Summary

- North America and Qatar are set to drive the next wave of LNG additions to 2030, with North American export capacity set to double.

- Europe may require more LNG to offset volumes from Russia and for general energy security, but gas demand is generally expected to be flattish or moderately down.

- The overall outlook for LNG demand relies more on Asia, where LNG can help fuel economic growth, replace coal, or offset lower domestic gas production.

The next few years are set to see a significant expansion in global LNG export capacity, led by North America and Qatar. On the demand side, attention is largely focused on Asia, where economic growth and the opportunity to replace coal can drive greater LNG imports. In Europe, the focus is on energy security and diversity of supply, given an ongoing shift away from Russian natural gas. Today’s note discusses major LNG export capacity expansions and the countries and regions with rising demand.

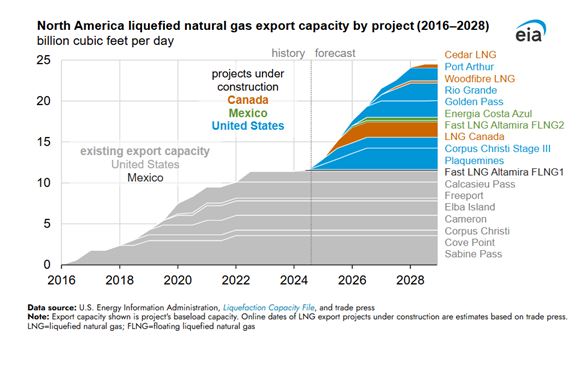

North America and Qatar are set to drive the next wave of LNG additions to 2030. According to the US Energy Information Administration, North American LNG export capacity is set to more than double from 11.4 to 24.4 Bcf/d using the baseload capacity of ten projects currently under construction. The bulk of the additions (9.7 Bcf/d) are located along the US Gulf Coast. Canada’s first LNG export project is expected online in 2025. The three LNG facilities under construction in British Columbia represent a combined 2.5 Bcf/d and will primarily supply Asia, given proximity to that growing market (read more). Meanwhile, Mexico accounts for 0.8 Bcf/d of capacity with projects on both coasts.

Additionally, there are a swath of projects in the US, Canada, and Mexico awaiting final investment decision (FID), which is when a company commits to building the project. Four more projects in Canada representing 4.1 Bcf/d of capacity have been approved by the Canadian regulator but are awaiting FID. Five projects are being developed along Mexico’s west coast representing aggregate capacity of 4.5 Bcf/d.

Select projects in the US were arguably delayed by an LNG export permit pause put in place by the Biden Administration in January 2024 (read more). The pause is expected to be quickly reversed under the new administration.

Meanwhile, Qatar has several LNG expansion projects underway, with the latest announced in February 2024. Qatar is expanding its export capacity by more than 80% from 10.1 Bcf/d to 18.7 Bcf/d by 2030. Qatar is largely focused on satisfying growing LNG demand in Asia.

In Asia, LNG Fuels Growth and Replaces Coal

The general outlook for LNG demand tends to rely on Asia, where LNG can be used for fueling economic growth and replacing coal. In some countries like Vietnam and the Philippines, LNG imports are needed to offset declines in domestic natural gas production.

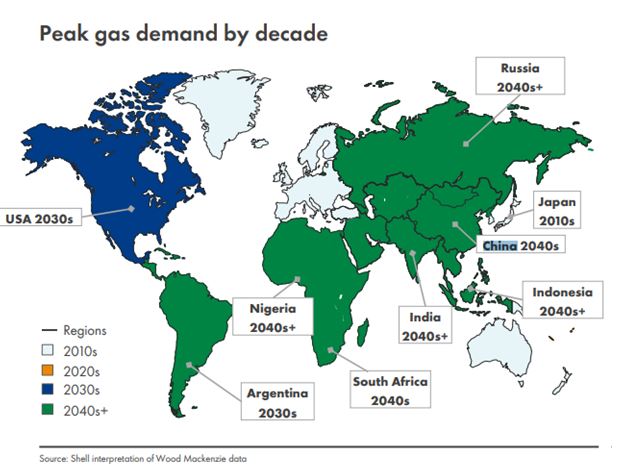

Broadly, Southeast Asia, China, and India are expected to drive global LNG demand growth. For example, Rystad Energy has forecasted that natural gas demand in India will double by 2040, requiring more LNG. While power demand is expected grow moderately, the bigger drive for India is expected to be industrial demand tied to fertilizer production, refining, and petrochemicals. China became the world’s largest LNG importer in 2023 and is expected to see continued growth in demand. In its 2024 LNG Outlook, Shell points to notable growth in LNG imports for Thailand and Bangladesh, with volumes more than doubling to ~3.3 Bcf/d for each in 2040. The map below from Shell’s LNG outlook provides a clear picture of what regions are expected to see growth in natural gas demand. Countries in green are not expected to see gas demand peak until 2040+.

For Europe, LNG Represents Energy Security

While overall natural gas demand has peaked there, Europe may require more LNG to offset volumes from Russia and for general energy security. Last month, Russia cut off natural gas volumes to Austria’s OMV, which was trying to recover sizable damages awarded in an arbitration process. Austria, Slovakia, and the Czech Republic receive natural gas from Russia via a pipeline that goes through Ukraine. Those shipments are expected to cease at the end of this year when the existing transit contract expires.

More broadly, the EU has a non-binding goal to stop importing Russian gas by 2027. In the first half of this year, however, Europe actually increased its imports of Russian LNG by 11%, with France, Spain, and Belgium accounting for the bulk of those volumes. According to media reports following a conversation with President-elect Trump, the European Commission President may angle for Europe to buy more US LNG in exchange for tariff relief. That said, it may be difficult for either leader to influence LNG trade given that US companies are typically supplying LNG under long-term sales contracts for a fixed liquefaction fee.

While there could be opportunities to replace Russian supplies, European gas demand is generally expected to be flat-to-down over time. On their recent earnings call, Cheniere’s (LNG) management noted that they expect European LNG demand to be stable through the middle of the next decade at around 120 to 130 million tons per year (~16-17 Bcf/d). The ongoing build out of regasification capacity in Europe enhances flexibility and overall energy security.

Tracking LNG-related Equities

An index of global equities is necessary for tracking the LNG market. The Alerian Liquefied Natural Gas Index (ALNGX) includes companies materially engaged in the LNG value chain, including companies focused on liquefaction, carrier services, and regasification. Some constituents participate in multiple segments of the LNG market.

ALNGX gained 5.8% on a total-return basis last month in conjunction with the US election results and stronger LNG prices in Asia and Europe as winter approaches. As of November 26, US companies accounted for 40% of the index, and Australia, which is also a major LNG exporter, represented 24%. ALNGX was yielding 3.6% as of November 29.

For more news, information, and strategy, visit the Energy Infrastructure Channel.

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our webcasts.

Read more commentaries by VettaFi