursday when department store, Dillard’s, releases results.

Q3 Earnings Wave

This earnings season, the peak weeks fell between October 28 - November 15, with each week reporting over 2,000 reports. November 7 was the most active day with 1,227 companies reporting. Thus far, 65% of companies have reported earnings (out of our universe of 11,000+ global names).

1 “S&P 500 posts record high close, Trump-linked stocks,” Reuters, by Lisa Pauline Mattackal and Purvi Agarwal, November 11, 2024, https://www.reuters.com

2 “Bitcoin jumps to record as Trump's election turbocharges cryptocurrencies,” Reuters, by Ankur Banerjee and Samuel Indyk, November 11, 2024, https://www.reuters.com

3 Federal Reserve issues FOMC statement, Board of Governors of the Federal Research System, November 7, 2024, https://www.federalreserve.gov

4 CME Group, FedWatch, November 12, 2024, https://www.cmegroup.com

5 Earnings Insight, FactSet, John Butters, November 8, 2024, https://advantage.factset.com/

6 Time Will Tell: Information in the Timing of Scheduled Earnings News, Journal of Financial and Quantitative Analysis, Eric C. So, Travis L. Johnson, Dec, 2018, https://papers.ssrn.com

7 The Walt Disney Company Reports Third Quarter and Nine Months Earnings for Fiscal 2024, August 7, 2024 https://thewaltdisneycompany.com

8 The Walt Disney Company Reports Third Quarter and Nine Months Earnings for Fiscal 2024, August 7, 2024 https://thewaltdisneycompany.com

9 The Walt Disney Company Reports Third Quarter and Nine Months Earnings for Fiscal 2024, August 7, 2024 https://thewaltdisneycompany.com

10 The Home Depot Announces Third Quarter Fiscal 2024 Results; Updates Fiscal 2024 Guidance, November 12, 2024 https://ir.homedepot.com

11 Home Depot’s sales are improving, but it says consumers are still cautious about spending, CNBC, by Melissa Repko, November 12, 2024 https://www.cnbc.com

Copyright © 2024 Wall Street Horizon, Inc. All rights reserved. Do not copy, distribute, sell or modify this document without Wall Street Horizon's prior written consent. This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies guarantees the completeness of the information contained in this publication, and we are not responsible for any errors or omissions in or your use of, or reliance on, the information. This publication is not intended to provide legal, accounting, tax, investment, financial or other advice and should not be relied upon for such advice. The information provided is not an invitation to purchase securities, including any listed on Toronto Stock Exchange and/or TSX Venture Exchange. TMX Group and its affiliated companies do not endorse or recommend any securities referenced in this publication. TMX, the TMX design, TMX Group, Toronto Stock Exchange, TSX, and TSX Venture Exchange are the trademarks of TSX Inc. and are used under license. Wall Street Horizon is the trademark of Wall Street Horizon, Inc. All other trademarks used in this publication are the property of their respective owners.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

© Wall Street Horizon

Read more commentaries by Wall Street Horizon