A once-mythical soft landing is at hand for the world’s major economies. The global expansion has remained resilient, withstanding restrictive monetary policy along with a host of geopolitical frictions. Inflation has been retreating, and employment levels remain very high. Equity markets have been especially strong.

That said, the mythology surrounding the incoming American government is an important factor in the outlook. The unstable nature of ongoing regional conflicts and the uncertain future of international commerce under the Trump administration could threaten performance in major world economies. Inflationary policy changes could add to sticky underlying price pressures and prevent a faster return to neutral monetary policy.

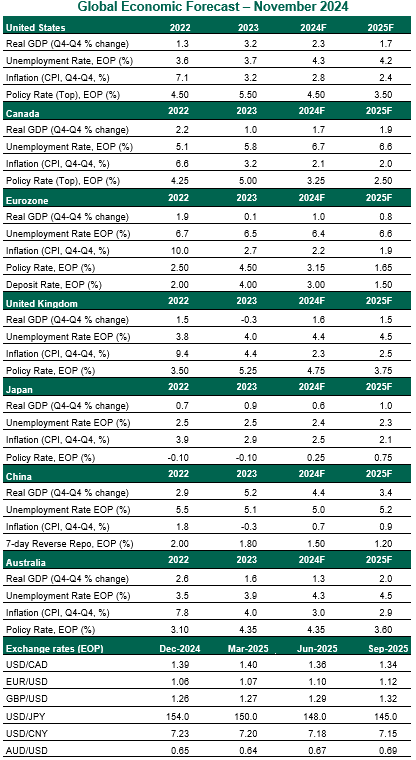

Following are our thoughts on how top areas are faring.

United States

- The U.S. economy performed well in the third quarter, with real gross domestic product (GDP) growing at 2.8% annualized pace. Consumers remain the main engine of growth. While much attention is focused on the economic consequences of the U.S. election, significantly altering our forecast at this time would be speculative. Inauguration is two months away; policies will take time to craft and enact; it may be a while before new measures become evident in the data. We believe the prospects for the soft landing are still favorable.

- The Fed’s policy rate remains sufficiently restrictive to justify continued interest rate cuts. But given the risks arising from tighter immigration policy, higher tariffs and the outlook for a prolonged fiscal imbalance, we now see the Fed taking a less urgent course of easing. The high level of interest rates may invite comment from the incoming administration, as it did prior to the pandemic.

Australia

- Australian economic momentum was soft in the first half of the year, but green shoots are starting to appear. Households are becoming less frugal, as reflected in the improvement in retail sales. Tax cuts coupled with steady wage gains are boosting consumers’ purchasing power, giving households confidence even as monetary conditions remain tight.

Overall, growth will remain below trend, as restrictive monetary policy continues to exert pressure on household balance sheets. A key risk for Australia is getting caught in the crossfire of the U.S.-China trade war, as both nations are among its top three trading partners. Weaker demand for Chinese goods will have a spillover impact on demand for Australian commodities.

- While economic conditions in Australia may not differ that much from its advanced economy peers, the Reserve Bank of Australia (RBA) continues to be an outlier. The central bank held the policy rate steady at its November meeting, as underlying inflation is too high for the central bank to pivot. A short and shallow easing cycle is expected to commence in early 2025.

Information is not intended to be and should not be construed as an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Under no circumstances should you rely upon this information as a substitute for obtaining specific legal or tax advice from your own professional legal or tax advisors. Information is subject to change based on market or other conditions and is not intended to influence your investment decisions.

© 2024 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. Incorporated with limited liability in the U.S. Products and services provided by subsidiaries of Northern Trust Corporation may vary in different markets and are offered in accordance with local regulation. For legal and regulatory information about individual market offices, visit northerntrust.com/terms-and-conditions.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out our most recent white papers.

© Northern Trust

Read more commentaries by Northern Trust