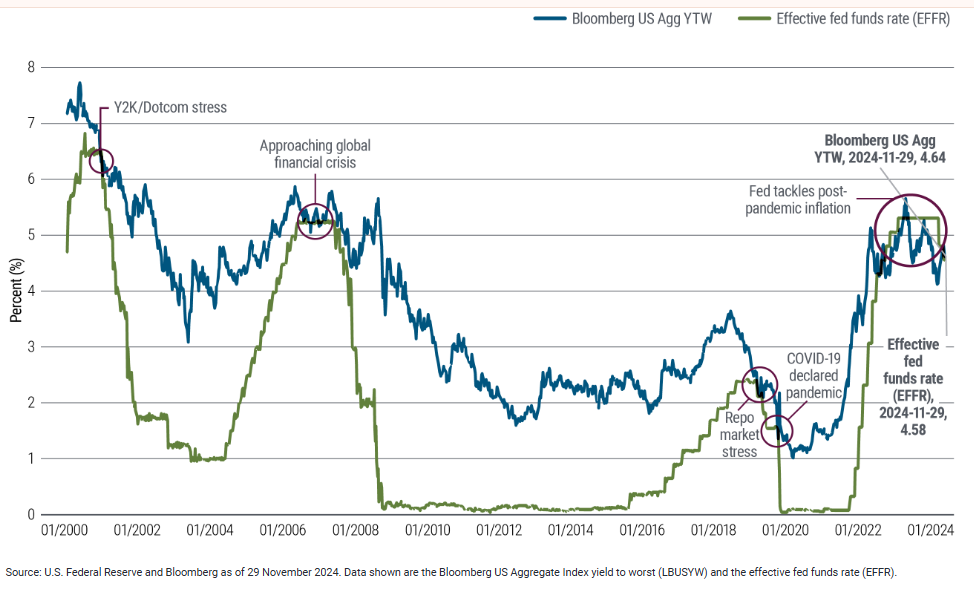

As post-pandemic disruptions to markets and economies recede, long-term trends are reasserting themselves. One key signal that markets are returning to historical patterns appeared in November, when a common yield measure on the Bloomberg US Aggregate Index climbed above the Federal Reserve policy rate for the first time in more than a year.

It’s difficult to overstate how extraordinary it was to have a benchmark bond yield running below – sometimes well below – the federal funds rate for such an extended period. Prior to the pandemic, this had only happened four times in this century, and never for more than a few weeks at a stretch (see Figure 1).

Figure 1: Benchmark bond index yield once again exceeds Fed’s policy rate

This prolonged reversal in the usual market trend reflected not only the Fed’s restrictive policy, but also investors’ response to the extreme inflation spike and other consequences of the pandemic. Many investors retreated into cash – which offered yields not seen in decades along with perceived safety – and stayed there.

Changed circumstances

Two years later, the market landscape has transformed. Now that the Fed has embarked on a rate-cutting path, over-allocating in cash creates reinvestment risk as the assets rapidly and repeatedly turn over into lower-yielding versions of themselves.

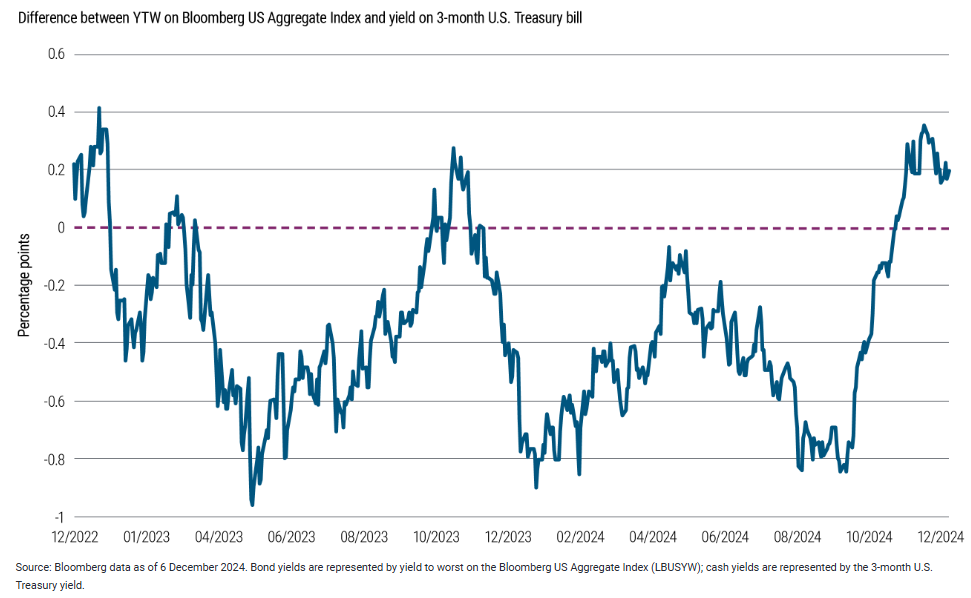

At the same time, we witnessed a profound shift higher in bond yields from pandemic-era lows. Relative to cash, where yields are dwindling as interest rates drop, bonds offer a more compelling opportunity: Consider the same core bond index yield measured against another common proxy for cash, the yield on the 3-month U.S. Treasury (see Figure 2). Both cash and bonds offered attractive yields over the past two years, but cash investors by nature can’t lock in those yields for longer time periods – and since September, when the Fed cut its policy rate by 50 basis points (bps), the outlook for cash yields relative to core bonds has diminished sharply.

Figure 2: U.S. core bonds outyielding cash equivalents

The Fed’s trajectory is not a foregone conclusion, and indeed we may see some upward revisions in officials’ rate projections following the December meeting, but the data and the communications to date suggest the most likely scenario is one of gradually lower rates. The Fed is looking to secure a soft landing for the U.S. economy – with labor markets healthy and inflation near target – and it has flexibility to pursue its goals despite expected or unexpected obstacles (e.g., trade policy, geopolitics, price surprises). This rate environment is highly favorable for bonds.

Bonds for the long run

Based on current relative valuations and market conditions, we believe there is compelling value in high quality, liquid public fixed income. Starting yields are attractive compared with other assets across the risk and liquidity spectrum – including cash – and historically, starting yields have been a strong indicator of long-term fixed income performance.

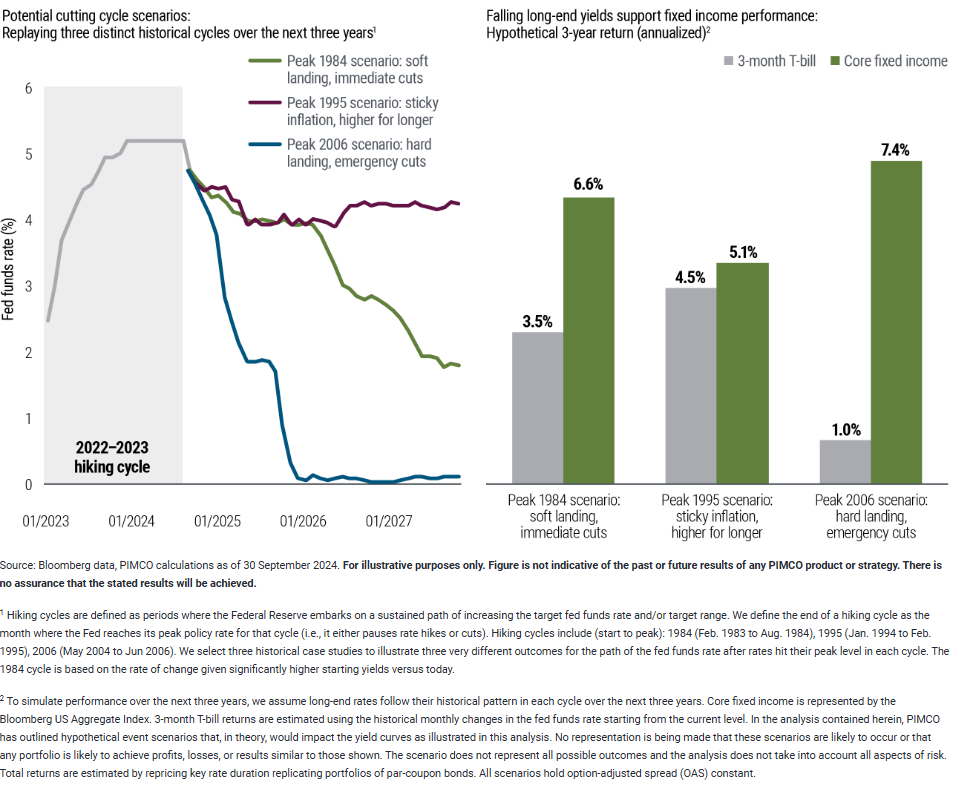

Also, bonds are well-positioned to withstand a range of scenarios outside the baseline. Historically, high quality bonds tend to perform well during soft landings – and even better in recessions, should that scenario play out instead. Bonds also have performed well historically across a range of different rate-cutting scenarios (like snowflakes, no two monetary cycles are alike) – see Figure 3. Whether the Fed took a very gradual (“higher-for-longer”) approach, or initiated a drastic drop, or took a downward path somewhere between those extremes, bonds subsequently outyielded cash in each of those historical rate environments.

Figure 3: Bonds have outpaced cash after the Fed initiates rate cuts, regardless of the path

Hedge and diversify risk

The bond market is effectively paying investors to hedge and diversify risk. Equity markets have a more checkered history with rate-cutting cycles, and indeed generally higher volatility over time – and we are in a period of heightened geopolitical unrest, along with leadership changes in major economies around the world.

Bonds and equities are negatively correlated today, after moving more in tandem during the post-pandemic inflation shock. A negative stock/bond correlation amplifies bonds’ potential to be a stable anchor for portfolios.

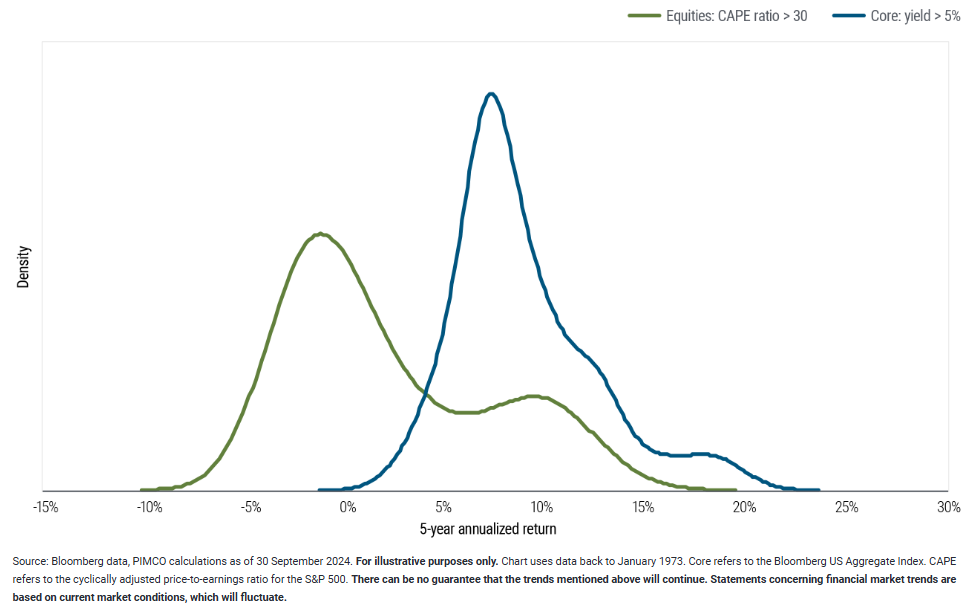

Historical trends also support bonds as an attractive risk hedge. Looking back at bond and equity markets on average since 1973, during periods when U.S. core bonds are yielding around 5% or greater while U.S. equities’ earnings ratios are above 30 – as they are today – bonds have offered higher five-year subsequent returns (see Figure 4), and with potentially lower volatility.

Figure 4: Historically, bonds at today’s yields have outpaced equities at today’s valuations

A fixed income allocation offers attractive yields, potential for price appreciation, and a liquid hedge against the risk that equities or other more volatile assets see a sustained contraction.

Takeaway

Market signals and Fed moves mean that bond yields have turned a corner. The combination of high starting yields and anticipation for lower rates creates an attractive outlook for a wide variety of bonds. Investors lingering in cash may want to consider fixed income.

Disclosures

All investments contain risk and may lose value. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and low interest rate environments increase this risk. Reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Equities may decline in value due to both real and perceived general market, economic and industry conditions. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value.

Bloomberg U.S. Aggregate Index represents securities that are SEC-registered, taxable, and dollar denominated. The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities. These major sectors are subdivided into more specific indices that are calculated and reported on a regular basis.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2024-1210-4087780

A message from Advisor Perspectives and VettaFi: To learn more about this and other topics, check out some of our videos.

© PIMCO

Read more commentaries by PIMCO